PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062028

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062028

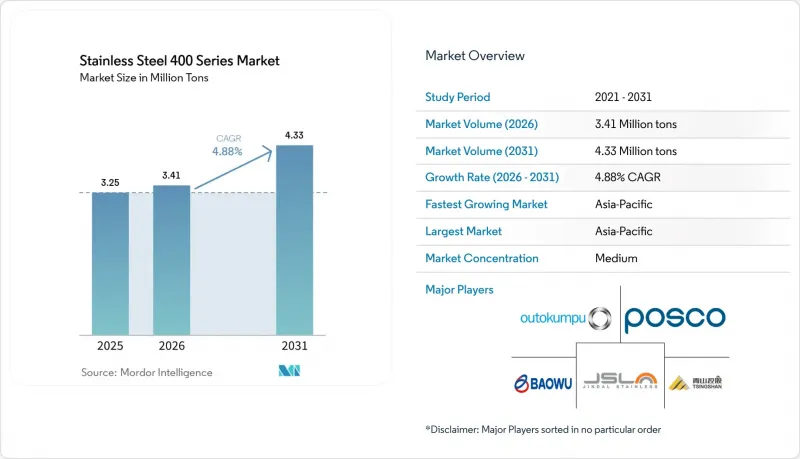

Stainless Steel 400 Series - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the stainless steel 400 series market size is projected to grow from 3.25 million tons in 2025 to 3.41 million tons in 2026 to reach 4.33 million tons by 2031, growing at a CAGR of 4.88% from 2026 to 2031.

This report is Segmented by Grade (409, 410, and More), Product Type (Sheets and Plates, Coils, and More), Application (Automotive Exhaust Systems, and More), End-Use Industry (Automotive and Transportation, Building and Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Global Stainless Steel 400 Series Market Trends and Insights

Growth in Construction and Infrastructure Spending

China's 2026 central budget sets aside CNY 755 billion (USD 109.22 billion) for municipal works and CNY 800 billion (USD 115.73 billion) in ultra-long treasury bonds that favor stainless structural products, propelling demand for ferritic grades in bridges, water pipelines, and public-transit upgrade. Grade 430, with 16-18% chromium, replaces galvanized steels in bridge decks and agricultural equipment because it balances corrosion resistance and formability. India's production-linked incentive scheme grants 4-15% on incremental stainless long-product sales, encouraging new ferritic melt shops. Rural water-safety rollouts in China extend stainless piping into previously untreated counties, enlarging the addressable base. Mega-projects in the Gulf and Southeast Asia broaden geographic exposure, though execution still hinges on public-finance cycles and input-price stability.

Cost Advantage Over Austenitic Grades Amid Nickel Volatility

Grade 409 trades at USD 1,800-2,200 per ton versus USD 3,000-3,500 for 304, a gap that widens when nickel surpasses USD 18,000 per ton. Indonesia supplies roughly 70% of global nickel ore, yet stricter 2026 quotas revived pricing after a 40% slide from 2021 peaks. Ferritic grades, containing little to no nickel, insulate OEM budgets and trigger substitution in exhausts, appliance panels, and re-rollers' feedstock. When nickel retreats, austenitic grades claw back share where higher corrosion thresholds are essential, underscoring a price-elastic see-saw across end markets.

Chromium and Ferrochrome Price Volatility

In early 2026, India's ferrochrome prices reached INR 74,000-75,000 (USD 784.17-794.77) per ton. Meanwhile, Chinese import offers were around USD 0.84 per pound, reflecting supply constraints due to production curtailments in South Africa. The Carbon Border Adjustment Mechanism (CBAM) applies default carbon dioxide (CO2) factors of 3.5-4.0 tons to unverified imports, resulting in taxes on blast-furnace stainless steel and higher Electric Arc Furnace (EAF) premiums. To address potential price fluctuations, China's state-owned mining companies secured over 500 million tons of chromite from international sources. Mills without captive ore resources face margin pressures during ferrochrome price increases, driving consolidation among vertically integrated producers.

Other drivers and restraints analyzed in the detailed report include:

- Rising Usage in Kitchenware and Home Appliances

- Adoption in Bipolar Plates for Green-Hydrogen Electrolyzers

- Additive-Manufacturing Cracking and Printability Issues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Grade 409 accounted for 41.11% of the stainless steel 400 series market share in 2025 and is projected to expand at 5.45% CAGR to 2031. The stainless steel 400 series market size for automotive exhaust lines benefits from grade 409's 10.5-11.75% chromium chemistry that withstands 600°C gases at half the cost of 304. Grade 430 capitalizes on appliance and architectural panels, buoyed by China's appliance-trade-in bounty. Martensitic 410, 420, and 440 grades deliver greater than or equal to 55 HRC hardness, fueling surgical-instrument and industrial-knife demand. Niche grade 446 services furnace linings and heat exchangers thanks to 23-27% chromium, but trades at a higher alloy surcharge.

Emerging ferritic variants such as T4003 and SOLEIL 4003 marry smaller than or equal to 13% chromium with titanium stabilizers, improving weldability and ductility for train shells and bridge decks. Patented surface activation by Nippon Steel enhances oxide-film stability, shrinking oxidation weight gain to 0.3 mg/cm2 at 600°C and extending service life in humid heat exchangers. Producers increasingly differentiate through coating and pickling know-how rather than raw metallurgy alone.

In 2025, sheets and plates accounted for 42.32% of the volume, reflecting their application in appliance skins, cladding, and body panels that require smooth surfaces and precise gauges. Bars and rods are projected to achieve the highest compound annual growth rate (CAGR) of 5.67%, driven by demand for precision-machined valves, gears, and the free-cutting 416 variant containing 0.15-0.30% sulfur. Coils address the needs of service centers and re-rollers, focusing on consistent chemistry across multi-ton lots. Pipes and tubes cater to the construction and energy sectors, while foils thinner than 0.1 mm support solid oxide fuel cell (SOFC) and electrolyzer stacks, creating a high-margin segment within the stainless steel 400 series market.

China's mills are advancing industry benchmarks: Fushun's big-data controls have improved plate precision by 65%, Liyang Delong operates the world's widest 2,680 mm hot mill, and Shanxi Fujian has implemented a 1,550 mm 20-roll cold mill, achieving micron-level tolerances. Surface finishes ranging from 2B to 8K command premiums of 10-30%, driving investments in polishing processes. While wire-arc directed energy deposition (DED) technology reduces raw material usage by 78% during large repairs, it remains less efficient in sheet throughput compared to conventional rolling, which continues to dominate.

Geography Analysis

Asia-Pacific commanded 52.34% of 2025 volume and is advancing at a 5.72% CAGR to 2031, underscored by China's CNY 755 billion (USD 109.22 billion) infrastructure budget and CNY 250 billion (USD 36.16 billion) appliance-trade-in plan. China's top three mills captured 67.30% of 2024 stainless output, consolidating supply and raising bargaining power. India's utilization hovers near 60% against 7.5 million t capacity, giving headroom for ferritic ramp-ups; Jindal's 1.2 million ton Indonesian melt shop reinforces regional self-sufficiency. Indonesia's POSCO-Tsingshan venture adds 2 million t of captive-ore-fed capacity, positioning the archipelago as a low-cost hub.

U.S. automotive still pulls grade 409, but EV diffusion trims per-vehicle stainless loadings. Tariff layers across the U.S., Canada, and Mexico entangle trade, steering buyers toward regional mills.

Europe confronts CBAM, allocating default CO2 factors that inflate landed costs for high-emission imports. Outokumpu's EUR 200 million (USD 229.65 million) Tornio upgrade pivots to duplex and precipitation-hardened grades, while Acerinox and Aperam sink EUR 160 million (USD 183.72 million) to curb energy use amid soft demand. Germany and the Nordics spearhead electrolyzer rollouts, favoring metallic bipolar plates. South America and MEA remain smaller slices but gain from localized appliance and construction needs despite currency risk.

- Acerinox

- Aperam

- Baosteel Desheng Stainless Steel Co., Ltd.

- Eternal Tsingshan Group Co., Ltd.

- Fushun Special Steel Co., Ltd.

- Jindal Steel

- NIPPON STEEL CORPORATION

- Outokumpu

- POSCO

- Shanxi Taigang Stainless

- Shyam Metalics

- Viraj Profiles Pvt. Ltd.

- Yieh Corp.

- China Baowu Steel Group

- TSINGSHAN HOLDING GROUP

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in construction and infrastructure spending

- 4.2.2 Cost advantage over austenitic grades amid nickel volatility

- 4.2.3 Rising usage in kitchenware and home appliances

- 4.2.4 Adoption in bipolar plates for green-hydrogen electrolyzers

- 4.2.5 Demand for ultra-thin ferritic foils in solid-oxide fuel cells and metal-supported batteries

- 4.3 Market Restraints

- 4.3.1 Chromium and ferro-chrome price volatility

- 4.3.2 Additive-manufacturing cracking and printability issues

- 4.3.3 Carbon-border-adjustment and lifecycle-CO2 rules raising compliance costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Grade

- 5.1.1 409

- 5.1.2 410

- 5.1.3 420

- 5.1.4 430

- 5.1.5 440

- 5.1.6 Other Grades (446, etc.)

- 5.2 By Product Type

- 5.2.1 Sheets and Plates

- 5.2.2 Coils

- 5.2.3 Bars and Rods

- 5.2.4 Pipes and Tubes

- 5.2.5 Other Product Types (Ultra-thin foil, etc.)

- 5.3 By Application

- 5.3.1 Automotive Exhaust Systems

- 5.3.2 Kitchenware and Cookware

- 5.3.3 Industrial Equipment

- 5.3.4 Construction and Architecture

- 5.3.5 Electrical Appliances

- 5.3.6 Energy Generation

- 5.3.7 Other Applications (Hydrogen Electrolyzer Plates, etc.)

- 5.4 By End-User Industry

- 5.4.1 Automotive and Transportation

- 5.4.2 Building and Construction

- 5.4.3 Consumer Goods

- 5.4.4 Industrial Machinery

- 5.4.5 Energy and Power

- 5.4.6 Aerospace and Defense

- 5.4.7 Other End-user Industries (Healthcare, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Initiatives

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Acerinox

- 6.4.2 Aperam

- 6.4.3 Baosteel Desheng Stainless Steel Co., Ltd.

- 6.4.4 Eternal Tsingshan Group Co., Ltd.

- 6.4.5 Fushun Special Steel Co., Ltd.

- 6.4.6 Jindal Steel

- 6.4.7 NIPPON STEEL CORPORATION

- 6.4.8 Outokumpu

- 6.4.9 POSCO

- 6.4.10 Shanxi Taigang Stainless

- 6.4.11 Shyam Metalics

- 6.4.12 Viraj Profiles Pvt. Ltd.

- 6.4.13 Yieh Corp.

- 6.4.14 China Baowu Steel Group

- 6.4.15 TSINGSHAN HOLDING GROUP

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment