PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062029

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062029

Silver Iodide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

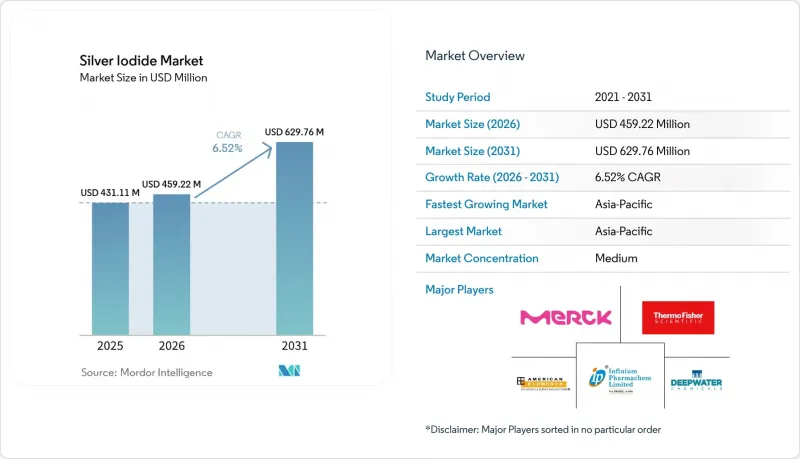

According to Mordor Intelligence, the silver iodide market size is projected to be USD 431.11 million in 2025, USD 459.22 million in 2026, and reach USD 629.76 million by 2031, growing at a CAGR of 6.52% from 2026 to 2031.

This report is Segmented by Type (Crystalline, Powdered, and Suspension/Colloidal), Application (Cloud Seeding, Antiseptic and Antimicrobial Agents, and More), End-User Industry (Agriculture and Environment, Healthcare and Pharmaceuticals, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Silver Iodide Market Trends and Insights

Surging Demand for Antimicrobial and Antiseptic Coatings

Hospital systems are adopting silver iodide (AgI)-based surface films, which release ions for 6-12 months, to manage infection costs. These films have a longer functional lifespan compared to colloidal silver. Silver iodide coatings have met the International Organization for Standardization (ISO) 10993 cytotoxicity thresholds and comply with the European Union Medical Device Regulation (EU MDR). Procurement increased after the United States Food and Drug Administration (US FDA) implemented stricter aseptic guidance in 2024. Consequently, the silver iodide market is experiencing consistent demand, particularly from retrofit programs in operating rooms. Suppliers report a 25-30% reduction in infection rates to support premium pricing.

Expansion of Silver-Iodide-Based Sensors in Industrial IoT

Graphene layers integrated with AgI nanocrystals detect iodine vapor at 0.5 parts per million (ppm) with millisecond response time while consuming 40% less power compared to metal-oxide sensors. Japan and South Korea have included halogen sensing in their 2025 smart-factory roadmaps. Wind-farm operators are adopting battery nodes with these sensors, contributing to the growth of the silver iodide market in offshore projects. Clinical groups are utilizing AgI electrodes for non-invasive urinary iodine tests, expanding the application in the healthcare sector. Furthermore, the integration of these sensors into 5G gateways is driving demand for colloidal precursors.

Environmental and Ethical Opposition to Weather-Modification Trials

Idaho House Bill 23 proposes a ban on cloud seeding, citing concerns about silver residue deposition in watersheds. Similar legislative discussions are ongoing in Iowa, with non-governmental organizations (NGOs) referencing precautionary principles. Insurance providers are delaying decisions due to the absence of clear liability frameworks, resulting in halted equipment orders. If such bans expand, North American demand could decrease by 15%, affecting the silver iodide market, which represents its largest application. Cloud seeding companies are requesting Environmental Protection Agency (EPA) guidelines to address these concerns and restore market confidence.

Other drivers and restraints analyzed in the detailed report include:

- Renewed Use in Analogue and Instant-Film Photography

- Tailored AgI Nanoparticles for Neuromorphic and Memristor Devices

- Rapid Progress of Bio-Based Ice-Nucleating Proteins as Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Crystalline grades captured 47.11% revenue in 2025 because their lattice parameter of 4.592 angstroms mirrors that of hexagonal ice and lowers the nucleation barrier. Powdered forms occupied 28% and grew steadily among ground-based seeding cooperatives. Suspension and colloidal variants expanded at 7.68%, catalyzed by sensor ink demand.

Crystalline suppliers leverage closed-loop systems to satisfy REACH dossiers, crowding out smaller rivals. Colloidal innovators tap solution-phase routes to engineer nanoflakes for spin-coated memristor stacks. Tokyo Chemical Industry scales 10 g/L suspensions for research and development, while Merck bundles AgI with test-grade acetylene black to create drop-in conductive pastes. These moves diversify revenue while lifting average selling prices, underpinning the silver iodide market.

Geography Analysis

Asia-Pacific generated 37.15% revenue in 2025 and accelerated at 7.76% through 2031 as China deploys the world's largest weather-modification network, and Japan scales IoT sensor manufacturing. India's Infinium Pharmachem adds 500 tons of annual capacity, sharpening regional price competition. South Korea and Taiwan explore AgI memristors for 3 nm processes, potentially adding USD 100 million incremental demand by 2028. ASEAN pilots, though tiny today, may expand if haze-control mandates gain funding.

In 2025, North America demonstrated significant market activity, driven by western U.S. seeding initiatives that enhanced snowpack levels. While legislative resistance in Idaho and Iowa presents challenges, adoption by hospitals and research and development (R&D) entities supports market stability. Canada and Mexico operate sporadic programs, with U.S. laboratories leading in the consumption of ultra-pure AgI for federally backed nanodevice projects.

Europe, led by Germany, the U.K., and France, maintained a strong presence in the market. The stringent REACH registration increases entry barriers and consolidates influence among established players like Merck KGA-MERCK.COM. Although cloud-seeding budgets are limited, the market benefits from advancements in perovskite R&D and antimicrobial applications. Nordic countries are utilizing AgI for offshore wind blade coatings to enhance resistance to salt fog.

South America and the Middle East & Africa regions exhibited notable developments. The UAE conducted numerous missions in 2025, reporting improved rainfall outcomes. Saudi Arabia initiated a national program in 2024, with Morocco exploring similar strategies. Brazil is testing ground-based generators to protect soybean yields, though financial constraints remain a consideration. South Africa is evaluating AgI seeding to support Cape Town's reservoirs. These regions, despite starting from smaller bases, contribute to the growth of the global silver iodide market.

- Abcr GmbH

- American Elements

- Aritech Chemazone Pvt. Ltd.

- Ascensus

- Deep Water Chemicals

- ESPI Metals

- Infinium Pharmachem Limited

- Merck KGaA

- Micron Platers

- Nanoshel LLC

- Santa Cruz Biotechnology Inc.

- Thermo Fisher Scientific Inc.

- Tokyo Chemical Industry (India) Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for antimicrobial and antiseptic coatings

- 4.2.2 Expansion of silver-iodide-based sensors in industrial IoT

- 4.2.3 Renewed use in analogue and instant-film photography

- 4.2.4 Tailored AgI nanoparticles for neuromorphic and memristor devices

- 4.2.5 Break-through integration in perovskite and thin-film PV cells

- 4.3 Market Restraints

- 4.3.1 Environmental and ethical opposition to weather-modification trials

- 4.3.2 Rapid progress of bio-based ice-nucleating proteins as substitutes

- 4.3.3 High purity AgI feed-stock price volatility and hedging costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Crystalline

- 5.1.2 Powdered

- 5.1.3 Suspension/Colloidal

- 5.2 By Application

- 5.2.1 Cloud Seeding

- 5.2.2 Antiseptic and Antimicrobial Agents

- 5.2.3 Photography and Imaging

- 5.2.4 Electro-chemical and Sensor Applications

- 5.2.5 Research and Military Uses

- 5.2.6 Other Applications (Synthesis, Coatings)

- 5.3 By End-User Industry

- 5.3.1 Agriculture and Environment

- 5.3.2 Healthcare and Pharmaceuticals

- 5.3.3 Defense and Aerospace

- 5.3.4 Industrial Manufacturing

- 5.3.5 Other End-user Industries (Research, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Initiatives

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Abcr GmbH

- 6.4.2 American Elements

- 6.4.3 Aritech Chemazone Pvt. Ltd.

- 6.4.4 Ascensus

- 6.4.5 Deep Water Chemicals

- 6.4.6 ESPI Metals

- 6.4.7 Infinium Pharmachem Limited

- 6.4.8 Merck KGaA

- 6.4.9 Micron Platers

- 6.4.10 Nanoshel LLC

- 6.4.11 Santa Cruz Biotechnology Inc.

- 6.4.12 Thermo Fisher Scientific Inc.

- 6.4.13 Tokyo Chemical Industry (India) Pvt. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment