PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062059

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062059

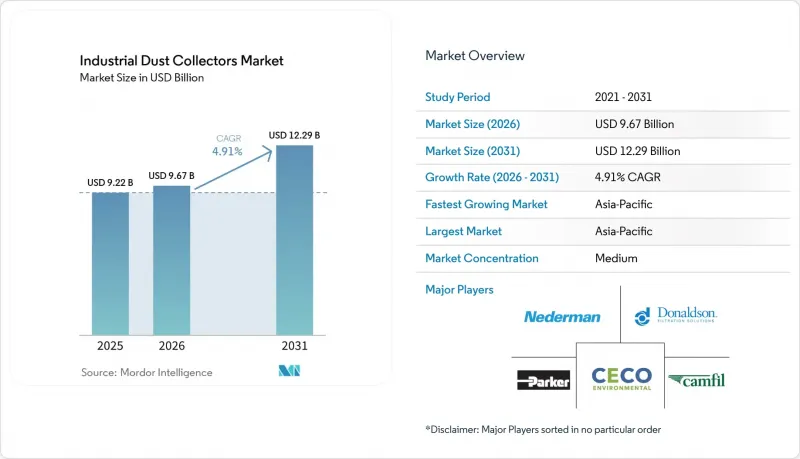

Industrial Dust Collectors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the industrial dust collectors market size is projected to be USD 9.22 billion in 2025, USD 9.67 billion in 2026, and reach USD 12.29 billion by 2031, growing at a CAGR of 4.91% from 2026 to 2031.

This report is Segmented by Collector Type (Baghouse, Cartridge, and More), Filter-Cleaning Mechanism (Continuous-Pulse, On-Demand Pulse, Sonic/Ultrasonic), Mobility (Stationary, Portable), End-Use Industry (Manufacturing, Food and Beverage, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Industrial Dust Collectors Market Trends and Insights

Rapid Industrialization in Asia-Pacific and Africa

India has set a manufacturing output target of USD 1 trillion by 2030, with a projected growth rate of 12.5% CAGR. ASEAN factories are expected to grow by 5.4% in 2024 and 4.8% in 2025, driven by demand in cement, steel, and chemical sectors requiring high-capacity baghouse and electrostatic-precipitator systems. China's industrial output, estimated at USD 5.3 trillion in 2024, is sustaining retrofit projects across coal-fired power plants and non-ferrous smelters. In Vietnam, USD 36.6 billion in 2024 Foreign Direct Investment (FDI) directed toward electronics and automotive facilities is increasing demand for cleanroom-grade cartridge collectors. Sub-Saharan Africa's cement sector presents growth opportunities; however, infrastructure limitations currently restrict developments to tier-one projects supported by multilateral funding.

Expansion of Dust-Intensive Battery and EV-Material Plants

In 2024, a Quebec battery-material plant received a custom baghouse from Macrotek, designed with spark-detection interlocks. Meanwhile, Donaldson's Torit PowerCore battery module achieves 99.99% efficiency on sub-micron particles, operating at a differential pressure of under 4 in.W.C. and reducing fan energy consumption by 20%. As Chilean lithium refineries expand towards U.S. gigafactories, there is a preference for modular, skid-mounted units that enable phased commissioning. Stringent fire-safety codes increase engineering costs but ensure compliance with safety standards for explosion-proof hybrids. The production of lithium-ion cathodes and anodes introduces combustible metal-dust hazards, requiring explosion-proof collectors equipped with High-Efficiency Particulate Air (HEPA) H13/H14 filtration and static-dissipative linings.

Skilled-Labor Shortage for Installation and Service

Apprenticeships lasting 2 to 3 years are essential for tasks like high-voltage wiring, fabric tensioning, and classifying explosion hazards. A shortage of installers leads to project delays of 4 to 8 weeks, hindering aftermarket growth as operators defer media changes. In response, vendors offer factory-acceptance testing and pre-commissioning services, yet they take on performance risks, resulting in reduced profit margins.

Other drivers and restraints analyzed in the detailed report include:

- Retrofit Demand from Aging Cement and Steel Assets

- Carbon-Neutral Collector Designs Unlocking European Union Subsidies

- Slow Adoption in Micro-SME Fabrication Clusters

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Baghouse controlled 32.21% revenue in 2025, reflecting its dominance in cement, steel, and power generation. The industrial dust collectors market size for hybrid and modular platforms is projected to expand at 5.58% CAGR, capitalizing on battery gigafactory demand for skid-mounted, explosion-proof packages. Mitsubishi Power's PTFE Hybrid Bag Filter marries electrostatic pre-charging with fabric media to achieve 99.9% efficiency while trimming pressure drop 25%. NFPA 660 harmonizes combustible-dust criteria, cutting engineering costs and accelerating permitting.

Hybrid adoption cannibalizes cyclone and wet-scrubber share in processes with fine or sticky dust. Vendors that can deliver rapid-install modules with integrated spark detection win bids at lithium processing, cathode precursor, and graphite-anode lines. Upstream in cement, fabric upgrades to PPS or P84 bags avert full replacement, sustaining aftermarket revenue even as new-build demand migrates to EV materials.

Continuous-pulse systems captured 52.23% of 2025 revenue and will expand at 5.67% CAGR. Real-time differential-pressure sensors adjust pulse sequencing, slashing compressed-air use 30% and extending media life 25%. On-demand pulse solutions serve intermittent processes such as batch pharma blending, while sonic cleaning attracts Nordic cement plants with high power tariffs. AI-based predictive platforms underpin continuous-pulse dominance by monetizing data through SaaS.

IoT bundling differentiates offerings: vendors provide cyber-secure gateways, multi-protocol support, and cloud dashboards. As continuous-pulse becomes baseline, differentiation tilts to software sophistication and value-added service contracts. The industrial dust collectors market share for on-demand and sonic segments narrows but remains relevant in specialized duty cycles.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 46.34% of the revenue share, with a growth rate of 5.54% CAGR. China's enforcement of stack limits, ranging from 10 to 30 mg/m3, has driven baghouse retrofits in kilns and boilers. India's Clean Air Programme, targeting a 40% reduction in particulate matter (PM) by 2026, is increasing demand for collectors in industrial corridors. Vietnam's electronics FDI and Japan's battery-cell production expansions are driving the need for portable, HEPA-grade units. Additionally, cement expansion projects in the ASEAN region are supporting demand for high-capacity baghouses.

North America has strengthened its position, supported by the U.S. EPA's tightening of opacity regulations. Tenaris's retrofit in Pennsylvania reflects a broader trend of mills established before 2000 upgrading to meet stricter NESHAP regulations. In Canada, mines are utilizing edge analytics to optimize pulse cleaning processes. Aerospace hubs in Mexico are adopting portable fume extractors following OSHA's 2024 reduction of hexavalent chromium permissible exposure limits (PELs). Skilled labor shortages are delaying installations but are also driving demand for turnkey contracting solutions.

Europe is leveraging EU carbon-neutral subsidies under the Industrial Emissions Directive, promoting ultrasonic and heat-recovery designs. Filtrabit's loan in Finland highlights the role of grants in adoption. In Germany, BAFA supports high-efficiency units with 40% capital expenditure coverage. Nordic countries are favoring compressor-free sonic cleaning due to electricity price advantages. Russia faces challenges as sanctions limit access to advanced media, impacting performance improvements. In South America and the Middle East & Africa, growth opportunities are available in Brazil's bagasse sector, Saudi Arabia's petrochemicals, and South Africa's silica retrofits.

- Air Distribution Technologies, Inc.

- Airex Industries

- Camfil

- CECO ENVIRONMENTAL

- Dantherm Group A/S

- Donaldson Company, Inc.

- Keller Lufttechnik GmbH + Co. KG

- Longjing Environmental Protection

- Micronics Engineered Filtration Group, Inc.

- Nederman Holding AB

- PARKER HANNIFIN CORP

- SCHEUCH Group

- Sly, LLC.

- Thermax Limited

- U.S. Air Filtration, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid industrialisation in Asia-Pacific and Africa

- 4.2.2 Expansion of dust-intensive battery and EV-material plants

- 4.2.3 Retrofit demand from ageing cement and steel assets

- 4.2.4 Carbon-neutral collector designs unlocking European Union subsidies

- 4.2.5 Edge-analytics-enabled predictive-maintenance savings

- 4.3 Market Restraints

- 4.3.1 Skilled-labour shortage for installation and service

- 4.3.2 Slow adoption in micro-SME fabrication clusters

- 4.3.3 Dust-less power-tool integration reducing demand

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Collector Type

- 5.1.1 Baghouse

- 5.1.2 Cartridge

- 5.1.3 Cyclone

- 5.1.4 Wet Scrubbers

- 5.1.5 Electrostatic Precipitators

- 5.1.6 Other Collector Types (Hybrid/Modular Systems)

- 5.2 By Filter-Cleaning Mechanism

- 5.2.1 Continuous-Pulse

- 5.2.2 On-Demand Pulse

- 5.2.3 Sonic/Ultrasonic

- 5.3 By Mobility

- 5.3.1 Stationary

- 5.3.2 Portable

- 5.4 By End-Use Industry

- 5.4.1 Manufacturing

- 5.4.2 Food and Beverage

- 5.4.3 Pharmaceuticals

- 5.4.4 Chemical Processing

- 5.4.5 Power Generation

- 5.4.6 Cement

- 5.4.7 Mining and Metals

- 5.4.8 Woodworking and Furniture

- 5.4.9 Other End-user Industries (Textile, Automotive, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Air Distribution Technologies, Inc.

- 6.4.2 Airex Industries

- 6.4.3 Camfil

- 6.4.4 CECO ENVIRONMENTAL

- 6.4.5 Dantherm Group A/S

- 6.4.6 Donaldson Company, Inc.

- 6.4.7 Keller Lufttechnik GmbH + Co. KG

- 6.4.8 Longjing Environmental Protection

- 6.4.9 Micronics Engineered Filtration Group, Inc.

- 6.4.10 Nederman Holding AB

- 6.4.11 PARKER HANNIFIN CORP

- 6.4.12 SCHEUCH Group

- 6.4.13 Sly, LLC.

- 6.4.14 Thermax Limited

- 6.4.15 U.S. Air Filtration, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment