PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062060

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062060

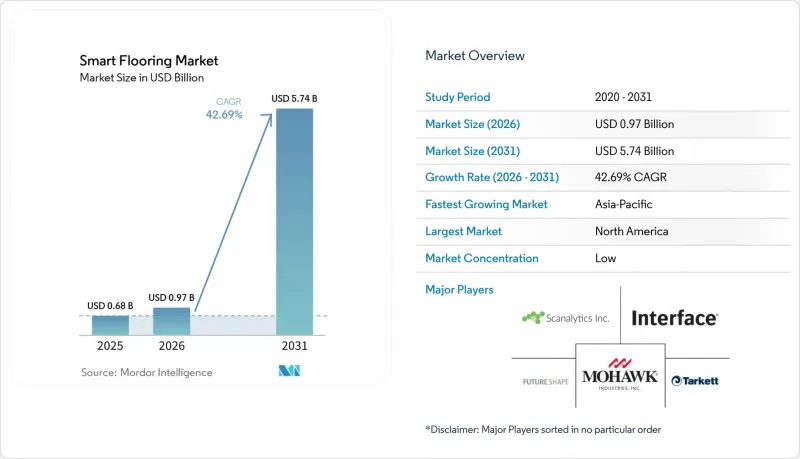

Smart Flooring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the smart flooring market size was valued at USD 0.68 billion in 2025 and estimated to grow from USD 0.97 billion in 2026 to reach USD 5.74 billion by 2031, at a CAGR of 42.69% during the forecast period (2026-2031).

This report is Segmented by Component (Hardware, and Software), Technology (Sensor-Embedded Floor Tiles, Smart Heated Flooring, Energy-Harvesting Flooring, and More), End-User (Residential, Commercial, Industrial and Logistics, and More), Application (Occupancy and Space-Utilization Analytics, HVAC and Energy Management, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Smart Flooring Market Trends and Insights

Rapid Commercial Adoption for Occupancy Analytics in Office Spaces

Commercial real-estate operators are using floor-based sensing to narrow the gap between booked space and actual usage, and enterprise occupancy platforms continue to place that mismatch at 30-40% of total seat inventory. In the smart flooring market, this matters because floor sensing can deliver sub-square-meter resolution that badge systems and ceiling-mounted passive infrared devices do not. That sharper movement data helps facilities teams adjust layouts based on real usage patterns and also improves how occupancy information is fed into building management workflows. Demand-controlled HVAC programs become more effective when zone-level occupancy signals are continuous rather than binary, which strengthens the operating case for the smart flooring market in office environments. A Siemens-integrated deployment cited by Capgemini UK demonstrated how anonymized floor monitoring can support building operations without identifying individuals, a design principle becoming increasingly important to enterprise buyers. This makes occupancy analytics one of the fastest ways for the smart flooring market to convert technical capability into clear commercial value.

Rising Smart-Home Renovations and Retrofit Projects

Residential demand in the smart flooring market is rising faster than older smart-home adoption curves suggested because retrofit costs are becoming less tied to full renovation cycles. Modular formats and wireless control layers have made it easier for homeowners to add smart functionality without major construction disruption, which reduces dependence on contractor-led projects. This changes the purchase decision from a large capital project into a more manageable home upgrade, especially when comfort, heating control, and occupancy awareness are packaged together. Warmup launched its 7iE Smart Matter WiFi Thermostat in October 2025, with compatibility with Apple Home, Google Home, and Amazon Alexa, strengthening the connection between underfloor heating and mainstream connected-home ecosystems. The same launch stated that SmartGeo technology reduced energy consumption by up to 25% during use testing, helping address one of the main running-cost objections in the residential smart flooring market. As a result, smart heated flooring is emerging as a practical entry point for household adoption, especially in premium homes and retrofit-led renovations.

High Initial Installation and Calibration Costs

High upfront cost remains the clearest near-term restraint on the smart flooring market. Full-sensor floor systems were priced at USD 75-150 per square foot, compared with USD 15-40 per square foot for conventional carpet, and retrofit work added 40% premium due to subfloor modifications and cabling complexity. That cost gap limits adoption outside larger enterprises, healthcare networks, and public-sector budgets, even though the broader addressable base includes many mid-market buyers. Calibration adds another layer of friction because sensor arrays must be tuned for site-specific vibration, airflow, and equipment signatures, or false positives will reduce trust in the analytics output. Mitsubishi Estate's October 2025 demonstration with Aeterlink showed why wireless power matters for this category, since under-floor sensors that avoid cabling can reduce part of the installation burden in retrofit settings. Until retrofit-ready formats move closer to conventional flooring economics, cost will continue to shape which buyers can enter the smart flooring market at scale.

Other drivers and restraints analyzed in the detailed report include:

- Legal Mandates for Fall-Detection Systems in Senior-Care Facilities

- Energy Savings from Embedded Power-Management Algorithms

- Lack of Global Interoperability Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sensor-embedded floor tiles commanded a 44.38% share in 2025, maintaining their lead in the smart flooring market. Their position was driven by proven reliability, easier integration with existing commercial wiring infrastructure, and a better fit for the needs of office, healthcare, and retail projects. Buyers in these settings tend to prefer systems that already work with established installation practices, especially when deployment speed and maintenance simplicity affect payback. Smart heated flooring remains a distinct technology path in the smart flooring market because it addresses comfort, energy efficiency, and home automation simultaneously. Warmup's October 2025 7iE launch demonstrated how Matter-compatible controls can connect underfloor heating to major smart-home ecosystems, strengthening the appeal of heated flooring in premium homes and retrofit projects.

Energy-harvesting flooring is the fastest-growing technology segment, with a 44.57% CAGR projected through 2031, driven by falling material costs and improved power-management circuits that are advancing self-powered sensor nodes toward commercial viability. Research published in 2024 demonstrated a prototype tile capable of harvesting up to 246 mW per tile at a material cost of USD 10.20, demonstrating how quickly the economics are improving for high-footfall use cases. Additional work on low-cost battery-free smart pavement systems also supports the idea that power-generating surfaces are becoming more practical as wireless communication loads fall. ETH Zurich's LignoVolt project adds another dimension by embedding Rochelle salt crystals into modified wood to create recyclable piezo-parquet, bringing the smart flooring market into premium interior design and sustainability-led renovation conversations. Static-dissipative smart flooring and interactive LED flooring remain small niches, but they broaden the smart flooring market's technology base into electronics production, data centers, retail, and entertainment venues.

Hardware retained 65.53% of the smart flooring market share in 2025, while software is projected to expand at a 43.92% CAGR through 2031. That starting point reflected the physical nature of early deployments, because sensor carpets, gateway hubs, and edge processors formed the non-negotiable base layer of each installation. In the first phase of the smart flooring market, buyers had to fund the full data-collection stack before they could benefit from analytics, alerts, or building-system integration. This favored vendors that could deliver hardware, local compute, and installation support as one package, especially in commercial sites where reliability mattered more than modularity. It also meant that early revenue concentration sat with physical product suppliers rather than with recurring software providers.

Software is now gaining weight because analytics subscriptions, visualization tools, and building management APIs can be layered onto installed floors without another full construction cycle. That model matters for the smart flooring industry because it creates recurring revenue and improves lifetime value per square foot. It also changes margin structure, since declining sensor costs are likely to pressure hardware pricing over time while analytics remains more defensible. As the installed base grows, vendors that control occupancy dashboards, alert logic, and workflow integration are likely to hold a stronger commercial position than those that supply only hardware shells. The next stage of the smart flooring market will therefore depend on how successfully suppliers combine open interoperability with proprietary software value that customers are willing to keep paying for.

Geography Analysis

North America held 42.73% of the smart flooring market share in 2025, maintaining its leading regional position. The region benefits from a large base of enterprise technology buyers, active green-building enforcement, and healthcare systems that are already familiar with compliance-driven procurement. In the United States, nursing-facility requirements under CMS 42 CFR § 483.25(d) continue to support fall-prevention investment, which strengthens one of the most regulation-linked parts of the smart flooring market. Demand-controlled HVAC programs also improve the regional case for floor sensing because building operators can tie occupancy data to measurable energy savings and operating efficiency. Europe remained another important region in the smart flooring market, supported by building-efficiency rules under the Energy Performance of Buildings Directive and by the appeal of anonymous sensing approaches in privacy-sensitive workplace environments.

Asia-Pacific is projected to grow at a 44.54% CAGR through 2031, which makes it the fastest-expanding regional segment in the smart flooring market. China has already demonstrated commercial-scale use in office properties, where smart sensing floors are linked to lighting and HVAC systems, including a nearly 40% reduction in evening electricity consumption at Shoucheng International Center. Japan is a strong elder-care demand center, and Magic Shields reported deployment of its Koroyawa Sensor Mat III across 1,600 facilities by April 2026. India adds another source of demand through industrial-park modernization and wider adoption of smart buildings, giving the regional smart flooring market exposure to both commercial and industrial settings. South Korea, Australia, and New Zealand are also helping the regional mix through smart-city and connected-building programs that support sensor-led infrastructure upgrades.

South America, the Middle East, and Africa remained smaller parts of the smart flooring market, but they are strategically important because large infrastructure projects can quickly scale demand once procurement begins. Brazil and Argentina are still centered on commercial smart-building pilots, while South Africa is the clearest early adopter in African commercial real estate. In the Gulf, city-scale development programs are creating openings for kinetic and interactive flooring, and Pavegen has highlighted growing interest in energy-autonomous public-realm surfaces that can support urban infrastructure goals. Wider adoption across Turkey, Nigeria, Egypt, and similar markets will depend on sustained urban investment, reliable integration performance, and clearer evidence of payback at scale.

- SensingTex S.L.

- Pavegen Systems Ltd.

- Future-Shape GmbH

- Tarkett S.A.

- Mohawk Industries Inc.

- Shaw Industries Group Inc.

- Forbo Holding AG

- Interface Inc.

- Gerflor Group

- Beaulieu International Group

- Warmup PLC

- nVent Electric plc

- nora Systems GmbH

- Flowcrete Group Ltd.

- Sensora PLC

- Electroroute Ltd.

- Huawei Technologies Co. Ltd. (Smart Campus Flooring)

- ABB Ltd. (Motion and Smart Buildings Division)

- Siemens AG (Smart Infrastructure)

- Honeywell International Inc. (Building Technologies)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Smart-Home Renovations and Retrofit Projects

- 4.2.2 Rapid Commercial Adoption for Occupancy Analytics in Office Spaces

- 4.2.3 Legal Mandates for Fall-Detection Systems in Senior-Care Facilities

- 4.2.4 Energy Savings From Embedded Power-Management Algorithms

- 4.2.5 Maturing Printed Piezoelectric Materials Lowering BOM Costs

- 4.2.6 Urban Mobility Flooring Integration in Multi-Modal Transit Hubs

- 4.3 Market Restraints

- 4.3.1 Lack of Global Interoperability Standards

- 4.3.2 High Initial Installation and Calibration Costs

- 4.3.3 Data-Privacy Concerns Around Continuous Motion Sensing

- 4.3.4 Mechanical Durability Limits in Energy-Harvesting Tiles

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.2 By Technology

- 5.2.1 Sensor-Embedded Floor Tiles

- 5.2.2 Smart Heated Flooring (Electric and Hydronic)

- 5.2.3 Energy-Harvesting Flooring

- 5.2.4 Static-Dissipative / ESD Smart Flooring

- 5.2.5 Interactive LED / Visualization Flooring

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial and Logistics

- 5.3.4 Sports and Fitness Facilities

- 5.3.5 Public Infrastructure / Smart-City Installations

- 5.3.6 Other End-Users

- 5.4 By Application

- 5.4.1 Occupancy and Space-Utilization Analytics

- 5.4.2 Fall Detection and Elderly-Care Monitoring

- 5.4.3 HVAC and Energy Management

- 5.4.4 Security and Access Control

- 5.4.5 Customer Engagement and Wayfinding

- 5.4.6 Gaming and Interactive Entertainment

- 5.4.7 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Spain

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SensingTex S.L.

- 6.4.2 Pavegen Systems Ltd.

- 6.4.3 Future-Shape GmbH

- 6.4.4 Tarkett S.A.

- 6.4.5 Mohawk Industries Inc.

- 6.4.6 Shaw Industries Group Inc.

- 6.4.7 Forbo Holding AG

- 6.4.8 Interface Inc.

- 6.4.9 Gerflor Group

- 6.4.10 Beaulieu International Group

- 6.4.11 Warmup PLC

- 6.4.12 nVent Electric plc

- 6.4.13 nora Systems GmbH

- 6.4.14 Flowcrete Group Ltd.

- 6.4.15 Sensora PLC

- 6.4.16 Electroroute Ltd.

- 6.4.17 Huawei Technologies Co. Ltd. (Smart Campus Flooring)

- 6.4.18 ABB Ltd. (Motion and Smart Buildings Division)

- 6.4.19 Siemens AG (Smart Infrastructure)

- 6.4.20 Honeywell International Inc. (Building Technologies)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment