PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062087

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062087

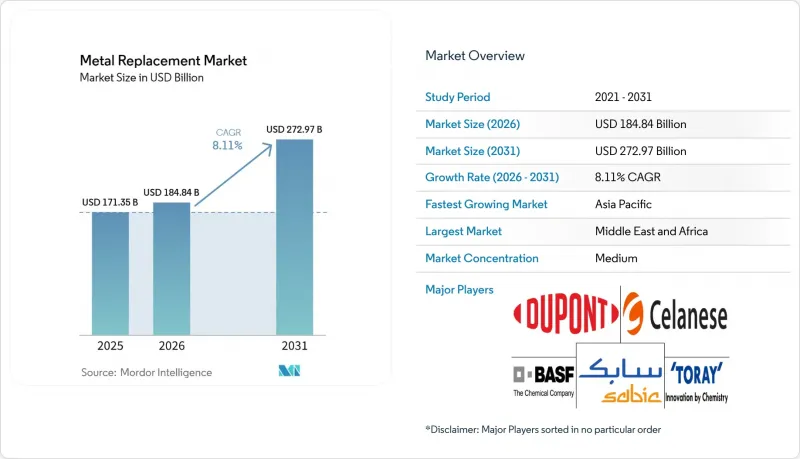

Metal Replacement - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the metal replacement market size is projected to be USD 171.35 billion in 2025, USD 184.84 billion in 2026, and reach USD 272.97 billion by 2031, growing at a CAGR of 8.11% from 2026 to 2031.

This report is Segmented by Material Type (Engineering Plastics and Composites), End-User Industry (Automotive, Aerospace and Defense, Industrial Equipment and Machinery, Construction and Infrastructure, Healthcare and Medical Devices, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Metal Replacement Market Trends and Insights

Growth in Automotive and Aerospace Lightweighting Trends

Battery-electric vehicles need to reduce 200-300 kg of chassis weight to offset the mass of lithium-ion batteries, leading automakers to replace underbody steel with glass-fiber polypropylene shields and carbon-fiber-reinforced thermoplastic battery enclosures that meet crash-worthiness standards while improving energy efficiency. Airbus validated a fully recyclable thermoplastic fuselage panel in 2025, which reduces manufacturing energy consumption by 40% compared to thermosets and allows for localized repairs, potentially lowering airline maintenance costs by 15-20% over a 25-year lifespan. Global wind-turbine capacity additions reached 117 GW in 2024, with composite blades now accounting for over 90% of rotor mass and reducing offshore foundation steel requirements by up to 40%. Hybrid carbon-glass designs approved by Sandia National Laboratories demonstrated a 44.7% increase in tensile strength, enabling rotor diameters to expand from 150 m to 180 m without proportional mass increases. Thermoplastic blades prototyped by Akelite in 2025 achieved an additional 7.3% weight reduction and full recyclability once standards are established.

Increasing Adoption of Engineering Plastics and Composites

Bio-based polyamide 11 captured 12% of the automotive under-hood market in 2025 after Arkema increased Rilsan PA11 production by 20% to meet EV cooling-line demand. Polyphenylene sulfide now holds 8% of the industrial pump housing market due to its acid resistance, which eliminates downtime previously costing operators USD 50,000-100,000 per incident. PEEK implants, despite being priced at a 15% premium over polycarbonate, have reduced spinal-fusion revision rates by 30%, saving USD 8,000-12,000 per patient. Carbon-fiber-reinforced PEEK screws demonstrated 25% greater pull-out strength than titanium in cadaveric tests, earning three new U.S. FDA clearances in 2025. Polyplastics' cellulose-fiber-blended PLASTRON LFT, launched in 2025, reduced the product carbon footprint by 30% while maintaining the impact strength required by global OEMs.

High Cost of Advanced Polymers and Composites

PEEK was priced at USD 60-80 per kg in 2025, eight to twelve times the cost of aluminum die-cast alloys, limiting its use in cost-sensitive applications such as appliances. Aerospace-grade carbon-fiber prepreg reached USD 150 per kg after a 12% increase in polyacrylonitrile feedstock prices, delaying composite adoption in secondary aircraft parts. Polyphenylene sulfide compounding requires USD 8-12 million twin-screw extruders, restricting supply to fewer than 20 global specialists. Flax and hemp composites reduce reinforcement costs by 30-40%, but their 8% moisture absorption causes dimensional drift, excluding them from precision applications like door modules. Recycled carbon fiber, priced at USD 15-25 per kg, has 20-30% lower tensile strength, limiting its use to non-structural products such as laptop shells.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of Electric-Vehicle Component Manufacturing

- Regulatory Push for Transportation Lightweighting

- Performance Limits in High-Stress/High-Temperature Uses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Engineering plastics accounted for 62.50% of the projected 2025 revenue, driven by the dominance of polyamide in under-hood components and the strength of polycarbonate in electronics housings. Composites are anticipated to grow at a 9.10% CAGR through 2031, as Asian carbon-fiber production reduces the cost gap to USD 20-25 per kg. The susceptibility of polycarbonate to hydrolysis is encouraging 5G antenna manufacturers to shift toward polyphenylene sulfide. ABS remains a cost-effective option for appliance shells at USD 3 per kg, but its 80 °C softening point limits its use to non-thermal applications. High-performance materials like PEEK, PEI, and PPS continue to reinforce their niche roles in medical and aerospace applications.

Glass-fiber-reinforced plastics, priced at USD 1.50-2.00 per kg, are widely used in automotive underbody shields and turbine housings. Carbon-fiber-reinforced systems remain essential for aerospace skins and premium EV body structures, despite their higher fiber cost of USD 25-40 per kg. Natural-fiber composites are primarily utilized in European door panels, valued for their lower embedded carbon. Toray has expanded French carbon-fiber production, while Hexcel's rapid-cure prepreg reduces autoclave cycles to two hours, helping thermosets maintain competitiveness against thermoplastics.

Geography Analysis

Asia-Pacific is expected to contribute 47.30% of 2025 revenue, driven by China's 6-8 Mt engineering plastics capacity and Japan's leadership in carbon-fiber precursor production. China hosts Mitsui Chemicals' long-glass-fiber polypropylene plant for EV battery trays, while Japan's Toray, Teijin, and Mitsubishi Chemical strengthen their aerospace-grade feedstock specialization. India is attracting new polymer investments as manufacturers diversify from China, and South Korea is piloting carbon-fiber recycling lines to meet China's 2028 mandate for 8% recycled fiber. ASEAN nations are gaining market share due to tariff concessions under RCEP and labor costs 30-40% lower than coastal China.

In North America, aerospace composites, Detroit's lightweighting initiatives, and wind-energy installations are supported by the U.S. Inflation Reduction Act's 30% manufacturing tax credit. BASF has increased polyisobutylene output by 60% at Ludwigshafen to meet EV battery-seal demand, while Canada's hydropower resources have attracted a 3,000-ton PAN-fiber plant with a 40% lower carbon footprint compared to coal-powered Chinese facilities. Mexico benefits from USMCA content rules favoring near-shoring of compounded resins.

Europe faces challenges from high energy costs but benefits from stringent 2030 CO2 targets, driving steel-to-polymer substitutions averaging 100 kg per passenger car. The Syensqo and Arkema HAICoPAS consortium secured EASA approval for a PEKK/carbon-fiber fuselage panel, reducing lay-up time from 8 hours to 45 minutes and enabling closed-loop repair pathways. The UK emphasizes recycling, with Hexcel and Lavoisier converting aerospace scrap into Carbonium reclaimed fabric at 40% lower cost than virgin materials. Nordic builders are adopting flax-fiber panels with half the embodied carbon of glass fiber. The Middle-East and Africa are forecast to achieve the highest CAGR of 9.07%, supported by Saudi Aramco and Syensqo's USD 30 billion investment in a vertically integrated compositing park.

- Arkema

- Asahi Kasei Corporation

- BASF

- Celanese Corporation

- Covestro AG

- DSM

- DuPont

- Ensinger

- Evonik Industries AG

- Hexcel Corporation

- Jushi Group

- LANXESS

- LG Chem

- Mitsubishi Chemical Group

- Owens Corning Corporation

- RTP Company

- SABIC

- SGL Carbon SE

- Solvay

- Sumitomo Chemical Co., Ltd.

- Teijin Aramid

- TORAY INDUSTRIES INC.

- Victrex plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in automotive and aerospace lightweighting trends

- 4.2.2 Increasing adoption of engineering plastics and composites

- 4.2.3 Rapid expansion of electric-vehicle component manufacturing

- 4.2.4 Regulatory push for transportation lightweighting

- 4.2.5 AI-driven topology optimisation enhancing polymer part design

- 4.3 Market Restraints

- 4.3.1 High cost of advanced polymers and composites

- 4.3.2 Performance limits in high-stress/high-temperature uses

- 4.3.3 Recycling and end-of-life challenges for multi-material parts

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Engineering Plastics

- 5.1.1.1 Polyamide (PA)

- 5.1.1.2 Polycarbonate (PC)

- 5.1.1.3 Acrylonitrile-Butadiene-Styrene (ABS)

- 5.1.1.4 Polyethylene Terephthalate (PET)

- 5.1.1.5 Polyphenylene Sulfide (PPS)

- 5.1.1.6 High-Performance Polymers (PEEK, PEI, etc.)

- 5.1.2 Composites

- 5.1.2.1 Glass Fibre-Reinforced Plastics (GFRP)

- 5.1.2.2 Carbon Fibre-Reinforced Plastics (CFRP)

- 5.1.2.3 Natural-Fibre Composites

- 5.1.1 Engineering Plastics

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Aerospace and Defense

- 5.2.3 Industrial Equipment and Machinery

- 5.2.4 Construction and Infrastructure

- 5.2.5 Healthcare and Medical Devices

- 5.2.6 Consumer Goods and Electronics

- 5.2.7 Energy and Utilities

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Arkema

- 6.4.2 Asahi Kasei Corporation

- 6.4.3 BASF

- 6.4.4 Celanese Corporation

- 6.4.5 Covestro AG

- 6.4.6 DSM

- 6.4.7 DuPont

- 6.4.8 Ensinger

- 6.4.9 Evonik Industries AG

- 6.4.10 Hexcel Corporation

- 6.4.11 Jushi Group

- 6.4.12 LANXESS

- 6.4.13 LG Chem

- 6.4.14 Mitsubishi Chemical Group

- 6.4.15 Owens Corning Corporation

- 6.4.16 RTP Company

- 6.4.17 SABIC

- 6.4.18 SGL Carbon SE

- 6.4.19 Solvay

- 6.4.20 Sumitomo Chemical Co., Ltd.

- 6.4.21 Teijin Aramid

- 6.4.22 TORAY INDUSTRIES INC.

- 6.4.23 Victrex plc

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Growth potential in electric-vehicle manufacturing