PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062088

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062088

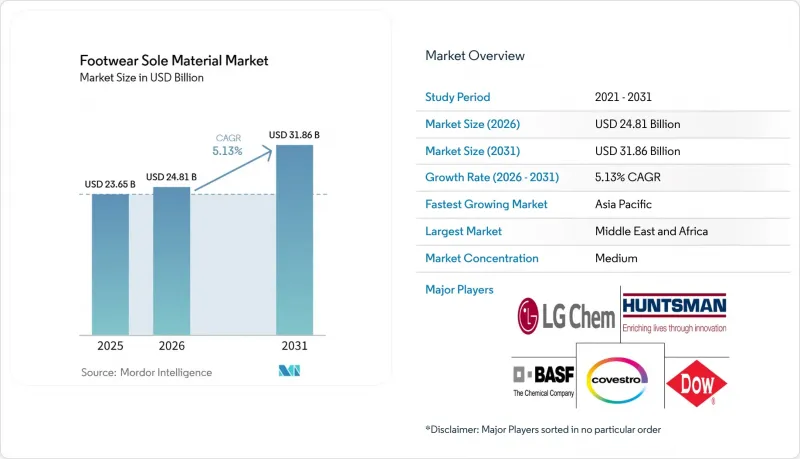

Footwear Sole Material - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the footwear sole material market size is projected to be USD 23.65 billion in 2025, USD 24.81 billion in 2026, and reach USD 31.86 billion by 2031, growing at a CAGR of 5.13% from 2026 to 2031.

This report is Segmented by Material Type (Polyurethane, Thermoplastic Rubber, and More), Manufacturing Process (Injection Moulding, Compression Moulding, Blow Moulding, and More), End-User Industry (Athletic and Sports, Casual and Fashion, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Footwear Sole Material Market Trends and Insights

Growing Global Footwear Output and Consumption

Worldwide production recovered to 23.9 billion pairs in 2024, reversing pandemic-induced declines and reflecting renewed consumer confidence across casual, athletic, and safety categories. Asia-Pacific factories in China, Vietnam, Indonesia, and India produced 88% of this volume and are now committing to minimum recycled-content thresholds in export collections, ensuring consistent demand for responsibly sourced pellets and polyols. Value-segment shoes priced below USD 250 continued to expand their market share in 2025, increasing cost pressures on compounders. Sole suppliers responded by reducing midsole gram-weights through higher-expansion foams and precision-metered molding. This production growth supports the footwear sole material market while pushing material producers toward leaner, performance-oriented formulations.

Rising Demand for Lightweight-Cushioning Compounds

Athletic brands have increased their adoption of energy-return foams. BASF's Infinergy expanded-bead TPU provides 55% rebound, enabling marathon-shoe manufacturers to offer reduced runner fatigue. Arkema's Pebax elastomers deliver stiffness-to-weight benefits for speed-focused racing shoes. Chinese sportswear company Li-Ning introduced nitrogen-infused TPU beads with an 82% energy return, giving domestic brands a competitive edge against global players. Concurrently, fashion trends favor ultra-thin ballerina-style sneakers, prompting polymer suppliers to maintain a wide range of density options. This diverse performance spectrum expands the addressable tonnage for the footwear sole material market while accommodating niche aesthetic preferences.

Petrochemical Raw-Material Price Volatility

Feedstocks such as ethylene, propylene oxide, and MDI experienced price spikes following early-2026 shipping disruptions in the Persian Gulf. Kraton raised polymer prices by USD 440-700 per tonne, LANXESS imposed surcharges of up to 50%, and Orion increased specialty carbon black prices by 25%. Footwear brands resisted passing these costs onto consumers, putting pressure on compounder margins. To address these challenges, strategies such as filler optimization, polymeric-MDI extension, and selective polyol substitution have been adopted, though these approaches risk compromising tensile strength. Covestro's integrated Zhuhai plant helps mitigate supply chain disruptions by internalizing TPU intermediates and securing downstream customers.

Other drivers and restraints analyzed in the detailed report include:

- Popularity Uptick in Sports/Athletic Footwear

- Automated Injection-Molding and Digital-Twin Adoption

- Environmental Scrutiny of Non-Biodegradable Soles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyurethane held 43.80% of the footwear sole material market share in 2025, attributed to its adaptability in hardness, excellent abrasion resistance, and ease of color customization. Ethylene-vinyl acetate continues to be a key material for lightweight midsoles, while thermoplastic rubber is widely used in children's and casual footwear. Natural and synthetic rubbers dominate oil-resistant work-boot outsoles. The fastest-growing category, which includes bio-based, recycled, and leather-alternative materials, is gaining traction due to initiatives like Arkema's tripling of castor-oil-based polyamide 11 capacity in Singapore and Soleic's launch of plant-based TPU, which reduces carbon emissions by 40% compared to traditional grades. As cost differences diminish, these materials could challenge polyurethane's dominance, altering the allocation of market share in the footwear sole material market.

The market for other material types is expected to grow at a 4.67% CAGR from 2026 to 2031, driven by the adoption of sugarcane-derived polyols and recycled EVA to meet European import regulations. However, the ability to scale feedstock availability and improve abrasion resistance will be critical for their application in high-wear segments like trail-running and industrial safety footwear.

Geography Analysis

The footwear sole material market size in Asia-Pacific amounted to 40.10% of total revenue in 2025. China's production benefits from the close integration of resin synthesis, compounding, and molding in coastal provinces. India's Production-Linked Incentive program supports EVA and TPU capacity expansion by subsidizing machinery investments. Vietnam aims to source 25% of sole inputs from recycled ocean plastics by mid-2026 to maintain access to European markets with strict eco-label requirements. Covestro's new TPU line in Zhuhai and BASF's elastomer expansion in Guangzhou strengthen regional feedstock security.

The Middle-East and Africa's footwear sole material market is projected to achieve the highest growth rate, with a 4.87% CAGR through 2031. African sneaker revenues reached USD 2.17 billion in 2024, with local brands like Bathu and Enda leveraging authentic storytelling to compete with multinational companies. However, the expiration of the African Growth and Opportunity Act in 2025 introduced U.S. tariffs of up to 32%, prompting a shift toward intra-African trade under AfCFTA and European markets.

North America and Europe emphasize sustainability and circular economy models. California's 2025 extended-producer-responsibility proposal could require brands to fund take-back programs, increasing demand for mono-material soles that simplify recycling. The EU's Product Environmental Footprint regulations are driving higher recycled-content thresholds, encouraging compounders to develop CQ-grade TPUs and castor-oil-based polyamides. South America remains a smaller market due to economic challenges, including currency fluctuations in Brazil and Argentina, which limit disposable income growth. However, domestic producers benefit from protective tariffs that support local manufacturing.

- Arkema

- Asahi Kasei Corp.

- BASF

- Celanese Corporation

- Coim Group

- Covestro AG

- Dow

- Evonik Industries AG

- Hexpol

- Huntsman International LLC

- KURARAY CO., LTD.

- LG Chem

- Lubrizol

- Mitsui Chemicals

- OrthoLite

- Solvay

- Teknor Apex

- Trelleborg AB

- Vibram Corporation

- Wanhua Chemical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing global footwear output and consumption

- 4.2.2 Rising demand for lightweight-cushioning compounds

- 4.2.3 Popularity uptick in sports/athletic footwear

- 4.2.4 Automated injection-moulding and digital-twin adoption

- 4.2.5 3-D printing enabling localised sole manufacture

- 4.3 Market Restraints

- 4.3.1 Petrochemical raw-material price volatility

- 4.3.2 Environmental scrutiny of non-biodegradable soles

- 4.3.3 Mechanical-performance gap in bio-based soles

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Polyurethane (PU)

- 5.1.2 Thermoplastic Rubber (TPR)

- 5.1.3 Ethylene-Vinyl Acetate (EVA)

- 5.1.4 Polyvinyl Chloride (PVC)

- 5.1.5 Rubber

- 5.1.6 Thermoplastic Polyurethane (TPU)

- 5.1.7 Other Material Types (Bio-based, Recycled, Leather, etc.)

- 5.2 By Manufacturing Process

- 5.2.1 Injection Moulding

- 5.2.2 Compression Moulding

- 5.2.3 Blow Moulding

- 5.2.4 Other Manufacturing Processes (3-D Printing, etc.)

- 5.3 By End-user Industry

- 5.3.1 Athletic and Sports Footwear

- 5.3.2 Casual and Fashion Footwear

- 5.3.3 Work and Safety Footwear

- 5.3.4 Slippers and Sandals

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Arkema

- 6.4.2 Asahi Kasei Corp.

- 6.4.3 BASF

- 6.4.4 Celanese Corporation

- 6.4.5 Coim Group

- 6.4.6 Covestro AG

- 6.4.7 Dow

- 6.4.8 Evonik Industries AG

- 6.4.9 Hexpol

- 6.4.10 Huntsman International LLC

- 6.4.11 KURARAY CO., LTD.

- 6.4.12 LG Chem

- 6.4.13 Lubrizol

- 6.4.14 Mitsui Chemicals

- 6.4.15 OrthoLite

- 6.4.16 Solvay

- 6.4.17 Teknor Apex

- 6.4.18 Trelleborg AB

- 6.4.19 Vibram Corporation

- 6.4.20 Wanhua Chemical

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Development of Sustainable and Recyclable Sole Materials