PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062089

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062089

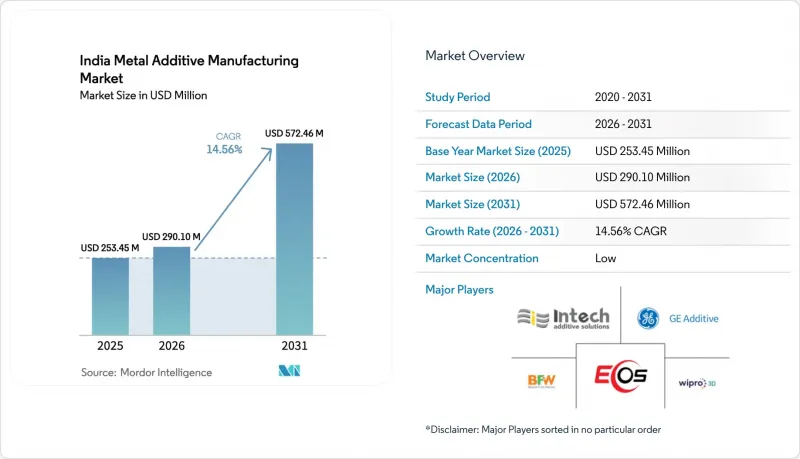

India Metal Additive Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india metal additive manufacturing market size was valued at USD 253.45 million in 2025 and is estimated to grow from USD 290.10 million in 2026 to reach USD 572.46 million by 2031, at a CAGR of 14.56% during the forecast period (2026-2031).

This report is Segmented by Technology (Powder Bed Fusion, Binder Jetting, More), Material Type (Stainless Steel, Aluminum, More), End-Use Industry (Aerospace and Defense, Automotive, Healthcare and Dental, Oil Gas and Energy, Tooling and Industrial Goods, Electronics and Semiconductors, Construction, Jewellery and Art), and Geography. Market Forecasts are Provided in Terms of Value in USD

India Metal Additive Manufacturing Market Trends and Insights

Growing Aerospace and Defense Indigenization Programs

Higher capital outlays and ringfenced domestic procurement are channeling demand for qualified metal AM components in air, land, and naval platforms across propulsion, structural, and thermal systems. Program announcements for next-generation aero engines elevate the role of printed injectors, liners, and complex cooling channels that benefit from repeatable powder-bed processes and robust post-processing. Mission timelines and platform upgrades tighten requirements for certified machines, powders, and heat treatment routes, which favors experienced service bureaus and integrators embedded in aerospace clusters. Standardization guidance aligned with ISO and ASTM practices is being adopted across airworthiness and naval classification pathways, which supports reliable series production of critical parts as test data matures. These shifts expand the opportunity space for the Indian metal additive manufacturing market by linking procurement pipelines to domestic qualification capacity.

Government's Make in India and Atmanirbhar Bharat Initiatives

The national roadmap places additive manufacturing among frontier technologies with significant GDP upside, outlining plug-and-play industrial parks and shared infrastructure that reduce entry barriers for capital-intensive metal printers. Policy measures emphasize indigenous machine development, localized materials, and a trained workforce so small and mid-sized firms can access advanced systems without prohibitive up-front costs. Competitive grants from the Technology Development Board further direct resources toward commercializing domestic metal and ceramics 3D printing technologies and enabler subsystems across the value chain. These interventions link procurement priorities with industrial capability-building, which accelerates qualification cycles for parts, machines, and materials aligned with national standards. The result for the Indian metal additive manufacturing market is a broader funnel of certified suppliers ready to serve regulated applications and time-bound projects.

Extremely High Equipment and Material Costs

Capital outlays for industrial-grade metal AM systems and their consumables remain high for the country's MSME base, which constrains adoption without access to shared infrastructure or pay-per-use models. Titanium powder pricing, combined with duties on specialty alloys, raises per-kilogram costs for aerospace-grade feedstocks relative to mature supply chains in other regions. Upstream moves to beneficiate ilmenite into titanium slag are building raw material resilience, yet downstream atomization capacity will take time to meet aerospace-grade sphericity and oxygen thresholds for powders. National plans for frontier-technology parks with shared equipment can reduce the burden, though the geographic spread of suppliers means localized service bureaus still matter for logistics and support. These cost and availability headwinds temper near-term penetration of the Indian metal additive manufacturing market in cost-sensitive end uses.

Other drivers and restraints analyzed in the detailed report include:

- Cost Advantages for Low-Volume and Complex Part Production

- Automotive Industry's Shift Toward Electric Vehicles

- Limited Availability of Qualified Metal Powders Domestically

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Powder Bed Fusion accounted for 45.87% of the installed base in 2025, reflecting airworthiness needs for sub-50-micron resolution and repeatability in turbine, injector, and thermal management parts validated through non-destructive evaluation and structured post-processing. This precision, combined with mature process controls and hot isostatic pressing routines, aligns with aerospace qualification flows that emphasize consistent microstructures and mechanical properties across complex geometries. Binder Jetting is the fastest-growing technology at a projected 15.78% CAGR to 2031, sustained by economics in tooling and medium-volume parts where sintering and infiltration deliver acceptable properties for automotive and industrial buyers. Directed Energy Deposition supports repair and remanufacture use cases, including blade-tip restoration and on-site or near-site part reinforcement, which shortens downtime for engines and shipboard systems. Technology selection correlates with certification readiness, so qualification frameworks favor PBF for flight hardware today while Binder Jetting expands in cost-sensitive applications as datasets mature.

Adoption patterns also mirror national R&D priorities for lattice structures, conformal cooling, and build-parameter optimization that raise first-time-right rates and cut rework. This strengthens the opportunity in the Indian metal additive manufacturing market, where tooling amortization would otherwise hinder complex, low- to mid-volume runs. Within technology choices, the Indian metal additive manufacturing market share for PBF benefits from airworthiness and classification guidance aligned with ISO and ASTM, while Binder Jetting's qualification playbook continues to evolve on material systems and sintering repeatability. As certification data accumulates for electron-beam variants, wire-arc routes, and hybrid platforms, multi-technology facilities can tailor processes to part function and lifecycle requirements. These certification-driven choices are reshaping go-to-market strategies for both OEMs and service bureaus in India's regional clusters.

List of Companies Covered in this Report:

- Wipro 3D

- Intech Additive Solutions

- Bharat Fritz Werner (BFW Additive)

- GE Additive (India)

- EOS India

- 3D Systems India

- SLM Solutions

- Phillips Additive/Phillips Machine Tools

- Objectify Technologies

- 3D Incredible

- Imaginarium Rapid

- Truventor.ai (Supercraft3D)

- BASF Forward AM India

- Indo-MIM

- Agnikul Cosmos

- Godrej Aerospace

- Tata Advanced Systems

- Bharat Forge

- L&T Technology Services

- HP Metal Jet (India)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government's Make in India and Atmanirbhar Bharat Initiatives

- 4.2.2 Growing Aerospace and Defense Indigenization Programs

- 4.2.3 Expansion of India's Space Program

- 4.2.4 Rising Demand for Customized Medical Implants and Prosthetics

- 4.2.5 Automotive Industry's Shift Toward Electric Vehicles

- 4.2.6 Cost Advantages for Low-Volume and Complex Part Production

- 4.3 Market Restraints

- 4.3.1 Extremely High Equipment and Material Costs

- 4.3.2 Limited Availability of Qualified Metal Powders Domestically

- 4.3.3 Lack of Standardization and Quality Certification Frameworks

- 4.3.4 Insufficient Awareness Among Traditional Manufacturing Sectors

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Tier-Based Adoption Pattern Across Indian Industry

- 4.9 Regional Concentration Around Aerospace and Automotive Clusters

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Technology

- 5.1.1 Powder Bed Fusion (PBF)

- 5.1.2 Binder Jetting

- 5.1.3 Directed Energy Deposition (DED)

- 5.1.4 Other Metal AM Processes

- 5.2 By Material Type

- 5.2.1 Stainless Steel

- 5.2.2 Aluminum

- 5.2.3 Titanium

- 5.2.4 Cobalt Chrome

- 5.2.5 Nickel Alloys

- 5.2.6 Precious Metals (e.g., gold, silver, platinum)

- 5.2.7 Others (custom alloys, high-temp superalloys)

- 5.3 By End-Use Industry

- 5.3.1 Aerospace & Defence

- 5.3.2 Automotive

- 5.3.3 Healthcare & Dental

- 5.3.4 Oil, Gas & Energy

- 5.3.5 Tooling & Industrial Goods

- 5.3.6 Electronics & Semiconductors

- 5.3.7 Construction

- 5.3.8 Jewellery & Art

- 5.4 By Region

- 5.4.1 North India (Delhi, Haryana, UP, Punjab)

- 5.4.2 West India (Maharashtra, Gujarat, Goa)

- 5.4.3 South India (Karnataka, Tamil Nadu, Telangana, Kerala)

- 5.4.4 East & North-East India

- 5.4.5 Central India (MP, Chhattisgarh)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves & Partnerships

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Wipro 3D

- 6.4.2 Intech Additive Solutions

- 6.4.3 Bharat Fritz Werner (BFW Additive)

- 6.4.4 GE Additive (India)

- 6.4.5 EOS India

- 6.4.6 3D Systems India

- 6.4.7 SLM Solutions

- 6.4.8 Phillips Additive/Phillips Machine Tools

- 6.4.9 Objectify Technologies

- 6.4.10 3D Incredible

- 6.4.11 Imaginarium Rapid

- 6.4.12 Truventor.ai (Supercraft3D)

- 6.4.13 BASF Forward AM India

- 6.4.14 Indo-MIM

- 6.4.15 Agnikul Cosmos

- 6.4.16 Godrej Aerospace

- 6.4.17 Tata Advanced Systems

- 6.4.18 Bharat Forge

- 6.4.19 L&T Technology Services

- 6.4.20 HP Metal Jet (India)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment