PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062098

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062098

Agro-Rural Tourism - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

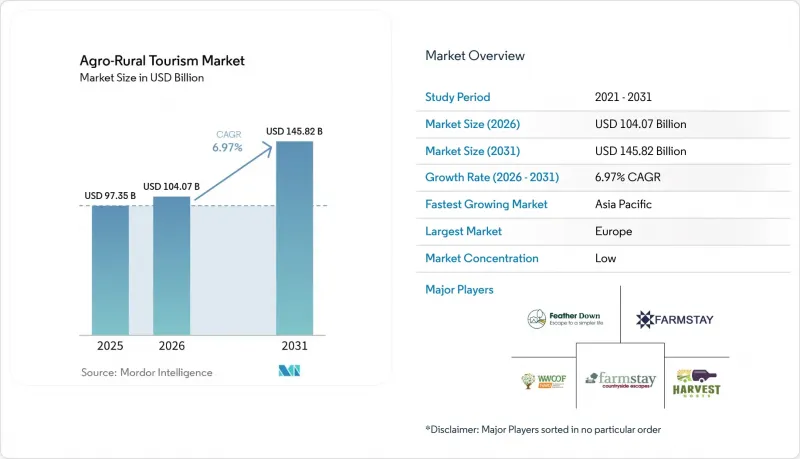

According to Mordor Intelligence, the agro-Rural tourism market was valued at USD 97.35 billion in 2025 and is estimated to grow from USD 104.07 billion in 2026 to reach a higher valuation by 2031, at a CAGR of 6.97% during the forecast period (2026-2031).

This report is Segmented by Tourism Type (Agri-Stay, Agri-Education, and More), Booking Channel (Direct, Online, and More), Tourist Type (Domestic Tourists and International Tourists), Revenue Source (Accommodation, Activities & Experiences, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Agro-Rural Tourism Market Trends and Insights

Rising preference for immersive and experience-led travel

Participatory farm experiences that combine education, local food, and nature are gaining popularity, with activities like guided harvests, tastings, and producer workshops drawing families and school groups to accredited farms during peak periods. Structured tastings and educational farm programs have become standard in leading European regions, while Saudi Arabia focuses on hands-on produce picking and farm education to ensure year-round engagement under its national diversification strategy. Public programs are integrating farms into procurement networks for hotels and cruise operators, creating steady demand for accredited sites. To attract remote professionals, operators are offering packages that combine nature, wellness, and flexible work amenities, catering to those seeking quiet rural settings with reliable connectivity for extended stays during off-peak periods.

Increasing policy support for rural tourism through government subsidy programs

Targeted incentives are reducing entry barriers and operating costs for farm-based stays and experiences by supporting rural operators through investment schemes, grants, and subsidies. Programs like Scotland's initiative and sector census highlight increased business numbers, strong visitor turnout, and opportunities for capital inflows beyond traditional accommodation. Ireland promotes agri-food tourism with capped grants for developing tasting rooms, trails, and visitor facilities aligned with national standards. In India, Maharashtra and Arunachal Pradesh combine subsidies, concessional tariffs, and certifications to lower costs while ensuring sustainability and safety. Additionally, infrastructure projects, such as Ireland's Outdoor Recreation Infrastructure Scheme, enhance rural visitor flows by connecting farms to walking and cycling networks.

Inadequate infrastructure and accessibility challenges in rural regions

Aging rail and road networks in Europe hinder rural access, as station closures and delayed upgrades reduce mass-transit options to agritourism areas, increasing reliance on private vehicles and limiting inclusive visitation. In India, poor accommodation availability, inadequate road quality, and limited access to electricity and internet are significant barriers, rated as severe by operators, and reducing demand for higher-value international bookings. Sri Lankan surveys show most agritourism sites lack proper roads and visitor facilities, creating a revenue-capital cycle that delays improvements. In the United States, essential infrastructure requirements and the distance to emergency care raise financial and safety challenges for small farms, underscoring the need for clear hygiene and safety measures .

Other drivers and restraints analyzed in the detailed report include:

- Growing need for income diversification among farming communities

- Rapid expansion of digital booking platforms for short-duration rural stays

- Strong seasonality impacting occupancy rates and revenue stability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The agri-stay (farm accommodation) segment accounted for 38.42% of the Agro-Rural Tourism market, driven by demand for immersive rural lodging experiences that combine accommodation with food, wine, cultural heritage, and educational farm activities. This segment benefits from established rural tourism ecosystems in mature destinations, where farms are integrated into hospitality networks offering structured packages. These packages attract domestic and international travelers seeking short-stay, nature-connected experiences near urban centers. Seasonal travel patterns, weekend tourism flows, and repeat visits tied to festivals, harvest cycles, and curated farm-to-table experiences contribute to high occupancy rates, enhancing revenue stability and reinforcing the segment's leadership.

The "Others" segment, including agri-volunteer programs, agri-wellness retreats, and similar offerings, is projected to grow at a CAGR of 8.94% through 2031. Growth is driven by demand for non-traditional rural engagement formats such as farm volunteering, experiential workshops, yoga retreats, and nature-based therapy activities that emphasize mental well-being and skill-based participation. Consumer preference for meaningful travel experiences encourages farms to diversify offerings, enabling deeper visitor engagement through hands-on agricultural activities such as harvesting, animal care, and sustainable farming education. Wellness-oriented agritourism is gaining popularity as travelers associate rural environments with stress reduction, healthier lifestyles, and digital detox opportunities. Policy support for rural development, integration of farms into local tourism circuits, and collaboration with educational institutions boost weekday demand and utilization rates. Seasonal and event-driven programming enhances revenue concentration, allowing operators to optimize pricing and invest in off-peak innovations. These factors are transforming the agro-rural tourism market into a more experience-driven, diversified, and high-value ecosystem.

Many farm owners prioritize commission-free sales and maintain relationships with repeat guests, leading to direct bookings accounting for 44.15% of transactions in 2025. In Europe, agritourism transactions largely occur directly, though digital discovery driven by local food, wine, and nature experiences is growing, with bookings often made via phone or farm websites. Social media and community platforms are forecast to grow at a 9.97% CAGR through 2031, supported by visual discovery tools and peer networks that highlight authenticity and uncover lesser-known farms. Specialist platforms enable farms to manage reservations independently with listing scalability and white-label tools, avoiding high OTA commissions and preserving profitability. Integrated ecosystems now combine membership options, campground searches, and farm host services, simplifying trip planning and expanding the rural tourism customer base. General OTAs focus on tours and tastings rather than accommodations, leaving room for specialist platforms or direct channels to maintain market share in room bookings and extended-stay packages. Social discovery integrations with RV ownership, route planning, and host networks continue to benefit the agro-rural tourism market, with partnerships enhancing inventory and filtering options like vehicle length and access rules. Traditional agencies curate group itineraries for agricultural education and farm-to-table programs, appealing to international travelers seeking multi-farm routes and consistent standards. A digital divide persists in emerging markets, where limited online presence hinders structured bookings. Over time, unified membership platforms, direct farm booking engines, and niche discovery portals are expected to coexist, emphasizing authenticity and direct relationships while leveraging platform-enabled reach.

Geography Analysis

Europe is projected to hold the largest regional share at 37.50% in 2025, driven by strong agritourism capacity, diverse food and wine offerings, and sustained domestic and intra-regional travel, which support high seasonal occupancy. Growth is reinforced by expansion of licensed tasting rooms, educational farms, and coordinated rural infrastructure, while Southern Europe and island regions are expanding faster than saturated northern markets, indicating supply rebalancing and destination diversification. Spain's enotourism model and European Union-supported outdoor infrastructure further enhance rural accessibility and the integration of nature-based travel. Asia-Pacific is the fastest-growing region with a 10.51% CAGR through 2031, supported by policy-led rural tourism integration, subsidy programs, and structured farm tourism development in China, India, the Philippines, and Vietnam, where accreditation systems and supply-chain linkages are improving standards. North America shows a hybrid structure of fragmented operators and consolidating digital platforms, supported by state-level funding and RV-based membership ecosystems. The Middle East is developing integrated agritourism hubs combining farms, hospitality, and retail, while South Africa is expanding visibility through national platforms. Across regions, growth is shaped by safety standards, sustainability expectations, and digital discovery systems. The competitive landscape remains fragmented at operator level, while platforms increasingly consolidate discovery and bookings. Opportunities are emerging in underserved rural areas, digital coliving models, and midweek demand optimization, balancing local ownership with platform-led scalability.

- Feather Down Farms

- Harvest Hosts

- Farm Stay USA

- WWOOF International

- Farm Stay UK

- Agritours Italy

- AgriTours NZ

- Responsible Travel

- FarmHouse Inns

- Agritourism Limited

- EcoColors Tours

- Greenhorns

- Rural Escapes

- Agriliving

- FarmAdventure

- Countryside Holidays

- Agri-Experience Japan

- Stay on a Farm Australia

- Agritourismo Brazil

- Cape AgriTours

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising preference for immersive and experience-led travel

- 4.2.2 Increasing policy support for rural tourism through government subsidy programs

- 4.2.3 Growing need for income diversification among farming communities

- 4.2.4 Rapid expansion of digital booking platforms for short-duration rural stays

- 4.2.5 Increasing consumer inclination toward sustainable and carbon-conscious travel experiences

- 4.2.6 Emergence of rural locations as attractive hubs for remote workers and long-stay travelers

- 4.3 Market Restraints

- 4.3.1 Inadequate infrastructure and accessibility challenges in rural regions

- 4.3.2 Strong seasonality impacting occupancy rates and revenue stability

- 4.3.3 Stringent biosecurity and agricultural compliance requirements

- 4.3.4 Persistent concerns around health, hygiene, and animal-human interaction risks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Tourism Type

- 5.1.1 Agri-stay (farm accommodation)

- 5.1.2 Agri-education (classes & tours)

- 5.1.3 Agri-recreation (outdoor activities)

- 5.1.4 Agri-events & festivals

- 5.1.5 Others (Agri-volunteer (WWOOF, farm work) Agri-wellness (yoga retreats, nature therapy))

- 5.2 By Booking Channel

- 5.2.1 Direct (farm website / phone)

- 5.2.2 Online Travel Agencies (OTAs)

- 5.2.3 Traditional Travel Agencies

- 5.2.4 Social-media / community platforms

- 5.3 By Travelers Type

- 5.3.1 Domestic Tourists

- 5.3.2 International Tourists

- 5.4 By Revenue Source

- 5.4.1 Accommodation

- 5.4.2 Activities & Experiences

- 5.4.3 Food & Beverage

- 5.4.4 Retail (farm shop, crafts)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 Canada

- 5.5.1.2 United States

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX

- 5.5.3.7 NORDICS

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South-East Asia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East & Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East & Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Feather Down Farms

- 6.4.2 Harvest Hosts

- 6.4.3 Farm Stay USA

- 6.4.4 WWOOF International

- 6.4.5 Farm Stay UK

- 6.4.6 Agritours Italy

- 6.4.7 AgriTours NZ

- 6.4.8 Responsible Travel

- 6.4.9 FarmHouse Inns

- 6.4.10 Agritourism Limited

- 6.4.11 EcoColors Tours

- 6.4.12 Greenhorns

- 6.4.13 Rural Escapes

- 6.4.14 Agriliving

- 6.4.15 FarmAdventure

- 6.4.16 Countryside Holidays

- 6.4.17 Agri-Experience Japan

- 6.4.18 Stay on a Farm Australia

- 6.4.19 Agritourismo Brazil

- 6.4.20 Cape AgriTours

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment