PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062105

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062105

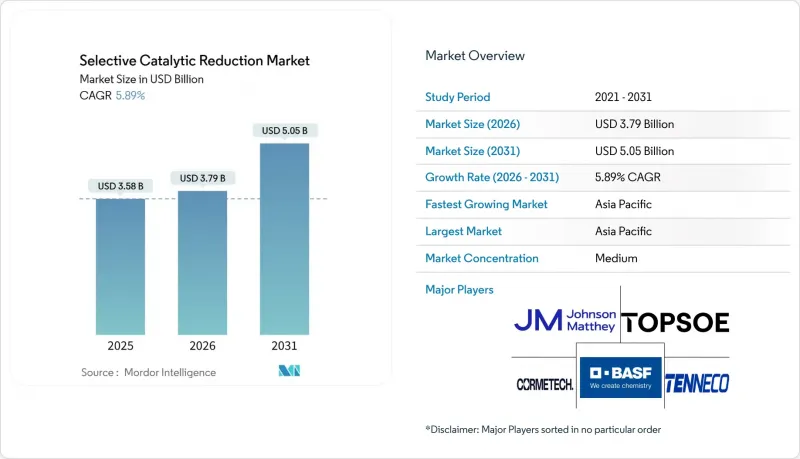

Selective Catalytic Reduction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the selective catalytic reduction market size is expected to grow from USD 3.58 billion in 2025 to USD 3.79 billion in 2026 and is forecast to reach USD 5.05 billion by 2031 at 5.89% CAGR over 2026-2031.

This report is Segmented by Type (High Dust SCR, Low Dust SCR, and Tail-End SCR), Application (Power Generation, Industrial Boilers and Furnaces, Cement and Lime Kilns, Chemicals and Petrochemicals, Automotive - Light-Duty, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Selective Catalytic Reduction Market Trends and Insights

Surge in Marine SCR Retrofits Ahead of IMO Tier III

Tier III rules require an 80% NOx cut, driving owners to retrofit SCR on vessels that enter Emission Control Areas. The 2025 designation of the Norwegian Sea and Canadian Arctic widened compliance zones and generated a backlog exceeding 3,000 vessels. Cruise operators moved fastest, fitting 81 ships with SCR by 2025, up from 7 in 2018. Retrofit costs run USD 1.5-4 million per ship, but new engines such as WinGD's X-DF-HP integrate SCR from the factory, trimming total cost of ownership by 15%. As more Tier III-ready tonnage is delivered post-2028, retrofit demand will cool, yet catalyst replacement will stay resilient through the 2030s.

Rapid Build-Out of Coal-to-Chemicals Plants in Asia-Pacific

China's Shaanxi Coal Yulin complex embeds SCR to meet the 50 mg/Nm3 NOx cap, a precedent for other mega-projects. India's 100-ton coal-gasification mission follows suit, but higher sulfur coal accelerates catalyst poisoning, inflating lifecycle cost. The public-health imperative remains clear, with studies showing SCR deployment could avert up to 210,000 premature deaths over a decade.

Accelerating Electrification of Light-Duty Vehicles

Global BEV (battery electric vehicle) sales topped 14 million in 2025, displacing diesel engines that drove aftermarket SCR catalyst sales. Euro 7 rules, effective 2027, tighten limits further but favor zero-tailpipe options, prompting Johnson Matthey to cut Platinum Group Metal (PGM) loadings 20% to defend share. Heavy-duty regulations in the U.S. will cushion demand until fuel-cell and battery trucks scale after 2030.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Low-Temperature Vanadium-Ceria Catalysts in Cement Kilns

- OEM Validation of SCR for Hydrogen-Fuelled Engines

- SO2/SO3 Poisoning Shortening Catalyst Life

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-Dust systems captured 45.12% of the Selective Catalytic Reduction market share in 2025. Operating upstream of particulate filters lets these units stay within 300-420°C, avoiding reheating but demanding erosion-resistant channels. CORMETECH's Dustbuster modules highlight such design features. Tail-End SCR, favored by gas turbines and marine engines, is expected to grow at the fastest CAGR of 6.18% during the forecast period (2026-2031) as low-temperature catalysts mature. The Selective catalytic reduction market size for Tail-End installations is projected to exceed USD 1 billion by 2031.

Continued catalyst advances will decide growth tempo. Trials of 3% V2O5-10 % MoO3/TiO2 show more than 67% average removal at 160-180°C over two years, while CERI's heat-free design achieved more than 90% removal at 120-140°C. Yet ammonium bisulfate fouling below 200°C remains a constraint for operators.

Geography Analysis

Asia-Pacific accounted for 51.25% of the Selective Catalytic Reduction market share in 2025 and is set to expand at 6.29% CAGR to 2031. China's 50 mg/Nm3 industrial cap embeds SCR in every new coal-to-chemicals line, while India's 100-ton gasification mission mirrors this pathway. Higher sulfur coal in India raises catalyst cost but also cements FGD retrofits. Japan's 800,000 tons per year low-carbon ammonia contracts point to early deployment of ammonia-fired turbines that will need to be tailored.

In North America, the EPA 2027 heavy-duty rule propels on-road demand, and combined-cycle retrofits keep utility orders flowing. Kentucky regulators highlighted a finished SCR project that closed under budget, informing cost expectations for new gas units. Canadian Arctic ECA status pushes vessel retrofits, but cold climate imposes urea-handling challenges.

In Europe, coal retirements dampen utility orders, yet the Industrial Emissions Directive's 200 mg/Nm3 limit for new cement kilns underpins low-temperature catalyst uptake. The 2025 Norwegian Sea ECA extended marine compliance northward, driving ferry and cruise retrofits. Honeywell's bid for Johnson Matthey reflects a consolidating regional supplier base.

- Babcock and Wilcox Enterprises Inc.

- BASF

- CLARIANT

- CORMETECH

- Dongfang Boiler Ltd

- DUCON

- FORVIA HELLA

- GE Vernova

- Hitachi Zosen India Private Limited

- Johnson Matthey

- MITSUBISHI HEAVY INDUSTRIES, LTD.

- Shandong Longking

- Siemens Energy

- Tenneco Inc

- Topsoe A/S

- Umicore

- YANMAR Marine International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in marine SCR retrofits ahead of IMO Tier III

- 4.2.2 Rapid build-out of coal-to-chemicals plants in Asia-Pacific

- 4.2.3 Adoption of low-temperature vanadium-ceria catalysts in cement kilns

- 4.2.4 OEM validation of SCR for hydrogen-fuelled engines

- 4.2.5 AI-driven adaptive ammonia injection controls

- 4.3 Market Restraints

- 4.3.1 Accelerating electrification of light-duty vehicles

- 4.3.2 SO2/SO3 poisoning shortening catalyst life

- 4.3.3 Regulatory ambiguity around blue-ammonia bunkering

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 High Dust SCR

- 5.1.2 Low Dust SCR

- 5.1.3 Tail-End SCR

- 5.2 By Application

- 5.2.1 Power Generation (Coal, Gas, and Biomass)

- 5.2.2 Industrial Boilers and Furnaces

- 5.2.3 Cement and Lime Kilns

- 5.2.4 Iron and Steel

- 5.2.5 Chemicals and Petrochemicals

- 5.2.6 Automotive - Light-duty

- 5.2.7 Automotive - Heavy-duty (On-road)

- 5.2.8 Marine Engines

- 5.2.9 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Babcock and Wilcox Enterprises Inc.

- 6.4.2 BASF

- 6.4.3 CLARIANT

- 6.4.4 CORMETECH

- 6.4.5 Dongfang Boiler Ltd

- 6.4.6 DUCON

- 6.4.7 FORVIA HELLA

- 6.4.8 GE Vernova

- 6.4.9 Hitachi Zosen India Private Limited

- 6.4.10 Johnson Matthey

- 6.4.11 MITSUBISHI HEAVY INDUSTRIES, LTD.

- 6.4.12 Shandong Longking

- 6.4.13 Siemens Energy

- 6.4.14 Tenneco Inc

- 6.4.15 Topsoe A/S

- 6.4.16 Umicore

- 6.4.17 YANMAR Marine International

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment