PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062113

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062113

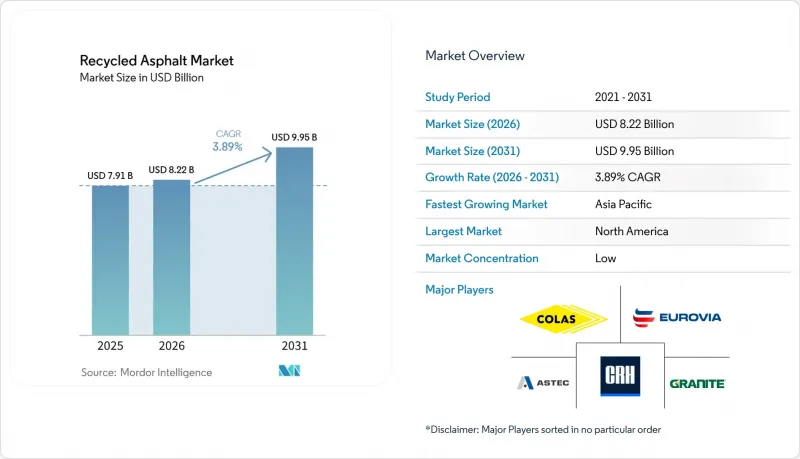

Recycled Asphalt - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the recycled asphalt market size is projected to expand from USD 7.91 billion in 2025 and USD 8.22 billion in 2026 to USD 9.95 billion by 2031, registering a CAGR of 3.89% between 2026 to 2031.

This report is Segmented by RAP Content Level (Low RAP Content (Less Than or Equal To 20%), Medium RAP Content 21-50%, and More), Recycled Asphalt Application (Patch Material, Hot Mix Asphalt, and More), End-User Industry (Commercial, Industrial, Municipal), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Recycled Asphalt Market Trends and Insights

Cost Competitiveness of RAP Versus Virgin Mixes

The National Asphalt Pavement Association reported USD 3.4 billion in U.S. producer savings in 2023 through the use of 96.1 million tons of Reclaimed Asphalt Pavement (RAP) at an average inclusion rate of 21.9%. This demonstrates the role of RAP in managing raw material costs. Field data from the Florida Department of Transportation indicated that RAP-rich pavements provide comparable performance at a lower delivered cost in subtropical climates. Cost advantages increase during crude oil price rises; for example, when Brent crude exceeds USD 85 per barrel, the price difference between virgin and reclaimed binder can double. This has enabled contractors in India to achieve cost reductions of 25-30% on highway projects. Furthermore, municipal budget limitations support RAP adoption, making its usage less influenced by fluctuations in virgin asphalt demand.

Stringent Sustainability Procurement Mandates By DOTs And Municipalities

California's Assembly Bill 2953, New Jersey's Public Law 2023 c.134, Colorado's Buy Clean Act, and Minnesota's 2025 EPD rule require bidders to document carbon intensity, integrating reclaimed asphalt content into all qualifying projects. Non-compliance penalties include measures such as contract holdbacks and disqualification, establishing a compliance baseline that ensures consistent demand regardless of crude oil price fluctuations. These regulations support suppliers that have invested in life-cycle assessment tools.

Fragmented Logistics and Stockpile Management For RAP

Moisture absorption, contamination, and variability in gradation impact the performance margins of Reclaimed Asphalt Pavement (RAP) and increase blending costs. Many public storage facilities lack fractionation and protective covering, leading Departments of Transportation (DOTs) to limit RAP content to 20-30% unless additional laboratory testing is conducted. Investments in covered storage, on-site screening, and continuous sampling are essential for the recycled asphalt market to achieve its high-RAP potential.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of 100%-RAP And Warm-Mix Plant Technologies

- Corporate Net-Zero Targets Spurring Carbon-Negative Pavement Credits

- Emergent Microplastics Scrutiny on Recycled Pavement Runoff

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, low RAP content (less than or equal to 20%) held the largest share of the recycled asphalt market. This is due to most DOT standards relying on legacy performance data. These mixes provide consistent compaction and are compatible with unmodified batch plants, reducing adoption risks. Medium RAP blends (21-50%) have seen increased usage due to dual-bin feed retrofits and advancements in rejuvenator chemistries, offering balanced fatigue resistance at a competitive cost.

High RAP content (greater than 50%) is expected to lead the recycled asphalt market with a 3.98% CAGR through 2031. Initiatives such as Eurovia's 100% RAP motorway trial and Astec's ReMix CCPR plant have demonstrated field feasibility. Furthermore, the introduction of ternary composite rejuvenation in 2026 addressed earlier concerns regarding low-temperature brittleness. Project bids incorporating at least 40% RAP now qualify for additional scoring credits in several U.S. states, prompting specifiers to reassess the cost-risk balance. Contractors investing in fractionation and automated dosage controls are positioned to expand this segment into a profitable market opportunity.

Geography Analysis

Asia-Pacific is projected to grow at a CAGR of 4.41% through 2031. China produces approximately 200 million tons of Reclaimed Asphalt Pavement (RAP) annually, but reuses only 30%, indicating potential for increased recycling as GB/T25033 supports hot, warm, and cold recycling methods. In India, over 63 million tons of waste were reused in FY 2023-24 across 6,634 kilometers of highways, with several states testing 40% RAP surface courses. Japan, with a 99% pavement recycling rate, has advanced collection logistics, while new PWRI test methods aim to validate mixes containing up to 70% reclaimed binder. Australia and South Korea currently maintain capped reuse levels but face fiscal considerations to increase thresholds.

North America: Market Share Driven by Policy and Cost Savings. North America accounted for 41.89% of the recycled asphalt market in 2025. In 2023, U.S. contractors saved USD 3.4 billion in material costs by utilizing 96.1 million tons of RAP. State regulations, such as California AB 2953 and Colorado's Buy Clean Act, mandate Environmental Product Declarations, while balanced mix design pilots are increasing allowable RAP percentages to 45-50%. Training partnerships between Wirtgen and state Departments of Transportation (DOTs) are enhancing operator skills for on-site cold recycling processes.

Europe recycled 95% of its 100 million-ton RAP output in 2024, driven by landfill bans and carbon taxes. France's A10 trial validated the use of 100% RAP in highway layers, while Colas expanded its recycling capabilities in Germany, Europe's largest road market, through the acquisition of Frauenrath. These developments reflect Europe's focus on sustainable road construction practices.

South America and the Middle East & Africa are smaller but growing markets. In Brazil, cold recycling systems were incorporated into Sao Paulo's urban infrastructure upgrades. Saudi Arabia approved the use of 25% RAP for national highways. Infrastructure stimulus budgets and circular-economy policies in these regions indicate a gradual increase in recycling adoption.

- Allan Myers, Inc.

- Apollo Asphalt Reclaimers LLC

- Astec Industries

- Colas

- CRH

- Eurovia (VINCI)

- Granite Construction Inc.

- MARINI FAYAT GROUP

- Martin Marietta

- MR Roads

- necoTECH

- Superpave Engineering Inc.

- WIRTGEN INDIA Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost competitiveness of RAP versus virgin mixes

- 4.2.2 Stringent sustainability procurement mandates by DOTs and municipalities

- 4.2.3 Expansion of 100 %-RAP and warm-mix plant technologies

- 4.2.4 Corporate net-zero targets spurring carbon-negative pavement credits

- 4.2.5 Secondary materials trading platforms unlocking high-quality RAP supply

- 4.3 Market Restraints

- 4.3.1 Fragmented logistics and stockpile management for RAP

- 4.3.2 Emergent microplastics scrutiny on recycled pavement runoff

- 4.3.3 Volatility of bitumen-rejuvenator additive pricing

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By RAP Content Level

- 5.1.1 Low RAP Content (Less than or Equal to 20 %)

- 5.1.2 Medium RAP Content (21-50 %)

- 5.1.3 High RAP Content (Greater than 50 %)

- 5.2 By Recycled Asphalt Application

- 5.2.1 Patch Material

- 5.2.2 Hot Mix Asphalt

- 5.2.3 Temporary Driveways and Roads

- 5.2.4 Road Aggregate

- 5.2.5 Interlocking Bricks

- 5.2.6 New Asphalt Shingles

- 5.2.7 Energy Recovery

- 5.3 By End-User Industry

- 5.3.1 Commercial

- 5.3.2 Industrial

- 5.3.3 Municipal

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 Australia

- 5.4.1.5 South Korea

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Allan Myers, Inc.

- 6.4.2 Apollo Asphalt Reclaimers LLC

- 6.4.3 Astec Industries

- 6.4.4 Colas

- 6.4.5 CRH

- 6.4.6 Eurovia (VINCI)

- 6.4.7 Granite Construction Inc.

- 6.4.8 MARINI FAYAT GROUP

- 6.4.9 Martin Marietta

- 6.4.10 MR Roads

- 6.4.11 necoTECH

- 6.4.12 Superpave Engineering Inc.

- 6.4.13 WIRTGEN INDIA Pvt. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment