PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062134

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062134

BLDC Fan - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

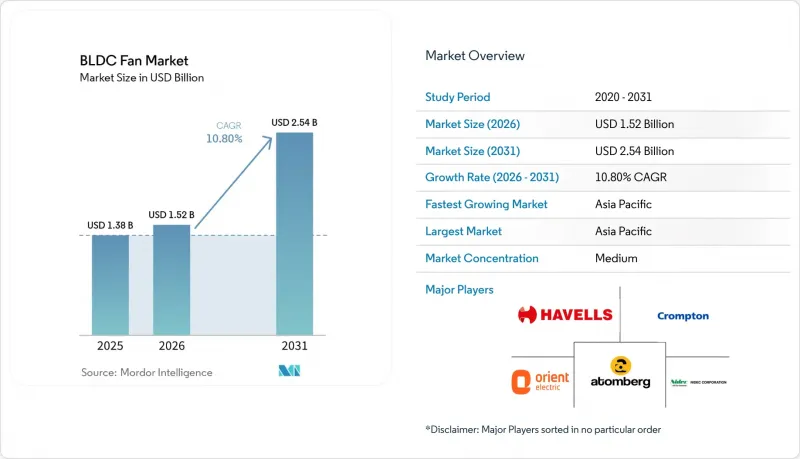

According to Mordor Intelligence, the bLDC fan market size is projected to expand from USD 1.38 billion in 2025 and USD 1.52 billion in 2026 to USD 2.54 billion by 2031, registering a CAGR of 10.80% between 2026 and 2031.

This report is Segmented by Product Type (Ceiling Fans, Pedestal, and More), Motor Architecture (Inner-Rotor BLDC, Outer-Rotor BLDC), Power Rating (Below30 W, 30-60 W, and More), Application (Residential, Commercial Buildings, and More), Distribution Channel (Offline Retail, Online, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global BLDC Fan Market Trends and Insights

Tighter Energy-Efficiency Standards and Star Labeling for Fans

Converging regulations in the United States, European Union, and India reset the baseline for fan performance by using holistic wire-to-air metrics and labeling schemes that expose system losses, which elevate the value of electronically commutated machines in both comfort and process ventilation. California's Title 20 requires FEI≥ 1.00 across a wide range of commercial and industrial fan types, a standard backed by AMCA test procedures and certification pipelines that already count large numbers of compliant models in MAEDbS. The European Commission's 2024 ecodesign rules for fans from 125W to 500kW project 31 TWh of annual electricity savings by 2030 and begin applying in June 2026, which pushes manufacturers to simplify portfolios around higher-efficiency platforms and provide richer performance data for designers. ENERGY STAR Most Efficient criteria for 2025 ventilating fans raise the most practical efficacy thresholds to achieve with EC motors and robust controls rather than with capacitor-start induction systems. Building codes like California Title 24 integrate FEI into mandatory requirements, which turns energy performance into a specification gate rather than a marketing option and positions BLDC fans as default selections in compliant projects.

Payback-Led Residential Replacement of AC Induction with BLDC Ceiling Fans

In India and across parts of Asia-Pacific, electricity tariffs and long daily runtimes compress payback periods for BLDC ceiling fans to below two years at typical price premiums, which makes the switch compelling even without subsidies and lifts repeat purchase intent. Manufacturer data show a conventional 75W induction ceiling fan can cost over INR 2,400 in annual electricity for high-usage homes, while a 28-35W BLDC model can cut that cost by more than half at common usage patterns and tariffs, reinforcing the upgrade case on household economics alone. India's mandatory star labeling for ceiling fans further amplifies this shift by requiring disclosure on service value, letting consumers compare air delivery per watt at the point of purchase, and pushing manufacturers to redesign portfolios around more efficient BLDC platforms. Product strategies in China center less on energy savings and more on connectivity and integration into smart ecosystems, where BLDC motors support quiet, precise speed control as part of larger home automation and IAQ solutions. Wide-voltage designs and controller robustness are also crucial in emerging markets with grid instability, which guides platform choices and value engineering in the BLDC fan market.

Upfront Cost Premium from Rare-Earth Magnets and Controllers.

Capital cost remains a barrier in price-sensitive markets, particularly where fans compete with basic induction alternatives that meet minimum airflow requirements at lower purchase prices. Procurement strategies and bill-of-material choices reflect an ongoing balance between higher-efficiency motors, controller sophistication, and acceptable payback periods at local tariffs. Supply concentration of rare-earth processing and permanent magnet manufacturing elevates input risk for BLDC bill of materials, which sustains premiums over time and complicates pricing strategies for mass-market segments. Manufacturers respond with platform standardization and controller reuse across product lines to improve scale economics and reduce certification overhead. Over the forecast, larger players are better positioned to absorb input volatility, which supports the relative strength of integrated vendors within the BLDC fan market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid EC Fan Adoption in Commercial HVAC for Variable-Speed Control and IAQ

- Data Center and Electronics Thermal Loads Favoring High-Reliability BLDC Fans

- Rare-Earth Magnet Price Volatility and Supply Concentration Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ceiling fans commanded 52.21% share in 2025, making them the largest product category by volume and revenue, while industrial HVLS and commercial ventilation fans deliver the fastest expansion at 11.95% CAGR through 2031, a split that reflects replacement cycles in homes and greenfield growth in logistics, data center, and industrial settings within the BLDC fan market. The installed base and familiarity of ceiling fans sustain their lead, and mandatory labeling in countries like India increases transparency that favors BLDC models with high service value and quiet operation. Product innovation cycles in residential categories now emphasize connectivity, aesthetic options, and lower noise, while commercial and industrial products lean toward controls integration, predictive diagnostics, and high static pressure performance aligned with HVAC design standards. Vendors in Europe and North America have also brought large-diameter EC axial and centrifugal models to market with native digital protocols and AI-supported optimization that build lifetime performance advantages over induction solutions. This mix sustains a strong ceiling fan core while shifting marginal growth to HVLS and specialized ventilation use cases inside the BLDC fan market.

Across product lines, portable, wall, and exhaust fans retain solid roles in code-driven ventilation and spot cooling, but they show more incremental innovation relative to HVLS and advanced commercial systems. Premium consumer products in desk, tower, and bladeless formats compete on design and quietness, with integrated app control and sensor feedback that adapts airflow to room conditions. Industrial HVLS solutions emphasize destratification benefits and year-round comfort in large facilities, where variable-speed EC drives offer smoother control, reduced energy use, and better acoustic performance at low RPM. In warehouses and logistics, BLDC fans combine with demand-based controls to meet both IAQ and comfort targets during peak periods, and manufacturers now include features such as vibration sensing and BMS integration for predictive maintenance. The BLDC fan market continues to balance volume-driven ceiling applications with the growing premium and specification-led opportunity in HVLS and advanced commercial ventilation.

Inner-rotor designs helda 68.87% share in 2025 and remain the architecture of choice for many ceiling, pedestal, and compact fans, while outer-rotor EC designs are the fastest-growing with 9.99% CAGR through 2031 as HVAC systems favor low-speed, high-torque configurations in the BLDC fan market. Inner-rotor motors deliver high torque density in compact footprints and serve reversible, oscillating, and smart ceiling fans well, where rapid speed changes and quiet operation are emphasized in residential and light commercial settings. Their constraints lie in thermal management at higher continuous power, which curbs scalability for large HVAC fans without added conduction paths or heat sinks that raise cost and weight. Outer-rotor EC designs distribute mass around the perimeter for higher torque at low RPM, which suits larger diameters and higher airflows with lower noise and extended bearing life. In air handling applications, these fans can maintain efficiency across wide turndown ranges, which is central to meeting ventilation standards at variable occupancy levels in commercial buildings.

Product launches reinforce these themes with larger-diameter EC platforms and compact diagonal modules that substitute for axial units at lower noise and higher efficiency. European suppliers emphasize modular frames, wide voltage tolerances, and digital communication protocols for faster commissioning and system-level optimization, which improves delivered performance over time. Residential suppliers focus on refinement of connectivity, app control, and silent profiles at low speeds, where user experience drives differentiation in crowded retail categories. Over the forecast period, inner-rotor platforms should retain dominant share by unit volumes, while outer-rotor EC configurations expand share in HVAC, clean room, and process ventilation due to static pressure and low-noise advantages. This architecture mix keeps the BLDC fan market responsive to both consumer preferences and commercial performance targets.

Geography Analysis

Asia-Pacific held 45.75% share in 2025 and leads regional growth at 12.68% CAGR through 2031, with India's high-usage households and mandatory labeling catalyzing BLDC upgrades and China's commercial and industrial deployments aligning with broader electrification and IAQ goals in the BLDC fan market. In India, value communication around wattage and air delivery helps consumers weigh total ownership cost against premiums, while connected features and color choices win share in urban tiers. Southeast Asia presents varied adoption, from high BLDC penetration in Singapore's commercial projects influenced by advanced green building rules to early-stage transitions in large, price-sensitive markets. Japan and Australia show a strong preference for quiet, clean, and connected ventilation in homes and small commercial sites, which underpins premium EC product lines. Across the Asia-Pacific region, standards, labeling, and power stability shape platform designs and marketing narratives in the BLDC fan market.

North America balances mature replacement volumes with high-value commercial and data center deployments that demand integrated controls, reliability, and FEI-aligned specifications. The federal withdrawal of a proposed fan efficiency rule in 2025 kept the regulatory vector at the state and local levels, with California's appliance and building codes establishing baseline performance that guides national portfolios. ENERGY STAR criteria continue to shape ventilating fan performance goals, and BMS-led optimization in certified buildings lifts EC adoption. Data center ecosystems emphasize advanced thermal solutions and 48V-ready components, where BLDC fans with telemetry and modularity integrate best into next-generation power topologies. These factors keep North America a high-value deployment region within the BLDC fan market.

Europe's share reflects smaller absolute volumes compared with Asia-Pacific but strong policy pull from ecodesign, high energy prices, and tightening building performance standards that favor EC solutions in both new builds and retrofits. The European Commission's 2024 update on fans from 125W to 500kW directly raises the efficiency bar, with application in June 2026 and a significant electricity reduction target by 2030, which accelerates portfolio shifts to FEI-aligned systems. Markets like Germany and the UK have seen pronounced adoption in commercial ventilation and clean environments, where large EC centrifugal and axial fans with digital control are now the norm. UK case material demonstrates that BMS optimization combined with efficient fans can drive measurable energy and CO2 reductions, validating longer-run economic outcomes for these investments. Southern and Eastern Europe advance more gradually due to climate and cost factors, but policy, labeling, and incentive structures continue to close gaps. Over the forecast period, Europe's regulatory clarity and designers' familiarity with EC platforms support consistency in the BLDC fan market.

- Atomberg Technologies

- Crompton Greaves Consumer

- Havells India

- Orient Electric

- Usha International

- Polycab India

- Panasonic Life Solutions

- Nidec Corporation

- Delta Electronics

- ebm-papst Group

- Johnson Electric

- Regal Rexnord (Marathon)

- ZIEHL-ABEGG

- Mitsubishi Electric

- Big Ass Fans

- Dyson

- Hunter Fan Company

- Lasko Products

- Haier Smart Home

- Midea Group

- Gree Electric

- MinebeaMitsumi Inc.

- Sanyo Denki

- Allied Motion Technologies

- Jupiter Fan

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tighter energy-efficiency standards and star labeling for fans

- 4.2.2 Payback-led residential replacement of AC induction with BLDC ceiling fans

- 4.2.3 Rapid EC fan adoption in commercial HVAC for variable-speed control and IAQ

- 4.2.4 Data center and electronics thermal loads favoring high-reliability BLDC fans

- 4.2.5 48V DC distribution in racks/buildings enabling direct BLDC fan deployments

- 4.2.6 Utility and green-building incentives bundling smart BLDC fans with BMS/EMS

- 4.3 Market Restraints

- 4.3.1 Upfront cost premium from rare-earth magnets and controllers

- 4.3.2 Rare-earth magnet price volatility and supply concentration risks

- 4.3.3 After-sales electronics service gaps and reliability concerns in harsh environments

- 4.3.4 EMI/acoustic compliance constraints slowing global SKU rollouts

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Ceiling Fans

- 5.1.2 Pedestal & Table Fans

- 5.1.3 Wall & Exhaust Fans

- 5.1.4 Industrial HVLS / Commercial Ventilation Fans

- 5.2 By Motor Architecture

- 5.2.1 Inner-Rotor BLDC

- 5.2.2 Outer-Rotor BLDC (EC)

- 5.3 By Power Rating

- 5.3.1 <30 W

- 5.3.2 30 - 60 W

- 5.3.3 60 - 120 W

- 5.3.4 >120 W

- 5.4 By Application

- 5.4.1 Residential

- 5.4.2 Commercial Buildings

- 5.4.3 Industrial / Warehouse

- 5.4.4 Data-Centre & Electronics Cooling

- 5.4.5 Automotive Cabin & Battery-Thermal

- 5.5 By Distribution Channel

- 5.5.1 Offline Retail (Dealer / MBO)

- 5.5.2 Direct Institutional & OEM

- 5.5.3 Online (E-commerce & D2C)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 Canada

- 5.6.1.2 United States

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Asia-Pacific

- 5.6.3.1 India

- 5.6.3.2 China

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 South East Asia (SG, MY, TH, ID, VN, PH)

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 Europe

- 5.6.4.1 United Kingdom

- 5.6.4.2 Germany

- 5.6.4.3 France

- 5.6.4.4 Spain

- 5.6.4.5 Italy

- 5.6.4.6 BENELUX

- 5.6.4.7 NORDICS

- 5.6.4.8 Rest of Europe

- 5.6.5 Middle East And Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East And Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Atomberg Technologies

- 6.4.2 Crompton Greaves Consumer

- 6.4.3 Havells India

- 6.4.4 Orient Electric

- 6.4.5 Usha International

- 6.4.6 Polycab India

- 6.4.7 Panasonic Life Solutions

- 6.4.8 Nidec Corporation

- 6.4.9 Delta Electronics

- 6.4.10 ebm-papst Group

- 6.4.11 Johnson Electric

- 6.4.12 Regal Rexnord (Marathon)

- 6.4.13 ZIEHL-ABEGG

- 6.4.14 Mitsubishi Electric

- 6.4.15 Big Ass Fans

- 6.4.16 Dyson

- 6.4.17 Hunter Fan Company

- 6.4.18 Lasko Products

- 6.4.19 Haier Smart Home

- 6.4.20 Midea Group

- 6.4.21 Gree Electric

- 6.4.22 MinebeaMitsumi Inc.

- 6.4.23 Sanyo Denki

- 6.4.24 Allied Motion Technologies

- 6.4.25 Jupiter Fan

7 Market Opportunities & Future Outlook

- 7.1 Rapid-cook combi ovens integrating microwave & impingement for QSRs

- 7.2 AI-driven autonomous cooking algorithms for consistency & labour savings