PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062135

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062135

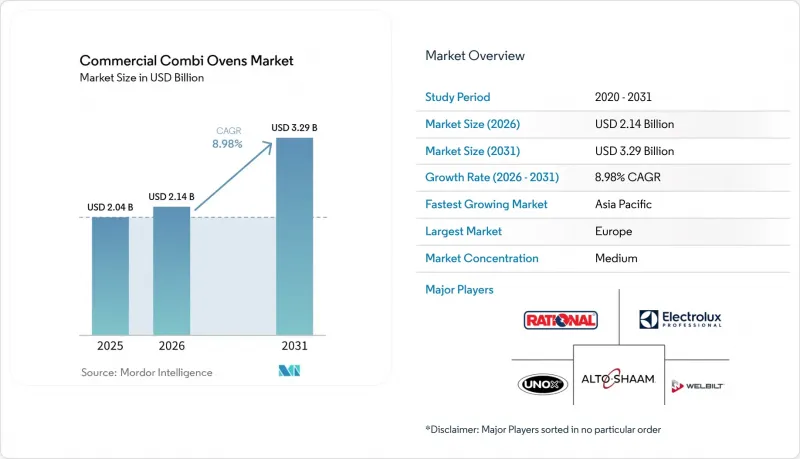

Commercial Combi Ovens - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the commercial combi ovens market size is projected to be USD 2.04 billion in 2025, USD 2.14 billion in 2026, and reach USD 3.29 billion by 2031, growing at a CAGR of 8.98% from 2026 to 2031.

This report is Segmented by Power Source (Electric, Gas), Steam Generation (Boiler, Injector), Capacity (Less Than 20 Lbs, 20-50 Lbs, and More), Installation Type (Counter-Top, Floor-Standing), End-User (QSR, Full-Service Restaurants, Hotels & Resorts, and More), and Geography (North America, South America, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD Million).

Global Commercial Combi Ovens Market Trends and Insights

Sustainability-Driven Kitchen Retrofits Propel Electrification and Lifecycle-Cost Focus

Electrification momentum is building as operators integrate high-efficiency equipment to reduce energy use and meet building performance targets. In 2025, a UK hospitality organization study highlighted that electric cooking equipment can reach around 90% energy-use efficiency compared to 40-60% for gas, a differential that supports both operating-cost reduction and lower heat in work areas. The Sustainable Restaurant Association (SRA), the Global Cooksafe Coalition (GCC), and Hospitality Energy Saving and Sustainability (HESS) combined study found that all-electric kitchens in real-world sites delivered annual energy-cost savings between GBP 2,610 and GBP 8,839, energy-consumption cuts of 49-64%, and carbon-emissions reductions of 50-65%, with a payback of around three years and 10-year savings above GBP 65,000 for a modeled gastropub, reinforcing the total-cost-of-ownership case for integrated electric platforms. These outcomes align with the core value proposition of the commercial combi ovens market, as single multi-mode systems can replace multiple appliances, lighten hood loads, and support demand-controlled exhaust strategies. Public- and private-sector procurement frameworks increasingly emphasize lifecycle-managed contracts, preventive maintenance, and remote monitoring to preserve performance and energy savings over time, which syncs with connected combi systems and manufacturer service programs. In regions prioritizing net-zero pathways and green-building standards, high-efficiency combi platforms enable electrification without sacrificing menu range, which is a key decision factor for multi-site chains and institutional buyers.

Ghost-Kitchen Expansion Accelerates Demand for Compact, Multi-Brand-Capable Units

Delivery-first business models require equipment that supports high throughput in small footprints, consistent yields for packaging and holding, and fast changeovers across multiple virtual brands. Asia-Pacific shows the strongest momentum, with the dark-kitchen business expanding in China and India as platforms and operators scale delivery logistics and multi-brand operating models at speed. These kitchens prioritize flexible equipment that supports programmable cooking, cloud-managed recipes, and compact or stackable footprints that work in sites with limited hood positions, which aligns with new-generation counter-top combi configurations. Reduced front-of-house investment in delivery-only sites can shift more budget to automation and connected back-of-house systems, which shortens menu iteration cycles and promotes standardization across multiple brands. As the commercial combi ovens market evolves, compact designs with efficient clean cycles and quick pre-heats allow operators to reconfigure production between dayparts and to run diverse menus from a constrained line-up. Continuous expansion of delivery ecosystems in dense urban areas favors programmable, networked combi ovens that enable multi-brand execution with repeatability at scale.

Capital Cost Premium Versus Traditional Convection Platforms Constrains SME Adoption

Upfront prices for commercial combi ovens exceed those of traditional gas convection platforms, which pressures budgets for independent operators and smaller chains. Equipment financing can spread acquisition costs over 12-84 months, with terms and rates linked to credit profiles, and this can include Section 179 deductions and bonus depreciation mechanics that influence purchase timing in 2026 and 2027. Manufacturer-backed leasing and bundled connectivity subscriptions demonstrate new routes to adoption that wrap hardware, maintenance, and service into fixed monthly fees, and these programs are seeing early traction with public-sector and multi-site buyers that value predictability. UNOX has brought an all-inclusive leasing model to UK public-sector caterers that packages delivery, installation, scheduled maintenance, and warranty within a monthly payment, which highlights how the commercial combi ovens market is adapting procurement to budget cycles. For cost-sensitive operators, certified pre-owned supply offers a lower entry price with warranty coverage, although availability and performance consistency can vary by source and vintage, which continues to limit scale in some regions.

Other drivers and restraints analyzed in the detailed report include:

- Labor Scarcity and Wage Inflation Drive Automation and Skill-Agnostic Equipment

- AI-Driven Recipe Optimization and Predictive Maintenance Lower Operational Complexity

- Three-Phase Electrical Infrastructure Gaps in Emerging Markets Delay Electrification Timelines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electric combi ovens accounted for 61.23% of 2025 revenue and are projected to expand at an 8.65% CAGR to 2031, supported by regulatory momentum and lifecycle-cost improvements that strengthen the value case in high-wage regions. The commercial combi ovens market is benefiting from city-level restrictions on new gas connections in several jurisdictions, which is concentrating new-build demand on electric platforms with advanced controls and cloud connectivity for fleet-wide standardization. Electric cooking is recognized for higher energy-use efficiency compared with gas, which reduces ambient kitchen heat and supports a better working environment that can improve staff retention in tight labor markets. As the commercial combi ovens market evolves, the ecosystem of connected services and remote monitoring supports uptime, compliance logging, and software updates, which aligns with the priorities of multi-location buyers that emphasize uniform execution.

Gas combi ovens retain a role in markets with low gas prices, established infrastructure, and culinary requirements that prefer flame or specific moisture dynamics, yet long-term regulatory uncertainty and cost variability are pushing many chains to plan for electrification. Product advances also show a pathway for future-proofing gas investments as energy systems evolve, including units that are designed to run on gas blends with hydrogen content in order to reduce emissions intensity in step with infrastructure changes. Maintenance profiles also differ, as gas units require flue management and periodic combustion checks, while electric platforms avoid flues and reduce indoor air pollutants, which can simplify compliance and operational routines in sensitive sites. In the commercial combi ovens market, the decision between electric and gas is increasingly grounded in lifecycle economics, local code requirements, and staffing priorities, with electric seeing broader preference in new-build and high-traffic chain locations. Where electrification remains phased, operators combine portable induction with compact combi ovens to reach targeted efficiency gains before a complete line conversion.

Boiler-based steam generation held 56.62% of 2025 revenue based on a legacy preference for precise humidity control and strong steam output. The commercial combi ovens market has seen injector-based systems close the performance gap as manufacturers improve preheating, atomization, and steam modulation to enable precise setpoint control and faster responsiveness for varied cooking tasks. Injector systems generate steam on demand by spraying water onto hot surfaces, which reduces standby energy draw and lowers water use because there is no tank to maintain at a temperature. Operators in hard-water areas often favor injector designs because they avoid reverse-osmosis infrastructure, save space, and simplify upkeep by reducing scale formation, which can lower maintenance costs over time. Growth expectations reflect these usage advantages and a technology curve that is maturing at scale, supporting a 9.15% CAGR for injector systems through 2031 in the commercial combi ovens market.

Menu and site conditions still shape architecture choices. Seafood and shellfish production can expose injector components to corrosive residues that require adherence to cleaning routines, while high-volume batch work for precision applications may continue to lean on boiler-based systems in specific contexts. Across both architectures, site water testing and filtration guidance remain essential, with attention to chlorine or chloramine tolerances and deliming protocols. OEMs are also enhancing variable-speed fans and self-clean coverage to reduce downtime and extend intervals between service cycles, which supports throughput and asset availability across large fleets. The commercial combi ovens market continues to educate buyers on aligning steam architecture with menu mix, water quality, and maintenance capacity in order to sustain expected performance across the equipment lifecycle.

Geography Analysis

Europe led with 34.41% of global revenue in 2025, supported by sustainability mandates, structured public procurement, and strong multi-brand catering networks. The region's associations actively track regulatory changes and product standards, helping manufacturers and buyers align on energy performance, materials, and compliance, which increases confidence in electrification investments across the commercial combi ovens market. UK Hospitality has highlighted the efficiency and work-environment gains from electric equipment, and 2026 guidance on electric kitchen savings has reinforced the case for transitions with tangible operational results. European OEMs continue to advance repairability and hydrogen readiness in gas-capable models, providing a bridge as infrastructure evolves and helping future-proof purchases under tightening emissions standards. The commercial combi ovens market size in Europe also benefits from tourism recovery and refurbishment cycles in hotels and foodservice chains that are standardizing on connected, multi-function platforms.

Asia-Pacific is set to post the fastest regional growth at a projected 9.79% CAGR through 2031, propelled by delivery ecosystems and urban density that demand compact, connected equipment. China remains a core market with technology-forward consumers and strong delivery penetration, while India's young, mobile-first population is driving smart, multi-brand kitchen models that value space efficiency and standardized execution. Southeast Asian markets are seeing gains driven by urbanization and tourism, and demand for remote monitoring and predictive maintenance is rising as operators scale their footprints across cities and countries. Some near-term softness in parts of the region has not changed the longer-term pattern, where labor constraints and delivery growth continue to push fleets toward intelligent, multi-function ovens that use space and energy more effectively. As the commercial combi ovens market expands, regional tailoring of cost and feature sets provides a path to penetration in SME-heavy segments.

North America shows steady momentum in dealer channels and among independents, institutions, and fast-casual operators, with large QSRs pacing investments amid mixed macro signals in 2025-2026. Associations representing a large base of manufacturers engage with energy, environmental, and regulatory topics that shape training, product qualification, and operator confidence in adoption. At the city level, the acceleration of New York City's Local Law 154 tightened exemptions for gas appliances in new buildings, which will concentrate upcoming projects on electric solutions and support a multi-year adoption curve for connected combi platforms in the commercial combi ovens market. In Canada, restaurant sales data and operator ROI guidance from equipment distributors indicate interest in high-efficiency ovens that compress payback windows and deliver quantifiable water and energy savings. Across Latin America, the Middle East, and Africa, adoption depends on electrical infrastructure and access to financing, with microfinance and leasing models emerging in some countries to support independent operators, while grid constraints in parts of MEA and APAC slow full electrification timelines. As the global commercial combi ovens market matures, regional differences in codes, infrastructure, and financing shape the pace and path of transitions.

- Rational AG

- Electrolux Professional AB

- Welbilt (Convotherm)

- Alto-Shaam Inc.

- Unox S.p.A.

- MKN GmbH

- Lainox (Ali Group)

- Blodgett (Middleby)

- Henny Penny Corp.

- Turbofan (Moffat)

- Retigo

- Hobart Corporation

- Fagor Industrial

- Eloma GmbH

- Angelo Po

- HOUNO A/S

- Bonnet International

- Palux AG

- Midea Group

- Duke Manufacturing

- Panasonic Corporation

- Vulcan

- Bongard

- Robot Coupe

- EssEmm Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Sustainability-driven kitchen retrofits (energy, water, waste)

- 4.2.2 Growing ghost-kitchen & dark-store footprints

- 4.2.3 Regulations on gas cooking emissions (e.g., U.S. city gas bans)

- 4.2.4 Post-COVID labor shortage accelerating back-of-house automation

- 4.2.5 AI-enabled recipe optimization lowering skill barriers (under-reported)

- 4.2.6 Micro-financing apps for independent QSR equipment leasing (under-reported)

- 4.3 Market Restraints

- 4.3.1 High capex vs. traditional convection ovens

- 4.3.2 Persistent gas price volatility influencing OPEX planning

- 4.3.3 Limited three-phase power availability in emerging markets (under-reported)

- 4.3.4 Data-security concerns around IoT-connected ovens (under-reported)

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Power Source

- 5.1.1 Electric

- 5.1.2 Gas

- 5.2 By Steam Generation

- 5.2.1 Boiler

- 5.2.2 Injector

- 5.3 By Capacity

- 5.3.1 Less than 20 lbs

- 5.3.2 20-50 lbs

- 5.3.3 50-100 lbs

- 5.3.4 More than 100 lbs

- 5.4 By Installation Type

- 5.4.1 Counter-top

- 5.4.2 Floor-standing

- 5.5 By End-User

- 5.5.1 Quick-Service Restaurants (QSR)

- 5.5.2 Full-Service Restaurants

- 5.5.3 Hotels & Resorts

- 5.5.4 Bakeries & Confectioneries

- 5.5.5 Institutional Catering

- 5.5.6 Catering Services & Central Kitchens

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 Canada

- 5.6.1.2 United States

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Asia-Pacific

- 5.6.3.1 India

- 5.6.3.2 China

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 South East Asia

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 Europe

- 5.6.4.1 United Kingdom

- 5.6.4.2 Germany

- 5.6.4.3 France

- 5.6.4.4 Spain

- 5.6.4.5 Italy

- 5.6.4.6 BENELUX

- 5.6.4.7 NORDICS

- 5.6.4.8 Rest of Europe

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East & Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Rational AG

- 6.4.2 Electrolux Professional AB

- 6.4.3 Welbilt (Convotherm)

- 6.4.4 Alto-Shaam Inc.

- 6.4.5 Unox S.p.A.

- 6.4.6 MKN GmbH

- 6.4.7 Lainox (Ali Group)

- 6.4.8 Blodgett (Middleby)

- 6.4.9 Henny Penny Corp.

- 6.4.10 Turbofan (Moffat)

- 6.4.11 Retigo

- 6.4.12 Hobart Corporation

- 6.4.13 Fagor Industrial

- 6.4.14 Eloma GmbH

- 6.4.15 Angelo Po

- 6.4.16 HOUNO A/S

- 6.4.17 Bonnet International

- 6.4.18 Palux AG

- 6.4.19 Midea Group

- 6.4.20 Duke Manufacturing

- 6.4.21 Panasonic Corporation

- 6.4.22 Vulcan

- 6.4.23 Bongard

- 6.4.24 Robot Coupe

- 6.4.25 EssEmm Corp.

7 Market Opportunities & Future Outlook

- 7.1 Digitally native 'equipment-as-a-service' subscription models

- 7.2 Hydrogen-ready combi ovens for net-zero commercial kitchens