PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062142

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062142

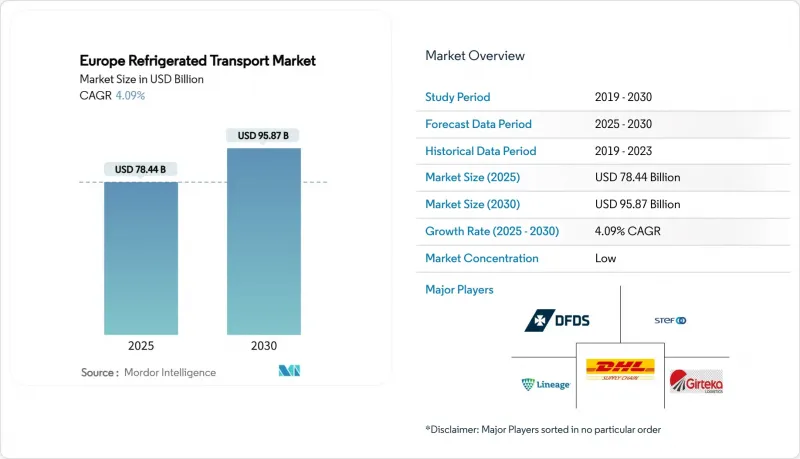

Europe Refrigerated Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe refrigerated transport market size is projected to be USD 78.44 billion in 2025, USD 81.58 billion in 2026, and reach USD 99.52 billion by 2031, growing at a CAGR of 4.0% from 2026 to 2031.

Heightened demand for precise temperature control in pharmaceutical and meal-kit logistics, coupled with retailer net-zero commitments, is reshaping fleet specifications and route planning. This report is Segmented by Mode of Transport (Road, Rail, Sea, Air), by Temperature (Chilled 0-5°C, Frozen -18-0°C, Ambient, Deep-Frozen/Ultra-Low More Than 20°C), by Application (Food & Beverages, Pharmaceuticals & Life-Sciences, Chemicals & Specialty Materials, Floral & Nursery, and More), and by Geography (Germany, France, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Refrigerated Transport Market Trends and Insights

IoT-Enabled End-to-End Cold-Chain Visibility

5G-linked sensors now stream temperature, humidity, and location data across road, rail, sea, and air legs, cutting excursion incidents by up to 35% for fleets deploying platforms such as Carrier's Lynx Fleet. Insurance firms are rewarding documented visibility with 10-15% premium discounts, improving return on technology spend. European Good Distribution Practice rules for medicines mandate continuous monitoring, pushing IoT uptake beyond early adopters. Trailer builders are integrating telematics at the factory, evidenced by Schmitz Cargobull's Atlantis Global System purchase, which embeds tracking hardware into new reefers. Predictive analytics built on sensor streams now flag compressor faults before cargo risk escalates, trimming unplanned downtime by roughly a quarter.

Booster Immunization Campaigns Driving Pharma Flows

Continued COVID-19 and influenza booster programs, plus a surge of temperature-sensitive biologics, keep 2-8 °C lanes running near capacity. DHL has expanded GDP-certified hubs across Europe, adding validated storage zones to support multi-temperature breaks in transit. High-value GLP-1 drugs for diabetes and obesity therapy move under reinforced chain-of-custody protocols, justifying premium freight rates. Modal diversification is growing; stable products shift to ocean or rail to cut emissions, while cell and gene therapies stay in air corridors for speed. Reusable packaging with embedded data-loggers is gaining traction, cutting waste and slicing total packaging spend by nearly half over multi-cycle use.

EU F-Gas Quota Cuts Raising Low-GWP Refrigerant Prices

Regulation 2024/573 slashes hydrofluorocarbon availability by nearly 88% in 2027 and 95% in 2030, driving R452A prices toward USD 49 per kg (EUR 45) versus USD 6-17 for natural CO2 or propane. Operators face retrofit bills of USD 16,000-37,000 per truck to adopt compliant systems. Carrier has introduced surcharges to offset steep input costs, yet promises 89% lower climate impact with next-gen refrigerants. Capital strain is harshest on small haulers that run older fleets.

Other drivers and restraints analyzed in the detailed report include:

- Meal-Kit and Ready-to-Cook Subscription Boom

- Retailer Net-Zero Targets Accelerating Fleet Electrification

- High Fuel & Energy Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Road transport captured 65.97% of the Europe refrigerated transport market share in 2025, anchored by flexible door-to-door service for grocery and pharma shippers. Driver shortages, such as 426,000 vacancies in early 2025 and steep toll hikes, are eroding cost advantages, but embedded telematics and expanded direct-store routes keep trucks indispensable. Rail and sea gain share where carbon targets are stringent; the Brenner Base Tunnel is forecast to increase the corridor's daily train capacity by over 50% (accommodating up to 400 trains per day) once fully opened, drawing frozen protein flows from Northern ports to Italian retailers. Air freight, paced by 7.66% CAGR, channels high-value biologics that justify premium lift prices, especially out of pharma clusters in Frankfurt and Basel. The ascent of controlled-atmosphere reefers on short-sea lanes also eases pressure on congested roads, extending shelf life by an extra week for citrus and berries.

Road's relative margin narrows as electricity and diesel dynamics diverge. Battery trucks excel on sub-250 km milk runs but struggle with long-haul payload penalties, while hydrogen prototypes target the Hamburg-Munich spine. Fleet operators hedge through dual-fuel strategies, pairing battery last-mile vans with liquid gas line-haul tractors to meet emission caps without sacrificing range. Intermodal players market CO2 savings of up to 75% versus truck-only delivery, a compelling figure for retailers reporting Scope 3 progress. As the value of visibility rises, carriers that integrate IoT telemetry across truck, rail, and vessel legs are winning new tenders from life-science shippers.

List of Companies Covered in this Report:

- DHL Group

- DFDS Logistics

- STEF Group

- Lineage Logistics

- Girteka Logistics

- Waberer's International

- DSV

- Dachser

- Frigoscandia

- Kuehne + Nagel

- Hellmann Worldwide Logistics

- Noatum Logistics

- Rhenus Logistics

- Geodis

- XPO Logistics

- Frigotrans

- Transports Octavio

- Constellation Cold Logistics

- Culina Group

- AGI Global Logistics Ltd*

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 IoT-Enabled End-To-End Cold-Chain Visibility

- 4.2.2 Booster Immunization Campaigns Driving Refrigerated Pharma Flows

- 4.2.3 Meal-Kit and Ready-To-Cook Subscription Boom

- 4.2.4 Retailer Net-Zero Targets Accelerating Fleet Electrification

- 4.2.5 Hydrogen Fuel-Cell Power Packs for Trailer Refrigeration

- 4.2.6 Liberalized Cross-Border Rail Paths for Temperature-Controlled Intermodal

- 4.3 Market Restraints

- 4.3.1 Peak-Hour Electricity Tariffs Inflating E-Reefer OPEX

- 4.3.2 EU F-Gas Quota Cuts Raising Low-GWP Refrigerant Prices

- 4.3.3 ADR-Qualified Technician Shortage for Lithium Battery Reefers

- 4.3.4 Pallet Standard Mismatches Causing Reverse-Logistics Dead-Runs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Mode of Transport

- 5.1.1 Road

- 5.1.2 Rail

- 5.1.3 Sea

- 5.1.4 Air

- 5.2 By Temperature

- 5.2.1 Chilled (0-5 °C)

- 5.2.2 Frozen (-18-0 °C)

- 5.2.3 Ambient

- 5.2.4 Deep-Frozen / Ultra-Low (more than -20 °C)

- 5.3 By Application

- 5.3.1 Food and Beverages

- 5.3.2 Pharmaceuticals and Life-sciences

- 5.3.3 Chemicals and Specialty Materials

- 5.3.4 Floral & Nursery

- 5.3.5 Other Perishables

- 5.4 By Country

- 5.4.1 Germany

- 5.4.2 France

- 5.4.3 United Kingdom

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Netherlands

- 5.4.7 Belgium

- 5.4.8 Poland

- 5.4.9 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 DFDS Logistics

- 6.4.3 STEF Group

- 6.4.4 Lineage Logistics

- 6.4.5 Girteka Logistics

- 6.4.6 Waberer's International

- 6.4.7 DSV

- 6.4.8 Dachser

- 6.4.9 Frigoscandia

- 6.4.10 Kuehne + Nagel

- 6.4.11 Hellmann Worldwide Logistics

- 6.4.12 Noatum Logistics

- 6.4.13 Rhenus Logistics

- 6.4.14 Geodis

- 6.4.15 XPO Logistics

- 6.4.16 Frigotrans

- 6.4.17 Transports Octavio

- 6.4.18 Constellation Cold Logistics

- 6.4.19 Culina Group

- 6.4.20 AGI Global Logistics Ltd*

7 Market Opportunities and Future Outlook