PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062144

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062144

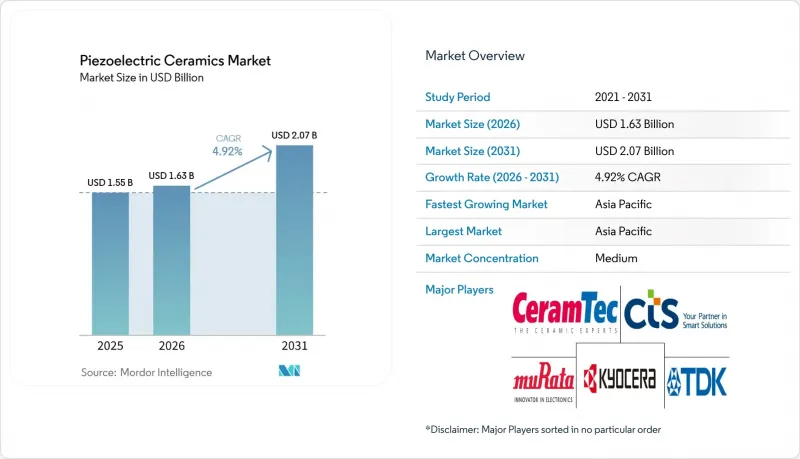

Piezoelectric Ceramics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the piezoelectric ceramics market size is projected to expand from USD 1.55 billion in 2025 and USD 1.63 billion in 2026 to USD 2.07 billion by 2031, registering a CAGR of 4.92% between 2026 to 2031.

This report is Segmented by Material Composition (Lead-Based and Lead-Free), Application (Sensors, Actuators, Energy Harvesters and Nanogenerators, and More), End-User Industry (Consumer Electronics, Automotive and E-Mobility, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Piezoelectric Ceramics Market Trends and Insights

Rising Adoption in Medical Imaging and Therapeutic Devices

Piezoelectric ceramics are increasingly replacing older transducer materials in compact ultrasound equipment as hospitals demand portable solutions. Lead-free KNN ceramics have achieved a d33 of 630 pC/N in wearable ultrasound patches, addressing toxicity concerns while maintaining sensitivity. pMUTs manufactured on CMOS lines reduce production costs and simplify signal integration in point-of-care scanners. High-intensity focused ultrasound systems now utilize CeramTec hemispherical discs larger than 150 mm, meeting power-density requirements for tumor ablation. Biocompatibility regulations in the United States and EU are accelerating the transition to lead-free BNT-BT composites, which match PZT power output at lower drive temperatures. As a result, device manufacturers are achieving both performance and compliance benefits, strengthening the piezoelectric ceramics market.

5G/6G RF-Filter Miniaturization Needs High-k Piezoceramics

Millimeter-wave rollouts require AlScN and LiNbO3 thin films for high-Q BAW and SAW filters that fit inside smartphone modules under 1 mm2. AlScN's kt2 exceeding 10% provides a sharper roll-off that handset OEMs need for crowded spectrum allocations. LiNbO3 LLSAW filters are optimized for sub-6 GHz bands, offering superior power handling compared to quartz. FUJIFILM's 2025 patent on niobium-doped PZT multilayers achieves a d31 of 389 pC/V below 7 V, aligning with the requirements of low-voltage mobile electronics. The rapid multiplication of frequency bands in 6G R&D ensures sustained demand, supporting long-term growth in the piezoelectric ceramics market.

Competition from PVDF-Based Piezopolymers

PVDF's flexibility, lightweight properties, and FDA clearance are driving its adoption in wearables, soft robotics, and implantable sensors, challenging rigid ceramics. While its d33 of 20-30 pC/N is significantly lower than PZT, it is sufficient for low-force applications. Cost-effective production methods such as solution casting and electrospinning are encouraging consumer brands to adopt polymer films. This shift toward entry-level applications intensifies price competition, exerting pressure on margins across the piezoelectric ceramics market.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Local MLCC Capacity Using PZT Dielectrics

- Quantum Transducer R&D Drives Cryogenic Piezoceramic Demand

- Supply-Chain Volatility of Nb2O5 and Ta2O5 for Lead-Free KNN Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lead-based systems accounted for 81.11% of the piezoelectric ceramics market share in 2025, with this share projected to grow at a 5.14% CAGR through 2031. The market size for lead-based variants is expanding faster than the overall market due to PZT's benchmark-setting d33 values exceeding 600 pC/N. Manufacturers are enhancing performance through dopants like niobium, as demonstrated by FUJIFILM's sub-7 V multilayer actuator patent. Parallel lead-free programs are being developed to mitigate future compliance risks but have yet to challenge PZT's dominance in high-performance applications such as medical imaging and sonar.

BNT-BT discs have shown equivalent acoustic power to PZT in 40 kHz ultrasonic cleaners with reduced heat generation, while KNN soft grades are targeting underwater receivers. Bismuth-layered ferroelectrics, with Curie points above 650 °C, are enabling extreme-temperature applications like oil-well logging. However, each substitution requires requalification in terms of geometry, voltage, and lifetime, which slows adoption but supports a multi-year growth trajectory within the piezoelectric ceramics market.

Geography Analysis

Asia-Pacific generated 52.22% of global revenue in 2025 and is projected to grow at a 5.78% CAGR through 2031. China dominates in high-volume powder and low-cost disc production, Japan specializes in multilayer and thin-film precision parts, and South Korea and Taiwan integrate components into smartphones and 5G modules. Murata's USD 233 million Fukui R&D facility, completed in February 2026, focuses on barium titanate and PZT advancements, reinforcing the region's leadership. Indian companies like Sparkler Ceramics are scaling industrial sensor production, while Australian miners drive demand for ruggedized sensors in challenging environments.

North America's demand is driven by aerospace, defense, and medical ultrasound applications. The CHIPS Act's fabrication incentives have indirectly benefited piezoelectric ceramics by sharing cleanroom facilities with semiconductor production. TDK's new U.S. production line for Apple products underscores the appeal of local sourcing amid geopolitical uncertainties. Canada and Mexico contribute through aerospace tooling and automotive sensor assembly, supporting the regional piezoelectric ceramics market.

Europe is led by Germany's automotive and industrial automation sectors and the United Kingdom's aerospace industry. CeramTec is scaling up production of large-format PZT discs for sonar applications, while PI Ceramic's April 2025 advancements in BNT and KNN materials have spurred collaborative projects. Strict EU RoHS regulations are accelerating the adoption of lead-free alternatives faster than in other regions. Additionally, Brazil's offshore energy projects and Saudi Arabia's smart-city initiatives contribute smaller but strategically significant volumes to the global piezoelectric ceramics market.

- APC International Ltd.

- Arkema

- CeramTec GmbH

- CTS Corporation

- FUJI CERAMICS CORPORATION

- Johnson Matthey

- KEMET

- Kistler Group

- KYOCERA Corporation

- Morgan Advanced Materials

- Murata Manufacturing Co., Ltd.

- Physik Instrumente (PI) SE & Co. KG

- PI Ceramic GmbH

- Piezosystem Jena GmbH

- SAMSUNG ELECTRO-MECHANICS

- Sensortech Canada

- Sparkler Ceramics Pvt. Ltd.

- TDK Corporation

- TRS Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising adoption in medical imaging and therapeutic devices

- 4.2.2 5G/6G RF-filter miniaturisation needs high-k piezoceramics

- 4.2.3 Government incentives for local MLCC capacity using PZT dielectrics

- 4.2.4 Quantum transducer R&D drives cryogenic piezoceramic demand

- 4.2.5 Additive manufacturing enables complex aerospace piezo meta-structures

- 4.3 Market Restraints

- 4.3.1 Competition from PVDF-based piezopolymers

- 4.3.2 Supply-chain volatility of Nb2O5 and Ta2O5 for lead-free KNN systems

- 4.3.3 High scrap rates in additive-manufactured piezoceramics scale-up

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Composition

- 5.1.1 Lead-based (PZT, PMN-PT, PZN-PT)

- 5.1.2 Lead-free (BNT-BT, KNN, BaTiO3, ZnO)

- 5.2 By Application

- 5.2.1 Sensors (pressure, ultrasonic, MEMS mics)

- 5.2.2 Actuators (fuel injectors, micro-positioners)

- 5.2.3 Energy Harvesters and Nanogenerators

- 5.2.4 Ultrasonic Imaging and Cleaning

- 5.2.5 Frequency Control and Timing (SAW/BAW resonators)

- 5.3 By End-user Industry

- 5.3.1 Consumer Electronics

- 5.3.2 Automotive and E-Mobility

- 5.3.3 Healthcare and Life-Sciences

- 5.3.4 Industrial Automation and Robotics

- 5.3.5 Aerospace and Defense

- 5.3.6 Energy and Utilities

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 Australia

- 5.4.1.5 NORDIC Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 APC International Ltd.

- 6.4.2 Arkema

- 6.4.3 CeramTec GmbH

- 6.4.4 CTS Corporation

- 6.4.5 FUJI CERAMICS CORPORATION

- 6.4.6 Johnson Matthey

- 6.4.7 KEMET

- 6.4.8 Kistler Group

- 6.4.9 KYOCERA Corporation

- 6.4.10 Morgan Advanced Materials

- 6.4.11 Murata Manufacturing Co., Ltd.

- 6.4.12 Physik Instrumente (PI) SE & Co. KG

- 6.4.13 PI Ceramic GmbH

- 6.4.14 Piezosystem Jena GmbH

- 6.4.15 SAMSUNG ELECTRO-MECHANICS

- 6.4.16 Sensortech Canada

- 6.4.17 Sparkler Ceramics Pvt. Ltd.

- 6.4.18 TDK Corporation

- 6.4.19 TRS Technologies Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment