PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062153

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062153

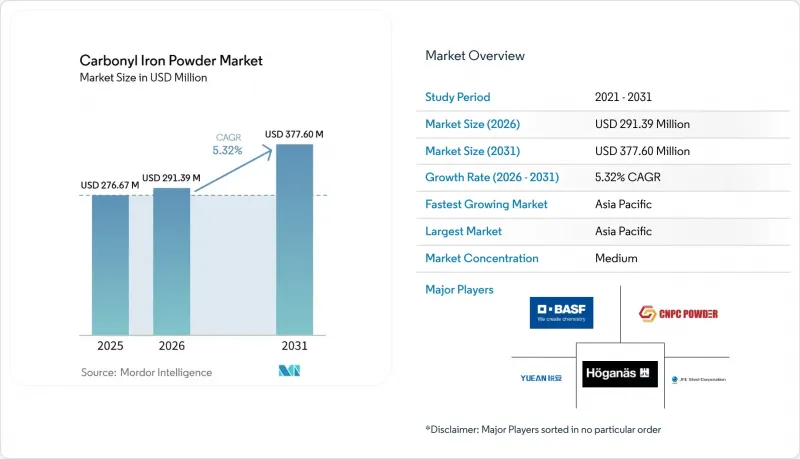

Carbonyl Iron Powder - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the carbonyl iron powder market size is projected to expand from USD 276.67 million in 2025 and USD 291.39 million in 2026 to USD 377.60 million by 2031, registering a CAGR of 5.32% between 2026 to 2031.

This report is Segmented by Type (Reduced Carbonyl Iron Powder and Atomized Carbonyl Iron Powder), Purity Grade (Standard More Than or Equal To 97% Fe, and More), End-User Industry (Electronics and Electricals, Automotive, Healthcare and Pharmaceuticals, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Carbonyl Iron Powder Market Trends and Insights

Surge in Powder-Metallurgy Use for Lightweight Electric Vehicle Drivetrain Parts

Electric-vehicle manufacturers are increasingly adopting powder-metallurgy components such as gears, cams, and brackets. These components help reduce drivetrain mass by 15% to 20% while maintaining fatigue strength above 500 MPa. This reduction contributes to an additional range of 15 to 20 km for every kilogram saved. A case study from Porite indicated a 20% to 30% cost reduction compared to machined steel. Similarly, Sterling Sintered Technologies reported that soft magnetic composites made with carbonyl iron powder reduced core losses by 20% and decreased motor sizes by 30%. The growing demand for lightweight and efficient components in electric vehicles is driving the adoption of powder-metallurgy solutions. Carbonyl iron powder is gaining attention in high-performance applications due to its spherical morphology and high sinterability. Suppliers capable of customizing particle sizes within the 1 to 5 micron range and providing pre-insulated grades to minimize eddy-current losses are positioned to achieve higher pricing. On the other hand, producers without these capabilities may face pressure on margins as automakers leverage their purchasing volumes to negotiate lower prices.

Uptake of Metal-Injection Molding for Miniaturized Medical Devices

In 2024, the revenue from medical and dental metal-injection molding (MIM) ranged between USD 578 million and USD 1.88 billion, with a growth rate of nearly 9% CAGR. The preference for carbonyl iron powder is driven by its spherical particles, which enable a 60 vol% solids loading and achieve densities exceeding 95% of theoretical post-sintering. To meet USP and ASTM B883-10 standards, oxygen content is limited to 0.2%, which helps reduce porosity in body-fluid environments. Suppliers that fail to comply may face exclusion from high-margin contracts, as FDA 21 CFR 820 documentation requirements become stricter. Metal-injection molding, capable of achieving tolerances below 0.05 mm and surface finishes finer than 1.6 µm, is essential for manufacturing orthodontic brackets and implantable housings.

Occupational Nanoparticle Inhalation Liabilities

Regulators, despite a systematic review finding no consistent disease link, have capped workplace iron-oxide exposure at 10 mg m-3. They now require real-time dust monitoring and medical surveillance by July 2027. Compliance upgrades, such as HEPA filtration, quarterly audits, and health tracking, increase costs by USD 50,000 to 150,000 annually per line. This rise in costs has prompted insurers to adjust premiums by 15% to 25%. While large integrated producers are managing these costs, smaller converters are experiencing financial pressure, which could lead to their exit from the market. This development is gradually driving the carbonyl iron powder market toward increased consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Iron-Fortified Micro-Encapsulated Nutraceuticals

- Localized Radar-Absorbing Composites for Autonomous-Vehicle Sensors

- Substitution Threat from Cheaper Water-Atomized Iron Powders

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, reduced grades, pharmaceutical supplements and metal-injection-molding medical parts, requiring oxygen levels of <0.2% and particle sizes between 1-10 µm, accounted for 67.11% of the carbonyl iron powder market under the reduced grades segment. Production depends on reactors operating at ≥ 20 MPa for cycles exceeding 120 hours, achieving iron purity levels above 99.5%. These characteristics ensure adequate green strength and densification surpassing 95% of theoretical standards, meeting the needs of healthcare and nutraceutical applications with relatively stable price sensitivity.

Atomized carbonyl iron powder, produced in 8 MPa reactors over a span of 60 hours, is projected to grow at a 5.88% CAGR. This growth is driven by its tighter D50 distributions of 3-8 µm, which help reduce eddy-current losses in soft magnetic composites, particularly for 50-100 kHz inverter coils. The segment is supported by the increasing adoption of 800-V EV platforms and silicon-carbide inverters in Asia-Pacific's vehicle programs. Suppliers offering pre-insulated atomized grades are gaining traction in high-frequency inductors, where a 1% reduction in core loss results in a 0.5% decrease in charging time. Additionally, dual-line producers capable of both high-pressure reduced and mid-pressure atomized outputs are positioned to maintain margins while addressing the varied demands of the carbonyl iron powder market.

Geography Analysis

In 2025, Asia-Pacific represented 42.27% of the revenue, with a projected 6.31% CAGR through 2031. This growth is supported by China's significant role, holding over 45% of global capacity and a demand exceeding 8,000 tons in 2023. In the first quarter of 2025, Chinese producers announced 12,000 tons of new production lines to cater to customers in Southeast Asia and North America. India, dealing with a 20%-30% premium on landed costs, imported between 1,200 and 1,500 tons in 2025, indicating the need for regional distribution hubs.

In North America, the aerospace, defense, and pharmaceutical sectors drive demand, with a focus on ASTM and USP traceability. American Carbonyl's plant in Alabama plays a key role in the domestic supply. Additionally, Hoganas' biochar substitution initiative is expected to reduce CO2 intensity by 15% by 2026, aligning with OEM Scope 3 targets. In Europe, BASF's site in Ludwigshafen increased capacity by 800 tons in 2023 and is now applying stricter classifications for sub-µm grades. However, Directive 2024/1785 is raising compliance costs, prompting smaller converters to consider consolidation or relocation.

South America and the Middle East & Africa remain fully dependent on imports, facing challenges with lead times of 8 to 12 weeks. Establishing bonded regional warehouses with 500 to 1,000 tons of stock and technical-service centers could enable price premiums of 10% to 15%. This approach is particularly relevant as multinational buyers implement supplier audits aligned with EU and U.S. standards.

- Americal Carbonyl

- BASF

- CNPC Powder

- CRS Holdings, LLC.

- Hoganas AB

- JFE Steel Corporation

- Jiangsu Tianyi Ultra-fine Metal Powder

- Jiangxi Yuean Advanced Materials Co Ltd

- KPT

- Micrometals Inc.

- MUBY Chemicals

- Nanorh

- Rio Tinto

- Shanghai Knowhow Powder-Tech Co.,Ltd

- Sintez-CIP Ltd

- Stanford Advanced Materials

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand in EMI-Shielding Applications

- 4.2.2 Increasing Use in Powder Metallurgy and Automotive Components

- 4.2.3 Adoption in Metal Injection-Molding (MIM) for Complex Parts

- 4.2.4 Expansion of Pharmaceutical Iron-Supplement Production

- 4.2.5 Emerging 3-D-Printed EM-Absorber Structures

- 4.3 Market Restraints

- 4.3.1 High Production Cost and Volatile Iron-Carbonyl Feedstock Supply

- 4.3.2 Health and Environmental Risks from Nano-Particle Inhalation

- 4.3.3 Substitution Threat from Cheaper Atomized Iron Powders

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Reduced Carbonyl Iron Powder

- 5.1.2 Atomized Carbonyl Iron Powder

- 5.2 By Purity Grade

- 5.2.1 Standard (more than or equal to 97% Fe)

- 5.2.2 High-Purity (more than or equal to 99% Fe)

- 5.2.3 Ultra-High-Purity (more than or equal to 99.9% Fe)

- 5.3 By End-user Industry

- 5.3.1 Electronics and Electricals

- 5.3.2 Automotive

- 5.3.3 Healthcare and Pharmaceuticals

- 5.3.4 Aerospace and Defense

- 5.3.5 Industrial Machinery

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Americal Carbonyl

- 6.4.2 BASF

- 6.4.3 CNPC Powder

- 6.4.4 CRS Holdings, LLC.

- 6.4.5 Hoganas AB

- 6.4.6 JFE Steel Corporation

- 6.4.7 Jiangsu Tianyi Ultra-fine Metal Powder

- 6.4.8 Jiangxi Yuean Advanced Materials Co Ltd

- 6.4.9 KPT

- 6.4.10 Micrometals Inc.

- 6.4.11 MUBY Chemicals

- 6.4.12 Nanorh

- 6.4.13 Rio Tinto

- 6.4.14 Shanghai Knowhow Powder-Tech Co.,Ltd

- 6.4.15 Sintez-CIP Ltd

- 6.4.16 Stanford Advanced Materials

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment