PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062154

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062154

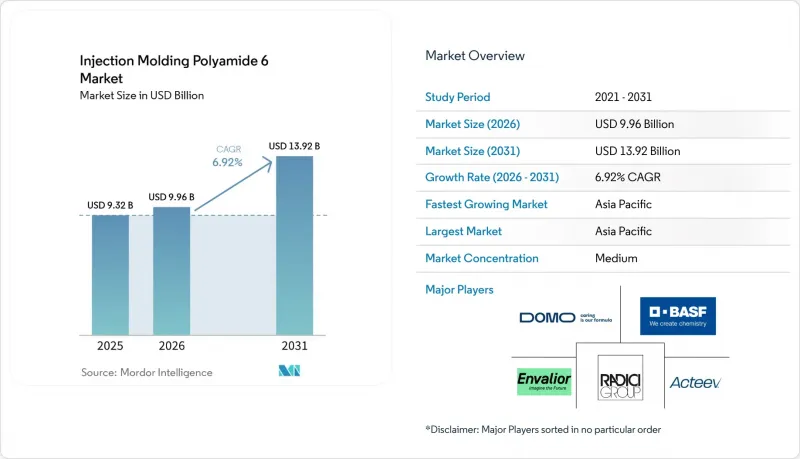

Injection Molding Polyamide 6 - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the injection molding polyamide 6 market size is expected to increase from USD 9.32 billion in 2025 to USD 9.96 billion in 2026 and reach USD 13.92 billion by 2031, growing at a CAGR of 6.92% over 2026-2031.

This report is Segmented by Type (Unfilled PA6, Mineral-Filled PA6, and More), Processing Method (Standard Injection Molding, Gas-Assisted Injection Molding, and More), Application (Automotive Components, Electrical and Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Injection Molding Polyamide 6 Market Trends and Insights

Growth in E&E Miniaturized Components

As high-voltage 800-V vehicle platforms expand, the demand for sub-gram connectors and sensors is increasing. These components require a UL 94 V-0 (Underwriters Laboratories 94 Vertical Burning Test) flame rating and a CTI (Comparative Tracking Index) of less than or equal to 600 V. Glass-fiber-reinforced PA6 grades consistently meet these standards. BASF's Ultramid Advanced N, a specialty polyamide, secured contracts in 2025 with KOSTAL Automotive, replacing liquid-crystal polymer. This demonstrates the ability of specialty polyamides to meet precise 0.03 mm tolerance windows while reducing resin costs by approximately 15%. Additionally, advancements in closed-loop shot-weight control within micro-injection presses now achieve 0.5% repeatability, minimizing dimensional drift and reducing the need for manual rework.

Excellent Mechanical and Thermal Profile of PA6

Unfilled Polyamide 6 (PA6) has a tensile strength of approximately 85 MPa. With a 30% glass loading, this strength increases to 170 MPa, making it a potential lightweight alternative to aluminum die-castings in non-load-bearing brackets. Toray's NANOALLOY-modified grades enhance the tensile modulus by an additional 25%, while maintaining the melt flow required for thin-wall molding. Additionally, PA6's vibration-damping capability reduces interior noise by up to 5 decibels (dB) compared to glass-filled polypropylene. This feature is utilized in instrument-panel cross-car beams.

Regulatory Pressure on Fossil-Based Polymers

Effective November 2025, the European Union's (EU) pellet-loss rule requires zero-discharge upgrades, aimed at minimizing environmental impact. This regulation is projected to reduce Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) margins for smaller compounders by up to 150 basis points. Furthermore, Extended Producer Responsibility (EPR) fees in France and Germany are driving the adoption of bio-based and chemically recycled polyamide 6 (PA6) by making it more cost-competitive.

Other drivers and restraints analyzed in the detailed report include:

- Capacity Expansions in Asia for Glass-Filled Grades

- Adoption in EV Battery Enclosures and E-Axle Housings

- Scrap-Rate Sensitivity in Micro-Injection Molding

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, glass-fiber-reinforced PA6 dominated the injection molding polyamide 6 market, seizing a 48.11% share. This surge was driven by the adoption of 30%-50% glass systems in applications like engine covers, seat frames, and battery-pack brackets, all demanding a modulus of less than or equal to 8,000 MPa. Meanwhile, mineral-filled and impact-modified variants carved out a combined quarter of the market, favored in applications prioritizing low warpage or cold-temperature toughness over stiffness. The other types segment of the injection molding polyamide 6 market, encompassing carbon-fiber, bio-based, and chemically recycled resins, is set to grow at a robust 7.88% CAGR, as OEMs aggressively pursue Scope-3 emission reductions.

Innovations in feedstock are reshaping supply chains, previously tethered to fossil benzene, as seen with BASF's loopamid, RadiciGroup's BIONSIDE PA610, and UBE's ISCC PLUS-certified bio-caprolactam. Concurrently, Envalior's Durethan FLX-RTM is carving out niches in rotational-molded pressure vessels. This trend underscores a market fragmentation, with a clear shift in value from generic unfilled grades to specialized engineered solutions that meet durability and sustainability benchmarks, all without the typical requalification holdups.

Geography Analysis

Asia-Pacific, accounting for 50.11% of the 2025 volume, is projected to grow at a 7.78% compound annual growth rate (CAGR) through 2031. In late 2025, China will activate new plants with a capacity of 922 kilotons per year, primarily focusing on exporting 30-50% glass compounds. Meanwhile, India's capacity expansions in Panoli and Thane are supporting domestic electric vehicle (EV) initiatives, driven by incentives from the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) scheme. Both Japan and South Korea are commercializing premium nano-modified and bio-circular variants, which, while commanding a 20-30% price uplift, also address the tightening carbon footprints of original equipment manufacturers (OEMs).

In North America, the reshoring of battery-component molding, spurred by the Inflation Reduction Act (IRA), is evident with Ascend's expansion of the ReDefyne mechanical-recycling capacity in Alabama. U.S. production lines are operating at over 85% utilization, leading Celanese to impose a USD 0.25 per kilogram surcharge in February 2026. Meanwhile, Canada's auto-parts trade, aligned with the United States-Mexico-Canada Agreement (USMCA), ensures a steady flow of polyamide 6 (PA6) intake manifolds and coolant reservoirs to the U.S., solidifying binational supply chains.

Europe, while managing costs from pellet-loss and extended producer responsibility (EPR) levies, maintains its leadership in material development. This is exemplified by BASF's complete acquisition of the Alsachimie joint venture, securing adipic acid and hexamethylenediamine (HMD) precursors within the bloc. German OEMs are leading the adoption of recycled content, aiming to meet the Ecodesign for Sustainable Products Regulation (ESPR)'s 25% threshold by 2028. In contrast, the UK's differing standards are extending qualification cycles. Latin America, with a focus on engine covers, is leveraging Brazil's ethanol-resistant formulations. Meanwhile, demand in the Middle East and Africa, though still in its early stages, is increasing with Saudi Arabia's EV assembly and South Africa's mining equipment.

- Arkema

- Asahi Kasei Corporation

- Ascend Performance Materials

- BASF

- Celanese Corporation

- Domo Chemicals

- EMS-CHEMIE HOLDING AG

- Ensinger

- Envalior

- Evonik Industries AG

- Kingfa Sci.&Tech. Co.,Ltd.

- LG Chem

- Mitsui Chemicals, Inc.

- Radici Partecipazioni SpA

- RTP Company

- SABIC

- Solvay

- Toray Industries, Inc.

- UBE Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in E&E miniaturised components

- 4.2.2 Excellent mechanical and thermal profile of PA6

- 4.2.3 Capacity expansions in Asia for glass-filled grades

- 4.2.4 Adoption in EV battery enclosures and e-axle housings

- 4.2.5 Rapid-heating thin-wall molding technologies boosting PA6 penetration

- 4.3 Market Restraints

- 4.3.1 Regulatory pressure on fossil-based polymers

- 4.3.2 Scrap-rate sensitivity in micro-injection molding

- 4.3.3 Low thermal margin vs PA66 for >150 °C under-hood parts

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Unfilled PA6

- 5.1.2 Glass-fiber-reinforced PA6

- 5.1.3 Mineral-filled PA6

- 5.1.4 Impact-modified PA6

- 5.1.5 Other Types (carbon-fiber, bio-based, recycled)

- 5.2 By Processing Method

- 5.2.1 Standard injection molding

- 5.2.2 Gas-assisted injection molding

- 5.2.3 Micro-injection molding

- 5.2.4 Other Processing Methods (water-assist, metal-insert)

- 5.3 By Application

- 5.3.1 Automotive Components

- 5.3.2 Electrical and Electronics

- 5.3.3 Industrial Machinery and Equipment

- 5.3.4 Consumer Goods (power tools, appliances)

- 5.3.5 Other Applications (Packaging, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Arkema

- 6.4.2 Asahi Kasei Corporation

- 6.4.3 Ascend Performance Materials

- 6.4.4 BASF

- 6.4.5 Celanese Corporation

- 6.4.6 Domo Chemicals

- 6.4.7 EMS-CHEMIE HOLDING AG

- 6.4.8 Ensinger

- 6.4.9 Envalior

- 6.4.10 Evonik Industries AG

- 6.4.11 Kingfa Sci.&Tech. Co.,Ltd.

- 6.4.12 LG Chem

- 6.4.13 Mitsui Chemicals, Inc.

- 6.4.14 Radici Partecipazioni SpA

- 6.4.15 RTP Company

- 6.4.16 SABIC

- 6.4.17 Solvay

- 6.4.18 Toray Industries, Inc.

- 6.4.19 UBE Corp.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment