PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062161

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062161

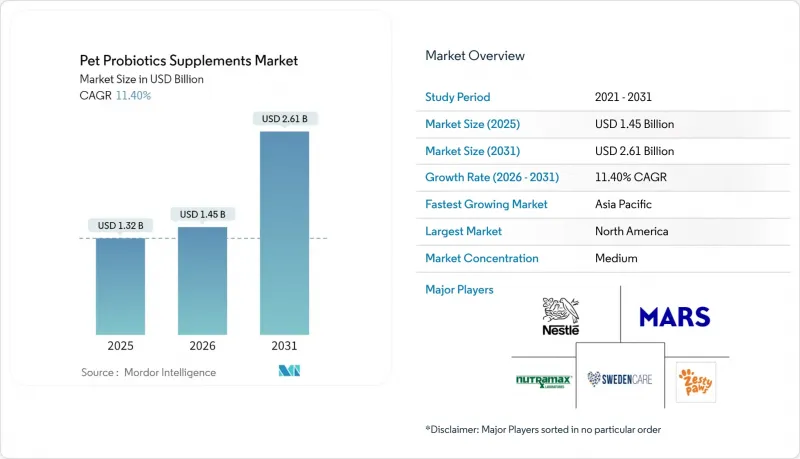

Pet Probiotics Supplements - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the pet probiotics supplements market was valued at USD 1.32 billion in 2025 and is projected to grow from USD 1.45 billion in 2026 to USD 2.61 billion by 2031, registering a CAGR of 11.4% between 2026 and 2031.

This report is Segmented by Pet Type (Dogs, and More), by Form (Chewable, and More), by Distribution Channel (Online Retail, and More), by Function-Health Benefit (Digestive Health, Immune Support and More), by Ingredient Source (Bacteria-Based Probiotics and More) and by Geography (North America, Europe, Africa, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Global Pet Probiotics Supplements Market Trends and Insights

Rising Pet Humanization and Premiumization Driving Demand

According to the American Pet Products Association (APPA) 2025, the United States pet industry expenditures reached USD 152 billion in 2024. Additionally, pet owners maintained their spending levels despite economic fluctuations, highlighting the emphasis on advanced pet wellness through specialized distribution channels. Growing awareness of the benefits of probiotics in supporting pet health, including improved digestion, enhanced immunity, and overall well-being. Bundled products that combine probiotics with joint or calming supplements are increasing basket value, offering a more comprehensive approach to pet care.

Increasing Veterinary Endorsements for Gut-Health Probiotics

Veterinary clinical studies indicate that probiotics are effective in managing canine acute diarrhea, demonstrating benefits such as a shorter duration of symptoms and improved gut health outcomes . Veterinary clinics now stock probiotic chewables at checkout counters, where point-of-care recommendations have proven effective in driving sales. Partnerships with big-box pharmacies are extending the reach of probiotics beyond traditional veterinary offices. Professional endorsements are also raising documentation standards, compelling brands to publish strain-specific data, which helps distinguish probiotics from general wellness products.

Regulatory Ambiguity Around Strain-Specific Claims

The Food and Drug Administration (FDA) Center for Veterinary Medicine classifies most probiotics as feed ingredients, making pre-market efficacy trials voluntary. Product labels are permitted to claim general benefits such as "supports digestive health," but they are prohibited from asserting disease treatment, which can lead to confusion among consumers. Currently, some of the probiotic brands display the National Animal Supplement Council (NASC) seal, leaving the majority of products without NASC oversight or auditing. In Europe, the European Pet Food Industry Federation (FEDIAF) requires strain identification but does not mandate outcome data, creating inconsistencies in global regulatory standards.

Other drivers and restraints analyzed in the detailed report include:

- Rapid E-Commerce Penetration Widening Access to Supplements

- DNA-Based Microbiome Testing Enabling Personalized Blends

- Limited Longitudinal Clinical Evidence Affecting Confidence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dogs accounted for the largest 63% of the pet probiotics supplements market share in 2025, driven by established veterinary protocols recommending Enterococcus-based blends for managing acute diarrhea and chronic inflammatory enteropathy. Cats trailed behind due to challenges in ensuring daily compliance. However, a 2025 study utilizing Saccharomyces cerevisiae DSM 34246 demonstrated measurable improvements in fecal immunoglobulin A levels, indicating potential strain-specific adoption among cat owners. The pet probiotics supplements market size for small mammals is projected to grow at the fastest CAGR of 15.4% from 2026 to 2031, supported by increased exotic-pet adoption and advancements in research on cecal microbiome modulation.

Birds and fish, categorized under "other pets," are benefiting from antibiotic-free aquaculture mandates, which have highlighted Bacillus subtilis and Lactobacillus plantarum as immune enhancers and water-quality modulators. Ornamental birds, such as parrots and cockatiels, often experience stress-induced enteritis, which has been shown to respond to Lactobacillus reuteri supplementation. This represents a niche that mainstream brands have yet to address fully. This category also encompasses reptiles and amphibians, where probiotic applications are still in the experimental stage. Early trials indicate that Bacillus strains may help address dysbiosis in captive-bred iguanas and tree frogs.

Chewables accounted for the largest 37.4% of the pet probiotics supplements market share in 2025, as chicken-liver and cheese flavor systems effectively mask the bitterness of probiotics, ensuring daily compliance by pet owners, a critical factor for sustained gut colonization. Powders remain a cost-effective option for multi-pet households. However, exposure to humidity can result in clumping and CFU (colony-forming unit) loss, which may reduce repeat-purchase intent. Capsules are commonly used in veterinary channels due to their tamper-evident packaging and clearly labeled CFU counts, although cats and toy breeds often resist pill intake.

The market size for liquid pet probiotic supplements is projected to achieve a fastest 12.8% CAGR from 2026 to 2031, particularly favored for use in birds, fish, and felines, where syringe or dropper dosing minimizes stress. Emerging gels and pastes combine the dosing precision of liquids with the shelf stability of powders, making them suitable for post-surgical applications. Bake-stable spore-forming strains enable soft treats to function as both supplements and snacks, although high oven temperatures still require microencapsulation. Ongoing format innovations ensure that the pet probiotic supplements market remains adaptable to evolving owner preferences for convenience and palatability.

Geography Analysis

North America is projected to hold the largest market share of 43% in the pet probiotics supplement market in 2025. This dominance is driven by high companion animal ownership, a well-established network of veterinary clinics, and the adoption of data-driven direct-to-consumer platforms such as Purina Petivity and AnimalBiome. These platforms leverage fecal sequencing to provide strain-specific recommendations. The United States leads the region in terms of volume, with online sales accounting for a significant portion of pet supplement spending. Subscription-based purchases represent a growing segment of the market.

The Asia-Pacific market size is projected to grow at the fastest 12.1% CAGR from 2026 to 2031, driven by increased companion animal spending in urban Chinese households. In Japan, regulatory changes now permit health claims for Lactobacillus and Bifidobacterium under its feed-additive framework, enabling the development of functional snacks that bypass drug registration requirements. Australia combines high pet ownership with strong veterinary influence, though its small population limits overall market volume. India and Southeast Asian economies rely heavily on e-commerce due to limited veterinary clinic density.

Europe, the Middle East, Africa, South America, and Russia exhibit fragmented adoption patterns. Germany, France, and the United Kingdom lead under the Federation of European Companion Animal Veterinary Associations guidelines, which mandate strain identification but do not require efficacy proof. This allows for quick product cycles but results in variable clinical backing. In the Middle East, the United Arab Emirates and Saudi Arabia are experiencing growth due to expatriate pet ownership and premium retail expansion, though cultural norms limit penetration into mainstream households. In Africa, South Africa and Egypt remain niche markets as counterfeit risks and affordability challenges deter branded importers.

- Nestle Purina PetCare Company

- Mars, Incorporated

- Nutramax Laboratories, Inc.

- Elanco Animal Health Incorporated

- Zesty Paws, LLC

- Swedencare AB (publ)

- NOW Health Group, Inc.

- Virbac S.A.

- Novonesis Group A/S

- PetLab Co. Ltd.

- AdvaCare Pharma LLC

- PetHonesty, LLC.

- Pet Naturals (FoodScience LLC)

- Fera Pets, Inc. (General Mills Inc.)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising pet humanization and premiumization driving demand

- 4.2.2 Increasing veterinary endorsements for gut-health probiotics

- 4.2.3 Rapid e-commerce penetration widening access to supplements

- 4.2.4 DNA-based microbiome testing enabling personalized blends

- 4.2.5 Aquaculture antibiotic stewardship boosting "other pets" demand

- 4.2.6 Next-gen postbiotic formulations improving shelf life

- 4.3 Market Restraints

- 4.3.1 Regulatory ambiguity around strain-specific claims

- 4.3.2 Limited longitudinal clinical evidence affecting confidence

- 4.3.3 Fermentation-capacity bottlenecks for spore-forming probiotics

- 4.3.4 Raw-diet movement reducing perceived supplement need

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Pet Type

- 5.1.1 Dogs

- 5.1.2 Cats

- 5.1.3 Others Pet Types

- 5.2 By Form

- 5.2.1 Chewables

- 5.2.2 Powder

- 5.2.3 Capsules and Tablets

- 5.2.4 Liquids

- 5.2.5 Other Forms

- 5.3 By Distribution Channel

- 5.3.1 Online Retail

- 5.3.2 Veterinary Clinics

- 5.3.3 Pet Specialty Stores

- 5.3.4 Mass-Market Retailers

- 5.3.5 Other Distribution Channels

- 5.4 By Function (Health Benefit)

- 5.4.1 Digestive Health

- 5.4.2 Immune Support

- 5.4.3 Oral Health

- 5.4.4 Skin and Coat

- 5.4.5 Joint Health

- 5.4.6 Anxiety and Stress

- 5.4.7 Other Functions

- 5.5 By Ingredient Source

- 5.5.1 Bacteria-based Probiotics (Lactobacillus, Bifidobacterium)

- 5.5.2 Yeast-based Probiotics (Saccharomyces)

- 5.5.3 Synbiotic Blends

- 5.5.4 Spore-forming Probiotics

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.1.4 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Russia

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 Australia

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global overview, Market overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nestle Purina PetCare Company

- 6.4.2 Mars, Incorporated

- 6.4.3 Nutramax Laboratories, Inc.

- 6.4.4 Elanco Animal Health Incorporated

- 6.4.5 Zesty Paws, LLC

- 6.4.6 Swedencare AB (publ)

- 6.4.7 NOW Health Group, Inc.

- 6.4.8 Virbac S.A.

- 6.4.9 Novonesis Group A/S

- 6.4.10 PetLab Co. Ltd.

- 6.4.11 AdvaCare Pharma LLC

- 6.4.12 PetHonesty, LLC.

- 6.4.13 Pet Naturals (FoodScience LLC)

- 6.4.14 Fera Pets, Inc. (General Mills Inc.)

7 Market Opportunities and Future Outlook