PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062166

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062166

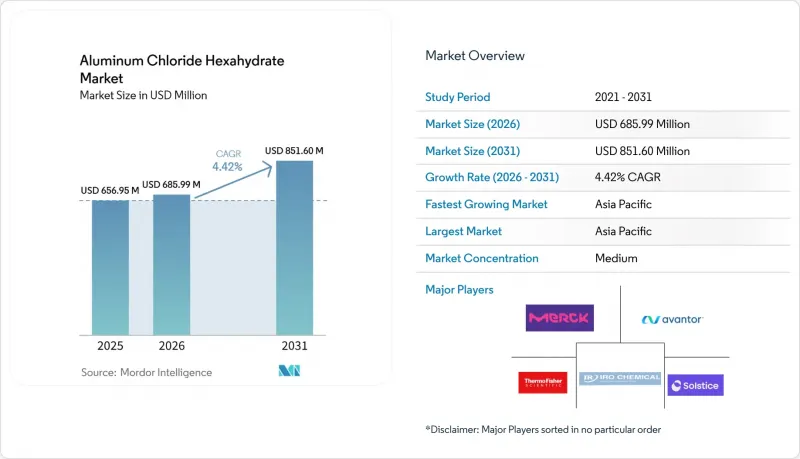

Aluminum Chloride Hexahydrate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the aluminum chloride hexahydrate market size is projected to be USD 656.95 million in 2025, USD 685.99 million in 2026, and reach USD 851.60 million by 2031, growing at a CAGR of 4.42% from 2026 to 2031.

This report is Segmented by Purity (Less Than 99%, Between 99% To 99. 5%, Greater Than 99. 5%), Application (Water Treatment, Pharmaceuticals, and More), End-User Industry (Chemical, Healthcare and Life-Sciences, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Aluminum Chloride Hexahydrate Market Trends and Insights

Expanding API Synthesis in Emerging-Market Pharmaceutical Clusters

Western drugmakers have relocated 60-70% of their intermediate production to Asia, reducing costs by up to 50%. This cost efficiency has resulted in a steady demand for catalytic grades with purity levels of 99-99.5% that adhere to FDA and EMA residue limits. The addition of new API capacities in Gujarat, Hyderabad, Jiangsu, and Zhejiang is increasing at an annual rate of 20-30%. However, stricter discharge regulations in China and India are influencing the preference for aluminum catalysts instead of ferric or zinc alternatives.

Scale-Up of Lewis-Acid Catalysis for Biomass-to-Chemicals Routes

Pilot biorefineries are converting corn stover and bagasse into 5-HMF and levulinic acid, with aluminum chloride hexahydrate being increasingly selected as a catalyst. This is driven by its ability to cleave lignin ether bonds under milder conditions compared to mineral acids. The economic feasibility of these processes depends on the recovery of this highly soluble catalyst. Current membrane systems contribute an additional cost of USD 0.15-0.25 per kg of product. Consequently, broader adoption is expected to follow the maturation of integrated, closed-loop projects in Europe after 2028.

Substitution by Alum and Polyaluminum Chloride in Bulk Coagulation

PAC reduces COD/BOD levels by 60-80% with half the aluminum dose. This results in cost savings for utilities of USD 0.02-0.04 per m3 while complying with the EU Directive 2020/2184's residual-Al cap of 200 µg/L. Similarly, China's GB 15892-2020 supports PAC's application. Currently, PAC is priced at USD 180-220 per MT, compared to USD 250-300 for hexahydrate, which impacts commodity demand.

Other drivers and restraints analyzed in the detailed report include:

- Commercialization of AlCl3-Based Deep-Eutectic Electrolytes for Next-Gen Batteries

- Growth of Precision Additive-Manufacturing Feedstocks

- Tight Anhydrous AlCl3 Supply Chains Causing Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, the 99-99.5 % purity segment accounted for 53.11 % of the revenue, driven by consistent demand in API, textiles, and water treatment. Economies of scale in China and India have supported pricing within the range of USD 1.20-1.50 /kg for aluminum chloride hexahydrate. The greater than 99.5 % ultra-high-purity segment is projected to grow at a 4.87 % CAGR, supported by increasing applications in deep-eutectic batteries and compliance with EU REACH catalyst mandates. Several producers have adopted fractional-crystallization units to enhance mid-grade stock at an additional cost of USD 0.30-0.50 /kg, focusing on higher-margin niches. The <99 % purity segment now represents only 12-15 % of the total volume, as PAC continues to replace it in southern-Asia municipal tenders.

Stricter regulatory requirements are shaping this segmental dynamic. Arsenic limits set by the EU and China, capped at <1 ppm, have reduced the viability of low-grade lots, prompting capacity upgrades or market exits.

Geography Analysis

Asia-Pacific, which accounts for 47.78% of 2025 sales, is projected to grow at a 5.76% CAGR through 2031. In China, vertical integration achieves costs of USD 1.10-1.40/kg, but stricter discharge regulations are leading to the closure of smaller plants, resulting in higher purity averages. In India, the Gujarat and Hyderabad corridors are increasing API capacity by 20-30% annually, driven by rising local demand. Vietnam's 30,000-ton PAC complex, expected to become operational in 2026, is anticipated to shift some coagulation expenditures while increasing the region's demand for high-grade hexahydrate, a key PAC feedstock catalyst.

In North America, the reshoring of CMOs and EPA's green-chemistry incentives are driving demand for high-purity products, although water-treatment volumes are stabilizing due to the PAC shift. Mexico, benefiting from the USMCA, is gradually expanding its capacity with a focus on automotive paints and packaging grades. In Europe, REACH criteria are encouraging the adoption of>99.5% purity standards. Merck's EUR 3 billion investment in life sciences reflects the focus on regulated niches. However, southern Europe's municipal tenders are experiencing reduced activity due to PAC substitutions.

In South America and the Middle East-Africa, growth is supported by Brazil's pulp-and-paper sector and water-scarcity initiatives in the Gulf. Nevertheless, currency fluctuations and logistical challenges are limiting the pace of growth.

- Alpha Chemika

- Avantor, Inc.

- GFS Chemicals Inc

- Solstice Advanced Materials Inc.

- IRO GROUP INC

- Jinan Haohua Industry

- Merck KGaA

- Otto Chemie Pvt. Ltd.

- Sisco Research Laboratories Pvt. Ltd.

- Spectrum Chemical

- Strem Chemicals

- Thermo Fisher Scientific Inc.

- Tianjin Kaifeng

- YIXING BLUWAT CHEMICALS CO., LTD.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding API synthesis in emerging-market pharmaceutical clusters

- 4.2.2 Scale-up of Lewis-acid catalysis for biomass-to-chemicals routes

- 4.2.3 Commercialization of AlCl3-based deep-eutectic electrolytes for next-gen batteries

- 4.2.4 Growth of precision additive-manufacturing feedstocks

- 4.2.5 Mandates for high-purity catalysts in green fine-chemicals production

- 4.3 Market Restraints

- 4.3.1 Substitution by alum and poly-aluminum chloride in bulk coagulation

- 4.3.2 Tight anhydrous AlCl3 supply chains causing price volatility

- 4.3.3 Shift toward "aluminum-free" consumer-care formulations

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Purity

- 5.1.1 Less than 99 %

- 5.1.2 Between 99 % to 99.5 %

- 5.1.3 Greater than 99.5 %

- 5.2 By Application

- 5.2.1 Water Treatment

- 5.2.2 Pharmaceuticals

- 5.2.3 Cosmetics and Antiperspirants

- 5.2.4 Dyes and Pigments

- 5.2.5 Catalyst and Chemical Synthesis

- 5.2.6 Others

- 5.3 By End-user Industry

- 5.3.1 Chemical

- 5.3.2 Healthcare and Life-sciences

- 5.3.3 Personal-care and Cosmetics

- 5.3.4 Textile

- 5.3.5 Pulp and Paper

- 5.3.6 Others

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Alpha Chemika

- 6.4.2 Avantor, Inc.

- 6.4.3 GFS Chemicals Inc

- 6.4.4 Solstice Advanced Materials Inc.

- 6.4.5 IRO GROUP INC

- 6.4.6 Jinan Haohua Industry

- 6.4.7 Merck KGaA

- 6.4.8 Otto Chemie Pvt. Ltd.

- 6.4.9 Sisco Research Laboratories Pvt. Ltd.

- 6.4.10 Spectrum Chemical

- 6.4.11 Strem Chemicals

- 6.4.12 Thermo Fisher Scientific Inc.

- 6.4.13 Tianjin Kaifeng

- 6.4.14 YIXING BLUWAT CHEMICALS CO., LTD.

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment