PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062175

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062175

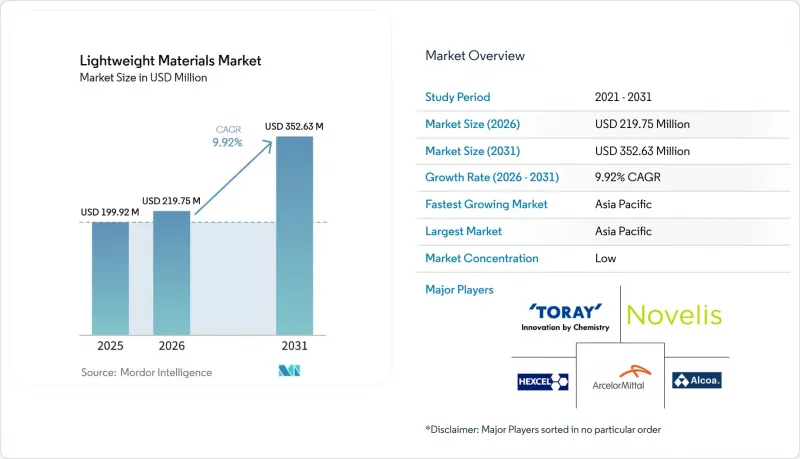

Lightweight Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the lightweight materials market size was valued at USD 199.92 million in 2025 and is estimated to grow from USD 219.75 million in 2026 to reach USD 352.63 million by 2031, at a CAGR of 9.92% during the forecast period (2026-2031).

This report is Segmented by Product Type (Polymers and Composites and Metals), Manufacturing Process (Extrusion and Rolling, Additive Manufacturing, and More), End-User Industry (Automotive, Aerospace and Defense, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Lightweight Materials Market Trends and Insights

Stricter Global CO2 and Fuel-Economy Regulations

Fleet-average carbon ceilings set by the European Union (EU), China, and the United States (U.S.) are prompting automakers to reduce 100-150 kilograms (kg) from every new platform. The EU imposes penalties of EUR 95 for each gram of excess CO2 per car. As a result, lightweight closures, subframes, and seat structures have become essential compliance measures. China's updated dual-credit scheme provides bonus credits for New Energy Vehicles (NEVs) consuming below 11 kilowatt-hours (kWh)/100 kilometers (km), a target that is challenging to meet without aluminum body-in-white and magnesium interior castings. The U.S. Environmental Protection Agency's (EPA) 2024 directive for model years 2027-2032 targets a 56% reduction in fleet-wide CO2 emissions from 2026 levels. This regulation is driving Original Equipment Manufacturers (OEMs) to adopt high-strength aluminum and Carbon Fiber Reinforced Polymer (CFRP) to offset battery mass. Consequently, the lightweight materials market is positioned at the intersection of vehicle design and regulatory compliance.

Hydrogen Storage and Distribution Weight Limits

The Department of Energy (DOE) mandates that light-duty fuel-cell vehicles must store 5.5 weight percent (wt%) hydrogen at 700 bar. This performance is achievable only with Type IV CFRP vessels, which weigh between 90 and 110 kg for a 5 kg hydrogen payload. Heavy-duty trucks face similar requirements: Nikola's eight-tank module carries 70 kg of hydrogen while keeping the total assembly mass under 500 kg, ensuring compliance with U.S. axle-weight limits. Japan has allocated USD 250 million in 2025 subsidies for hydrogen stations, each requiring 15-20 storage modules. This initiative is expected to increase domestic carbon-fiber demand by 8,000 tons annually. The structural demand for CFRP tanks provides a stable foundation for the lightweight materials market, independent of fluctuations in the aerospace or automotive industries.

Energy-Intensive Extraction and Processing

Primary aluminum smelting consumes 15-16 MWh per ton and is subject to electricity cost fluctuations. This was demonstrated in 2023 when European power price increases led to 800 kilotons of capacity being taken offline. Producing carbon fiber requires 80-110 MWh per ton during precursor oxidation and carbonization. The Kroll process for titanium production demands 60-80 MWh per ton and generates magnesium-chloride waste. High power requirements increase costs and scope-1 carbon emissions, potentially impacting the lightweight materials market unless technologies like inert-anode aluminum (ELYSIS) and electrified titanium processes achieve large-scale commercialization.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Aerospace and Reusable-Launch Adoption

- AI-Driven Generative-Design Mass Optimization

- Mixed-Material End-of-Life Separation Hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, carbon-fiber-reinforced and glass-fiber-reinforced polymers accounted for 64.42% of the revenue, supported by a 1.2 million tons annual demand for wind blades and a near-recovery of Boeing 787 and Airbus A350 production rates to pre-pandemic levels. Glass fiber remains prevalent in cost-sensitive construction, while high-temperature polymers like polyether ether ketone (PEEK) and polyetherimide (PEI) are gaining traction in battery housings and electric motor insulators, particularly where flame-smoke toxicity regulations exclude metals. The market for composite lightweight materials is expected to grow further, driven by thermoplastic tapes enabling 3-4 minute cycle times suitable for automotive lift gates.

Metals are projected to grow at a 9.28% compound annual growth rate (CAGR) through 2031, driven by aluminum giga-casting, China's magnesium mandate, and advancements in titanium additive manufacturing. Closed-loop aluminum, with 90% recycled content and a carbon dioxide (CO2) footprint of 2.3 tons CO2/ton, complies with Carbon Border Adjustment Mechanism (CBAM) thresholds, enabling original equipment manufacturers (OEMs) to label products as near-carbon-neutral. The market share for magnesium in lightweight materials is expected to increase as corrosion-resistant plasma-electrolytic-oxidation coatings become more cost-effective, potentially dropping below USD 8/kg. Titanium remains specialized, but Norsk Titanium's rapid-plasma-deposition technology reduces buy-to-fly ratios from 10-20% to under 2%, lowering aerospace alloy costs by 30-40%.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 41.12% of the lightweight materials market. Projections indicate this share will grow at a 9.77% compound annual growth rate (CAGR), extending to 2031. China's eight-ministry magnesium initiative is expected to increase domestic automotive demand by 5.3 times, reaching 80,000 tons by 2028. In Japan, subsidies for hydrogen refueling stations are anticipated to raise carbon-fiber precursor capacity by 8,000 tons annually. South Korea's KRW 450 billion (USD 0.29 billion) joint venture between Toray and SK is set to produce 3,000 tons of carbon fiber, catering to aerospace and fuel-cell vehicles.

Europe contributes significantly to global demand. In 2025, German original equipment manufacturers (OEMs) consumed nearly 200 kilotons of aluminum sheets. Looking ahead, ArcelorMittal's hydrogen-driven direct reduced iron (DRI) line in Dunkirk is projected to supply 1.5 million tons of low-carbon steel for European electric vehicle (EV) battery enclosures starting in 2026. However, Brexit-induced customs frictions have shifted 15% of the United Kingdom's (UK) composite wing production to continental plants, highlighting the industry's sensitivity to policy changes.

North America is experiencing steady growth, supported by Novelis's 600 kiloton recycling expansion in Kentucky and Tesla's adoption of giga-casting at its Monterrey and Austin facilities. While Canada's composite fuselage sector is facing challenges due to declining business-jet volumes, the decrease is largely offset by demand for United States (U.S.) launch vehicles. Mexico is benefiting from Tier-1 relocations aligning with the United States-Mexico-Canada Agreement (USMCA) rules-of-origin requirements for battery supply chains, enhancing the region's share in the lightweight materials market.

- Alcoa Corporation

- ArcelorMittal

- Covestro

- CRS Holdings, LLC

- ExxonMobil

- Gestamp

- Hexcel Corporation

- Norsk Titanium US Inc.

- Novelis Inc.

- SABIC

- SGL Carbon

- Solvay

- Toray Industries Inc.

- US Magnesium LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Fuel-Efficient and High-Performance Vehicles

- 4.2.2 Expansion of EV And Battery-Electric Platforms

- 4.2.3 Stringent Global Emission and Fuel-Economy Regulations

- 4.2.4 Rapid Adoption in Commercial Aerospace and Space Launch

- 4.2.5 Lightweighting Needs in Hydrogen Storage and Distribution

- 4.3 Market Restraints

- 4.3.1 High and Volatile Prices of Critical Raw Materials

- 4.3.2 Energy-Intensive Extraction and Processing Routes

- 4.3.3 Recycling and End-of-Life Separation Challenges

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Polymers and Composites

- 5.1.1.1 CFRP

- 5.1.1.2 GFRP

- 5.1.1.3 Thermoplastic Composites

- 5.1.1.4 High-performance Polymers (PEEK, PEI)

- 5.1.2 Metals

- 5.1.2.1 Aluminium

- 5.1.2.2 Magnesium

- 5.1.2.3 Titanium

- 5.1.2.4 High-strength Steel

- 5.1.1 Polymers and Composites

- 5.2 By Manufacturing Process

- 5.2.1 Extrusion / Rolling

- 5.2.2 Additive Manufacturing

- 5.2.3 Resin Transfer Molding

- 5.2.4 Hot Stamping and Hydroforming

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Aerospace and Defense

- 5.3.3 Construction

- 5.3.4 Energy (Wind, Hydrogen)

- 5.3.5 Marine

- 5.3.6 Other Industries (Sports, Rail, Packaging)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Mexico

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Alcoa Corporation

- 6.4.2 ArcelorMittal

- 6.4.3 Covestro

- 6.4.4 CRS Holdings, LLC

- 6.4.5 ExxonMobil

- 6.4.6 Gestamp

- 6.4.7 Hexcel Corporation

- 6.4.8 Norsk Titanium US Inc.

- 6.4.9 Novelis Inc.

- 6.4.10 SABIC

- 6.4.11 SGL Carbon

- 6.4.12 Solvay

- 6.4.13 Toray Industries Inc.

- 6.4.14 US Magnesium LLC

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Circular Economy and Recycling Innovation

- 7.3 Lightweight Materials for Hydrogen Economy