PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062178

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062178

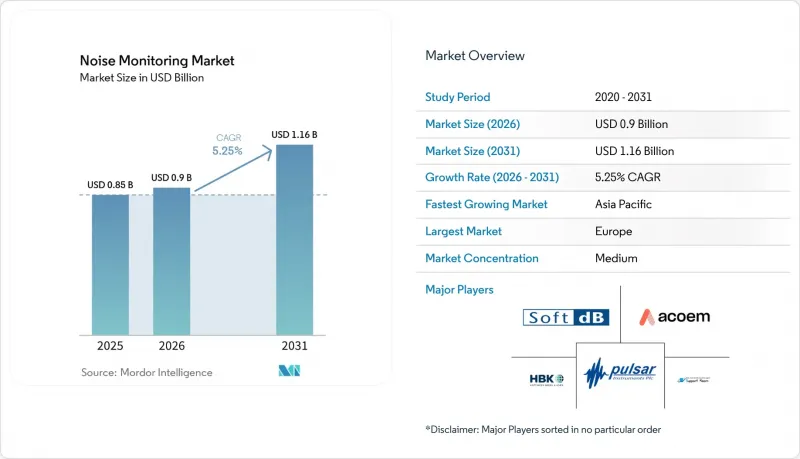

Noise Monitoring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the noise monitoring market size is projected to expand from USD 0.85 billion in 2025 and USD 0.90 billion in 2026 to USD 1.16 billion by 2031, registering a 5.25% CAGR between 2026 and 2031.

This report is Segmented by Component (Hardware, Software, and Services), Product Type (Fixed/Permanent, Portable, Wearable Dosimeters, Remote Kiosks, and More), Technology (Real-Time, IoT-Enabled, Cloud-Based Analytics, AI-Powered Predictive Analytics, and More), Application (Construction, Industrial, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Global Noise Monitoring Market Trends and Insights

Stricter Environmental Noise Regulations

New regulations convert once-optional monitoring into a procurement requirement. Ireland's draft guidance mandates CNOSSOS-EU methodology, recent input data, and validation of candidate mitigation areas, which expands demand for precision sensors and modeling tools. In the United States, the Federal Highway Administration proposes state-level inventories and model validation within +-3 dB, pushing agencies to deploy continuous networks that feed approved software. Municipal rules such as New York City's 2026 mandate for automated API uploads further accelerate the adoption of cloud-integrated devices. Vendors that certify to IEC 61672-1 and EN ISO 3744:2010 secure preferential status in public tenders.

Growth of Smart Cities and Urban Expansion

Noise sensors are now embedded within multiparameter platforms that also track traffic, air quality, and micro-climate data. Barcelona's TRAFFIC-NOISE project links acoustic and visual analytics to manage congestion in real time, illustrating how municipalities buy integrated stacks rather than stand-alone meters. Australia's OpenAIR program funds networked sensors across 13 local councils, using open protocols to future-proof procurement. Early adopters prefer suppliers offering ready-to-consume APIs and dashboard widgets that fit existing city operating systems, reshaping competition toward software openness.

High Capital and Maintenance Costs

Class 1 instrumentation, calibrated microphones, and secure cloud subscriptions strain small-city budgets. New York City's specification for outdoor-rated devices with compliant mounting heights illustrates how premium hardware and periodic recalibration inflate lifecycle cost. Vendors respond with subscription models that convert capex to opex, such as fleet-based pricing in the mining sector. Yet emerging markets still gravitate toward lower-accuracy alternatives, risking data gaps that undermine policy decisions.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Construction and Infrastructure Projects

- Rising Public Awareness of Noise-Related Health Impacts

- Data-Privacy Hurdles in Continuous Monitoring

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services outpace hardware as clients seek turnkey compliance and analytics. Although equipment sales dominated the noise monitoring market in 2025, recurring contracts for calibration, cloud dashboards, and expert interpretation are forecast to grow faster, pushing the overall services share upward. Cirrus Research's expanded NoiseTools suite exemplifies how software upgrades anchor installed devices and create upsell paths. Government agencies such as the European Environment Agency earmark dedicated budgets for data processing and machine-learning pilots, reinforcing demand for specialized consultancies.

Service providers leverage long-term agreements to bundle hardware leasing, remote diagnostics, and standards compliance audits, buffering revenue against hardware refresh cycles. This migration aligns vendor incentives with customer outcomes, supporting higher margins and stickier relationships across the noise monitoring market.

Fixed networks remain indispensable for urban noise maps, yet wearable dosimeters are gaining traction in occupational health programs. Continuous exposure tracking for mobile workers in aviation maintenance, mining haulage, and manufacturing floors accelerates uptake of clip-on sensors that log personal sound dose. New regulations in construction hotspots, such as New York City's rule for projects within 50 feet of residences, still favour rugged fixed stations with weatherproof microphones.

Wearables complement these networks by confirming individual compliance with exposure limits and delivering real-time vibration or sound feedback to workers. Vendors integrating Bluetooth connectivity and cloud synchronization position wearables as an extension of enterprise safety platforms, smoothing data correlation with area monitors and widening the addressable noise monitoring market.

Geography Analysis

Europe anchors global revenues through the Environmental Noise Directive's five-year reporting cadence and standardized CNOSSOS-EU methodology, which obliges cities to refresh noise maps and public action plans. National initiatives such as Italy's highway abatement program and Scotland's designation of quiet areas reinforce pipeline visibility.

Asia-Pacific is the fastest-growing region, buoyed by smart-city pilots and megaprojects. Australia's OpenAIR network and the University of Technology Sydney's noise-camera trial exemplify government-funded deployments that blend low-cost sensors with advanced analytics. Rapid urbanization across Southeast Asia and India adds municipal customers focused on affordable, scalable nodes and cloud dashboards.

North America benefits from updated federal guidance and stringent city ordinances. New York City's continuous monitoring rule spurs immediate procurement, while the Federal Highway Administration's forthcoming inventory mandate primes state departments for multiyear hardware and software purchases. South America and the Middle East and Africa trail in revenue but show momentum in mining belts and infrastructure corridors where environmental permits hinge on continuous sound logging. Regional diversity in standards drives demand for modular platforms that adapt firmware and reporting templates without wholesale hardware swaps, safeguarding vendor margins within the noise monitoring market.

- Hottinger Bruel & Kjaer GmbH

- Acoem Group

- Larson Davis (PCB Piezotronics)

- RION Co., Ltd.

- Svantek

- Cirrus Research

- NTi Audio

- Casella (IDEAL Industries)

- Pulsar Instruments Plc

- G.R.A.S Sound and Vibration

- Norsonic AS

- Soft dB

- SINUS Messtechnik

- Extech Instruments (FLIR)

- TES Electrical Electronic Corp.

- AWA Instruments

- NoiseMeters Inc.

- Bruitparif

- 3M Personal Safety Division

- Castle Group Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter Environmental Noise Regulations

- 4.2.2 Growth of Smart Cities and Urban Expansion

- 4.2.3 Expansion of Construction and Infrastructure Projects

- 4.2.4 Rising Public Awareness of Noise-Related Health Impacts

- 4.2.5 ESG-Linked Acoustic Compliance Mandates

- 4.2.6 Real-Time Noise Data for Dynamic Traffic Management

- 4.3 Market Restraints

- 4.3.1 High Capital and Maintenance Costs

- 4.3.2 Data-Privacy Hurdles in Continuous Monitoring

- 4.3.3 Interoperability Gaps in Multi-Vendor IoT Networks

- 4.3.4 Shortage of Acoustic-Data Analytics Talent

- 4.4 Industry Value-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Product Type

- 5.2.1 Fixed/Permanent Noise Monitoring Systems

- 5.2.2 Portable Noise Monitoring Systems

- 5.2.3 Wearable Personal Noise Dosimeters

- 5.2.4 Remote Noise Monitoring Kiosks

- 5.2.5 Other Product Types

- 5.3 By Technology

- 5.3.1 Real-Time Noise Monitoring

- 5.3.2 IoT-Enabled Smart Monitoring

- 5.3.3 Cloud-Based Noise Analytics Platforms

- 5.3.4 AI-Powered Predictive Acoustic Analytics

- 5.3.5 Other Technologies

- 5.4 By Application

- 5.4.1 Construction and Demolition Sites

- 5.4.2 Industrial Manufacturing Facilities

- 5.4.3 Transportation Hubs and Corridors

- 5.4.4 Urban / Community Noise Mapping

- 5.4.5 Mining and Energy Operations

- 5.4.6 Entertainment and Event Venues

- 5.4.7 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Hottinger Bruel & Kjaer GmbH

- 6.4.2 Acoem Group

- 6.4.3 Larson Davis (PCB Piezotronics)

- 6.4.4 RION Co., Ltd.

- 6.4.5 Svantek

- 6.4.6 Cirrus Research

- 6.4.7 NTi Audio

- 6.4.8 Casella (IDEAL Industries)

- 6.4.9 Pulsar Instruments Plc

- 6.4.10 G.R.A.S Sound and Vibration

- 6.4.11 Norsonic AS

- 6.4.12 Soft dB

- 6.4.13 SINUS Messtechnik

- 6.4.14 Extech Instruments (FLIR)

- 6.4.15 TES Electrical Electronic Corp.

- 6.4.16 AWA Instruments

- 6.4.17 NoiseMeters Inc.

- 6.4.18 Bruitparif

- 6.4.19 3M Personal Safety Division

- 6.4.20 Castle Group Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment