PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062206

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062206

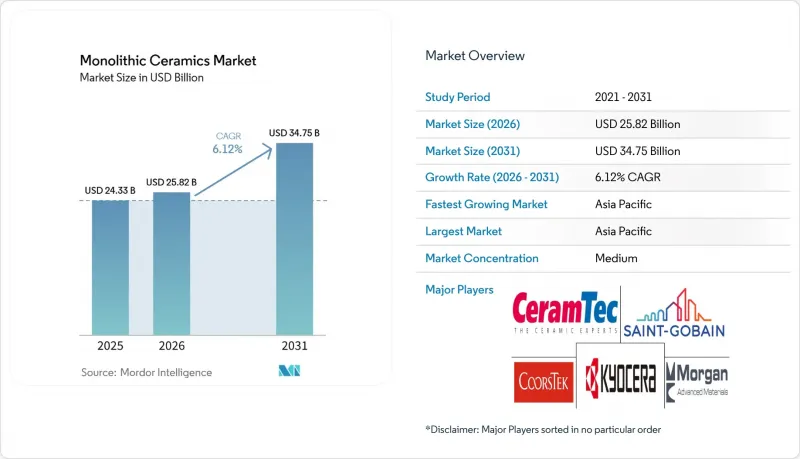

Monolithic Ceramics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the monolithic ceramics market size is expected to increase from USD 24.33 billion in 2025 to USD 25.82 billion in 2026 and reach USD 34.75 billion by 2031, growing at a CAGR of 6.12% over 2026-2031.

This report is Segmented by Material Type (Alumina, Zirconia, Silicon Nitride, and More), Structure (Transparent, Opaque, and Porous), End-User Industry (Electronics and Semiconductor, Automotive and Transportation, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Monolithic Ceramics Market Trends and Insights

EV Power-Train Thermal Management

Wide-bandgap silicon-carbide inverters now achieve over 99% efficiency, reducing heat loads by half compared to silicon IGBTs and increasing vehicle range by approximately 7% per charge. Mass production by ROHM-Schaeffler, STMicroelectronics, and Infineon on 200 mm wafers is lowering die costs and driving higher ceramic substrate volumes. Alumina and aluminum-nitride direct-bonded copper substrates are essential for dissipating these heat losses, while ISO 26262 compliance remains critical to mitigate delamination risks for inverter developers. The Monolithic ceramics market is well-aligned with the growth of 800-V e-mobility platforms. Back-end suppliers are already reporting nine-month lead times for AIN sheets, highlighting sustained pricing power.

Demand for Semiconductor Etch and CMP Fixtures

TSMC's USD 56 billion capital expenditure plan for 2026 and Intel's 18A ramp are expected to add thousands of alumina wafer carriers, yttria-coated chamber liners, and silicon-carbide susceptors per fab. CHIPS Act grants are projected to increase the U.S. share of advanced logic production to nearly 15% by the end of 2025, boosting local demand for semiconductor fixtures. NGK Insulators is tripling its HICERAM capacity to achieve JPY 20 billion in sales by 2030, emphasizing the integration of component manufacturing with semiconductor fabs. However, labor shortages are delaying tool installations, extending order backlogs for specialty carriers. The monolithic ceramics market remains closely tied to semiconductor capital expenditure cycles, ensuring volume visibility through 2028.

Intrinsic Brittleness and Design Limits

The fracture toughness of ceramics, ranging from 3-6 MPa√m, is significantly lower than that of metals, limiting their use in tensile or impact applications. For example, silicon-nitride EV motor bearings require surface roughness of ≤14 nm, increasing machining costs by four times compared to steel. Over-dimensioning to handle stress adds weight, while additive manufacturing introduces anisotropic flaws despite offering geometric flexibility. Standards such as ASTM C1161 and C1239 provide guidelines for flexural and Weibull testing, but no unified certification pathway exists for safety-critical additive-manufactured parts. These challenges constrain the broader adoption of ceramics, narrowing the addressable market until design standards evolve.

Other drivers and restraints analyzed in the detailed report include:

- Medical and Dental Implant Adoption Boom

- Green-Hydrogen Solid-Oxide Electrolyzer Stacks

- Carbon-Neutral Furnace Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Alumina held 47.12% of revenue dominance in 2025, but silicon carbide is anticipated to achieve a 6.58% CAGR through 2031, marking the fastest growth among materials. This is attributed to the shift towards wide-bandgap devices in EV inverters and renewable energy converters. Alumina's affordability ensures its continued use in CMP rings and implant abutments, while zirconia's transformation toughening enhances its application in solid-oxide electrolyzer electrolytes. Infineon's transition to 200 mm silicon carbide wafers has reduced epitaxy costs by 30%, supporting efforts to achieve price parity.

The monolithic ceramics market size for silicon carbide substrates is expected to grow significantly once ST-Sanan's 480,000-wafer production line reaches full capacity in 2028. Alumina, however, continues to dominate the monolithic ceramics market for fixtures. Silicon nitride and niche oxides, though smaller in scale, are strategically important for applications such as bearings and armor. Kyocera's BIOCERAM AZUL hybrid blend, with a flexural strength of 1,400 MPa, highlights incremental material innovations beyond the primary materials.

Geography Analysis

Asia-Pacific captured 44.22% of revenue in 2025 and is projected to grow at a 6.88% CAGR through 2031, driven by China's advanced ceramics production. Industrial clusters in Zibo and Foshan have a combined turnover exceeding CNY 100 billion, while Japanese manufacturers are investing JPY 55 billion in capacity and R&D between 2024 and 2026. ASEAN assembly hubs are also emerging as labor costs rise along China's coastal regions.

North America benefits from CHIPS Act incentives. Defense-driven demand for space ceramics is also contributing to growth. NGK's USD 58 million Arizona plant, set to become operational in 2027, will localize wafer-carrier supply. Canada and Mexico remain niche players, focusing on oil-field sensors and traditional tiles, respectively.

Europe interlinks ceramics with hydrogen goals. Topsoe's Danish electrolyzer plant, supported by EUR 94 million in funding, positions Scandinavia as a leader in green hydrogen. Germany's machinery sector and the U.K.'s Morgan Advanced Materials are key suppliers of aerospace composites. However, rising CBAM costs are prompting kiln electrification across southern Europe. Sanctions on Russia's advanced powder exports are redirecting demand within the CIS to domestic mills.

- 3M

- CeramTec GmbH

- CoorsTek Inc.

- Elan Technology

- H.C. Starck Tungsten GmbH

- Hitachi Chemical Co., Ltd.

- Kyocera Corporation

- Materion Corporation

- Morgan Advanced Materials

- Murata Manufacturing Co., Ltd.

- NGK INSULATORS, LTD.

- Rauschert Heinersdorf-Pressig GmbH

- Saint-Gobain

- SGL Carbon

- Sumitomo Electric Industries, Ltd.

- TOSOH CERAMICS CO., LTD.

- Vesuvius

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV power-train thermal management

- 4.2.2 Demand for semiconductor etch and CMP fixtures

- 4.2.3 Medical and dental implant adoption boom

- 4.2.4 Green-hydrogen solid-oxide electrolyzer stacks

- 4.2.5 Space economy (re-usable launchers, hypersonics)

- 4.3 Market Restraints

- 4.3.1 Intrinsic brittleness and design limits

- 4.3.2 Dopant-grade alumina and yttria supply squeeze

- 4.3.3 Carbon-neutral furnace regulations

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Alumina

- 5.1.2 Zirconia

- 5.1.3 Silicon Nitride

- 5.1.4 Silicon Carbide

- 5.1.5 Other Material Types (Magnesia, Mullite, Boron Carbide, etc.)

- 5.2 By Structure

- 5.2.1 Transparent

- 5.2.2 Opaque

- 5.2.3 Porous

- 5.3 By End-user Industry

- 5.3.1 Electronics and Semiconductor

- 5.3.2 Automotive and Transportation

- 5.3.3 Medical and Dental

- 5.3.4 Energy and Power

- 5.3.5 Other End-user Industries (Industrial Equipment, Chemical, Metallurgy, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 CeramTec GmbH

- 6.4.3 CoorsTek Inc.

- 6.4.4 Elan Technology

- 6.4.5 H.C. Starck Tungsten GmbH

- 6.4.6 Hitachi Chemical Co., Ltd.

- 6.4.7 Kyocera Corporation

- 6.4.8 Materion Corporation

- 6.4.9 Morgan Advanced Materials

- 6.4.10 Murata Manufacturing Co., Ltd.

- 6.4.11 NGK INSULATORS, LTD.

- 6.4.12 Rauschert Heinersdorf-Pressig GmbH

- 6.4.13 Saint-Gobain

- 6.4.14 SGL Carbon

- 6.4.15 Sumitomo Electric Industries, Ltd.

- 6.4.16 TOSOH CERAMICS CO., LTD.

- 6.4.17 Vesuvius

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment