PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062214

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062214

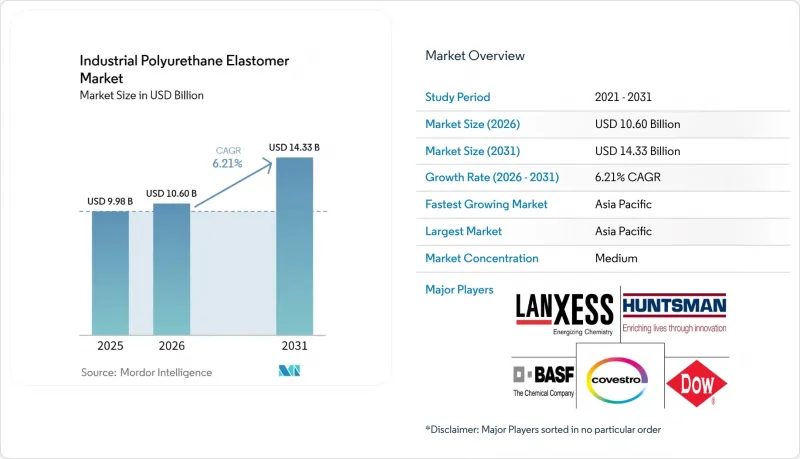

Industrial Polyurethane Elastomer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the industrial polyurethane elastomer market size was valued at USD 9.98 billion in 2025 and is estimated to grow from USD 10.60 billion in 2026 to reach USD 14.33 billion by 2031, at a CAGR of 6.21% during the forecast period (2026-2031).

This report is Segmented by Type (Thermoset PU Elastomers and Thermoplastic PU Elastomers), Processing Technology (Casting, and More), Application (Wheels and Rollers, Belts and Couplings, and More), End-User Industry (Automotive and Transportation, Oil and Gas, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Industrial Polyurethane Elastomer Market Trends and Insights

Expansion of Oil and Gas Exploration Equipment Using Polyurethane Parts

Polyurethane seals, pipeline pigs, and cable protectors exhibit excellent resistance to hydrocarbon immersion and temperatures below -40 °C, replacing nitrile and fluoroelastomers in subsea projects. Cast elastomers with Shore A 70-95 hardness ratings extend the service life of abrasive slurry pumps by up to 300%, reducing downtime for offshore operators.

Light-Weighting via Metal-PU Hybrids in Heavy Machinery

Bonding polyurethane sleeves to aluminum or steel cores reduces unsprung mass while maintaining the required stiffness for suspension bushings and cab mounts. BASF's Cellasto components achieved a 2.4% improvement in NVH (noise, vibration, and harshness) performance during a 2024 test program, leading to a EUR 100 million investment in a new Cellasto plant in India, scheduled to begin operations in 2026.

EU REACH Restrictions on Di-Isocyanates

Under EU REACH regulations effective August 2023, all European workers handling MDI or TDI must complete certified training, increasing compliance costs and encouraging OEMs to shift toward TPU, where injection molding can replace hand-cast CPU parts.

Other drivers and restraints analyzed in the detailed report include:

- Industrial Automation Needs High-Load Vibration Damping

- 3D-Printed PU Elastomer Tooling for Rapid Industrial Prototyping

- Advanced TPEs (PEBA, TPU Alloys) as Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thermoplastic polyurethane (TPU) elastomers accounted for 56.67% of the industrial polyurethane elastomer market share in 2025 and are projected to grow at a 6.89% CAGR through 2031. This segment leads in applications such as low-volume, heavy-duty screens, large rollers, and bespoke seals requiring tolerances exceeding +-5 mm. Cast processing enables shore hardness customization from 40A to 75D and facilitates the integration of fiber or microsphere fillers without shear-heating challenges. The growth of thermoplastic TPU is supported by recyclability mandates; Dow's SPECFLEX CIR line, launched in 2025, incorporates up to 65% recycled TPU while maintaining tensile strength benchmarks.

Thermoplastic TPU benefits from injection molding efficiency and compliance with circular economy requirements, particularly in automotive trim and electronics housings. However, cast polyurethane (CPU) retains an advantage in applications requiring extreme abrasion resistance, oversized parts, and complex chemistries that demand on-site processing flexibility. The ISO 7425-1:2021 standardization of hardness and compression-set tests enhances cross-supplier comparability and mitigates risks in large-asset procurement for industries such as mining and offshore platforms.

Injection molding held a 39.66% market share in 2025 due to its ability to produce precise geometries with minimal finishing. A 2024 study demonstrated that increasing barrel temperatures from 190 °C to 210 °C improved tensile strength by 12%, underscoring the importance of process parameters in optimizing TPU performance. Casting remains essential for manufacturing parts exceeding typical press capacities and for rapid field repairs. Other processing technologies, including compression and blow molding, are expected to grow at a 6.90% CAGR through 2031, driven by advancements in multi-component molding that combine soft-touch skins with structural cores in a single process.

Continuous extrusion is widely used for belts and tubing, where market growth is linked to improved material homogeneity and uninterrupted production. Additionally, digital process controls and closed-loop metering are lowering barriers for small fabricators to adopt hybrid platforms, redistributing market share toward agile regional processors.

Geography Analysis

Asia-Pacific dominated with 46.67% revenue share in 2025 and is forecast to have the fastest 6.98% CAGR to 2031. Capacity expansions in China, such as Covestro's Phase 1 Zhuhai TPU plant with a 30 kt/y capacity launched in 2026, are enabling local supply for industries including footwear, consumer electronics, and automotive. India's increasing polyol consumption aligns with new Cellasto capacity expected to come online in 2026, strengthening vertical integration in South Asia. Japan and South Korea focus on supplying advanced electronics-grade TPU, while ASEAN nations capture demand for footwear and appliance assemblies relocating from coastal China.

North America maintains a strong market position, supported by automotive, oil and gas, and warehouse automation sectors. Dow's 2025 expansion of propylene glycol production in Thailand secures upstream feedstock, complementing Huntsman's planned increase in European systems capacity by 2026. Mexico's near-shoring trend supports cast polyurethane NVH components for U.S. vehicle assembly lines.

In Europe, stringent REACH regulations on di-isocyanates are driving a shift toward TPU injection molding and pre-polymer systems with lower free-monomer content. Germany, France, and Italy anchor demand for advanced damping mounts and railway components, while Nordic countries emphasize bio-based polyols and halogen-free flame retardants for wind energy and cold-climate applications. Selected South American and Middle-Eastern markets utilize polyurethane in mining and petrochemical infrastructure, though growth is moderated by commodity cycle volatility.

- Arlanxeo

- BASF

- Blickle Rader+Rollen

- COIM Group

- Covestro AG

- Dow

- Era Polymers Pty Ltd

- Herikon BV

- Huntsman International LLC

- James Walker

- LANXESS

- Lubrizol

- MCPU Polymer Engineering LLC

- Mitsui Chemicals India Pvt. Ltd.

- Parker Hannifin Corp

- Reckon Rubber Industries

- Tosoh Corporation

- Trelleborg

- Wanhua

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of oil and gas exploration equipment using Polyurethane parts

- 4.2.2 Light-weighting via metal-PU hybrids in heavy machinery

- 4.2.3 Industrial automation needs high-load vibration damping

- 4.2.4 3-D printed PU elastomer tooling for rapid industrial prototyping

- 4.2.5 On-site spray-elastomer linings for asset-life extension

- 4.3 Market Restraints

- 4.3.1 EU REACH restrictions on di-isocyanates

- 4.3.2 Advanced TPEs (PEBA, TPU alloys) as substitutes

- 4.3.3 Insurance-driven flammability concerns in underground mining

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Thermoplastic PU Elastomers (TPU)

- 5.1.2 Thermoset PU Elastomers (CPU)

- 5.2 By Processing Technology

- 5.2.1 Injection Molding

- 5.2.2 Casting

- 5.2.3 Extrusion

- 5.2.4 Other Processing Technologies (Compression, Blow, etc.)

- 5.3 By Application

- 5.3.1 Wheels and Rollers

- 5.3.2 Belts and Couplings

- 5.3.3 Vibration and Shock-absorbing Components

- 5.3.4 Seals and Gaskets

- 5.3.5 Machine Components

- 5.3.6 Mining Screens and Liners

- 5.3.7 Other Applications

- 5.4 By End-user Industry

- 5.4.1 Automotive and Transportation

- 5.4.2 Oil and Gas

- 5.4.3 Mining and Quarrying

- 5.4.4 Industrial Machinery and Equipment

- 5.4.5 Material Handling

- 5.4.6 Construction

- 5.4.7 Electronics and Electrical

- 5.4.8 Other End-user Industries (Textile, Paper, Food, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Arlanxeo

- 6.4.2 BASF

- 6.4.3 Blickle Rader+Rollen

- 6.4.4 COIM Group

- 6.4.5 Covestro AG

- 6.4.6 Dow

- 6.4.7 Era Polymers Pty Ltd

- 6.4.8 Herikon BV

- 6.4.9 Huntsman International LLC

- 6.4.10 James Walker

- 6.4.11 LANXESS

- 6.4.12 Lubrizol

- 6.4.13 MCPU Polymer Engineering LLC

- 6.4.14 Mitsui Chemicals India Pvt. Ltd.

- 6.4.15 Parker Hannifin Corp

- 6.4.16 Reckon Rubber Industries

- 6.4.17 Tosoh Corporation

- 6.4.18 Trelleborg

- 6.4.19 Wanhua

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment