PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062219

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062219

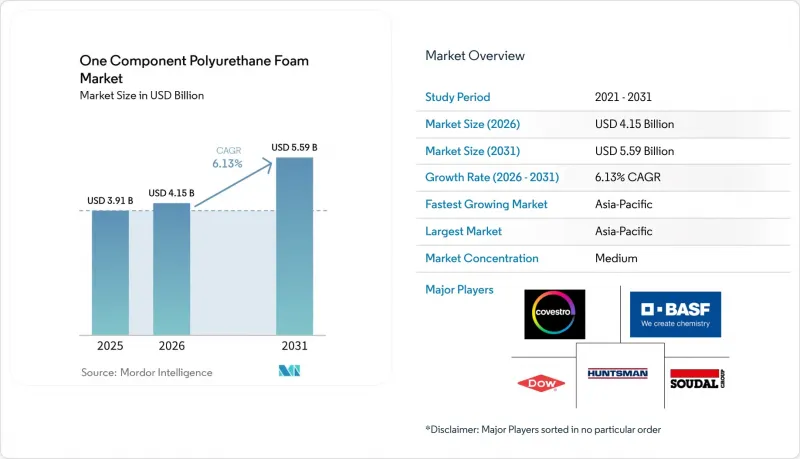

One Component Polyurethane Foam - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the one component polyurethane foam market size was valued at USD 3.91 billion in 2025 and is estimated to grow from USD 4.15 billion in 2026 to reach USD 5.59 billion by 2031, at a CAGR of 6.13% during the forecast period (2026-2031).

This report is Segmented by Type (Traditional, Fire-Resistant, and More), Application (Window and Door-Frame Sealing, HVAC and Pipeline Insulation, and More), End-User Industry (Residential Construction, Commercial Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global One Component Polyurethane Foam Market Trends and Insights

Expansion of Fire-Rated and Moisture-Resistant Foam Technologies

Fire-resistant one component polyurethane foam will grow 6.68% per year to 2031, outpacing legacy grades as building authorities tighten flame-spread and smoke-toxicity thresholds. Updated UK Part L 2026 rules set wall U-values at 0.18 W/m2K, encouraging contractors to specify gap fillers that preserve compartmentation without compromising thermal targets. Closed-cell, moisture-resistant variants are favored in coastal regions and cold-storage hubs for below-grade or high-humidity service, where water-absorption limits below 2% by volume protect durability. BASF's Autofroth system, introduced in February 2026, reduces smoke toxicity 30% versus brominated baselines while trimming embodied carbon by up to 20%. A global trend toward intumescent, hybrid sealant-foam systems aligns passive fire protection with acoustic and energy-performance objectives.

Increased Use in Window and Door-Frame Installations

Window and door-frame sealing represented 38.89% of 2025 revenue as triple-glazed units mainstreamed across renovation programs. Low-expansion foams that exert under 5 psi during cure prevent frame distortion and have become mandatory in many manufacturers' warranties. SikaWall-3000 Rapid Bond, launched April 2025, halves curing time to under four hours, cutting labor costs 40% on high-rise facades. Revised EU Energy Performance of Buildings Directive requirements for whole-life carbon disclosure push architects toward bio-based, low-VOC foams, which now command a modest premium amid growing acceptance. Utility rebates in California and Ontario that cover up to 50% of air-sealing materials, including online purchases, amplify do-it-yourself uptake in North America.

Strict Limits on Isocyanate Emissions and Worker Safety

OSHA's 20 ppb eight-hour MDI limit and EU REACH's mandatory diisocyanate training regime elevate compliance costs across small-scale contracting. The UK Health and Safety Executive's March 2025 guidelines require local exhaust ventilation and biological monitoring above 50% of exposure limits, raising project overhead for residential remodelers. Australia's SafeWork model Code of Practice presumes hazard unless air monitoring proves otherwise, accelerating the shift to low-free-isocyanate formulas that sacrifice 10-15% compressive strength but avoid costly ventilation retrofits. Smaller contractors increasingly switch to silicone or acrylic latex where structural loads are minimal.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Pressure on Thermal-Insulation Compliance

- Surge in Prefabricated Modular Construction Requiring Pre-Cured Foams

- Availability of Alternative Sealants and Insulation Methods

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traditional one component polyurethane foam accounted for 43.35% of one component polyurethane foam market share in 2025, anchored in general-purpose gap filling, where cost sensitivity dominates. Fire-rated products are set to grow 6.68% annually during the forecast period (2026-2031), propelled by ASTM E84 Class A and NFPA 286 adoption in mixed-use towers. The one-component polyurethane foam market size for fire-rated variants is projected to reach a greater value in 2031, underscoring a regulatory pivot toward safety-critical seals. Low-expansion lines continue to displace high-expansion foams in premium fenestration installations as manufacturers link warranty coverage to frame-pressure limits. Niche acoustic and phase-change formulations are gaining traction in electric-vehicle NVH packages following Nissan's demonstration of ride comfort improvement in 2025.

Second-generation products layer sustainability onto safety. BASF's Autofroth reduces smoke toxicity 30% and carbon footprint up to 20%, positioning the company for specification in health-care facilities with stringent indoor-air protocols. Price differentials between traditional and fire-resistant cans narrowed to under USD 2 in 2026, supporting mainstream adoption even in cost-focused residential upgrades. Mature high-expansion lines remain favored in attic and crawl-space retrofits where speed outweighs precision, yet volumetric share is expected to erode as labor-sensitive contractors embrace quick-curing, low-pressure alternatives.

Geography Analysis

Asia-Pacific dominated the one component polyurethane foam market with a 47.74% revenue share in 2025 and is projected to grow at 6.92% CAGR through 2031. China's polyurethane output in 2024 and Wanhua Chemical's 1.8 million-ton MDI capacity expansion in January 2025 alleviated prior feedstock tightness. India's annual polyurethane volume growth and infrastructure push signal continued demand, while Indonesia's palm-oil cold-storage boom sustains double-digit foam usage. Japan's prefab housing share reached 18% in 2024, integrating factory-applied foams to hit airtightness targets.

North America's polyurethane sector faces high-GWP propellant bans effective 2025 under the EPA rule set. Yet data-center construction climbed 35% in 2025, driving industrial-grade foam uptake. Canada's code updates raise Climate Zone 6 insulation requirements 20%, boosting high-R foam sales in Ontario and Quebec. Mexico's near-shoring wave adds cleanroom and humidity-controlled factories that specify gap-free insulation around HVAC ductwork.

Europe confronts the Energy Performance of Buildings Directive redo, mandating zero-emission new buildings by 2030 and whole-life carbon reporting for structures over 1,000 m2 starting 2028. Germany's GEG 2024, the UK's Part L 2026, and France's RE2020 toughen thermal transmittance limits, underpinning demand for certified, fire-rated foams. Covestro's Dormagen TDI force majeure in July 2025 cut 300,000 tons per annum and tightened European supply, nudging contractors toward premixed, single-can formats that curb site-level isocyanate exposure.

- Akfix

- Arkema

- BASF

- Covestro AG

- Dow

- fischer Group of Companies

- Huntsman International LLC

- ICP Building Solutions Group

- QUILOSA - Selena Iberia S.L.U.

- SEKISUI CHEMICAL CO., LTD.

- Shanghai Haohai Chemical Co., Ltd.

- Sika AG

- Soudal Group

- Trelleborg AB

- Wanhua

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of fire-rated and moisture-resistant foam technologies

- 4.2.2 Increased use in window and door-frame installations

- 4.2.3 Regulatory pressure on thermal-insulation compliance

- 4.2.4 Surge in prefabricated modular construction requiring pre-cured foams

- 4.2.5 E-commerce DIY channels accelerating single-can foam adoption

- 4.3 Market Restraints

- 4.3.1 Strict limits on isocyanate emissions and worker safety

- 4.3.2 Availability of alternative sealants and insulation methods

- 4.3.3 Upcoming bans on high-GWP propellants in Europe and North America

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Traditional One Component Polyurethane Foam

- 5.1.2 Fire-Resistant One Component Polyurethane Foam

- 5.1.3 Low-Expansion One Component Polyurethane Foam

- 5.1.4 High-Expansion One Component Polyurethane Foam

- 5.1.5 Other Types (Specialized Foams)

- 5.2 By Application

- 5.2.1 Window and Door-Frame Sealing

- 5.2.2 HVAC and Pipeline Insulation

- 5.2.3 Gap Filling and Crack Sealing

- 5.2.4 Roofing and Wall Cavities

- 5.2.5 Other Applications (Construction and Industrial, etc.)

- 5.3 By End-user Industry

- 5.3.1 Residential Construction

- 5.3.2 Commercial Construction

- 5.3.3 Industrial and Infrastructure

- 5.3.4 Automotive and Transportation

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Akfix

- 6.4.2 Arkema

- 6.4.3 BASF

- 6.4.4 Covestro AG

- 6.4.5 Dow

- 6.4.6 fischer Group of Companies

- 6.4.7 Huntsman International LLC

- 6.4.8 ICP Building Solutions Group

- 6.4.9 QUILOSA - Selena Iberia S.L.U.

- 6.4.10 SEKISUI CHEMICAL CO., LTD.

- 6.4.11 Shanghai Haohai Chemical Co., Ltd.

- 6.4.12 Sika AG

- 6.4.13 Soudal Group

- 6.4.14 Trelleborg AB

- 6.4.15 Wanhua

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment