PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062225

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062225

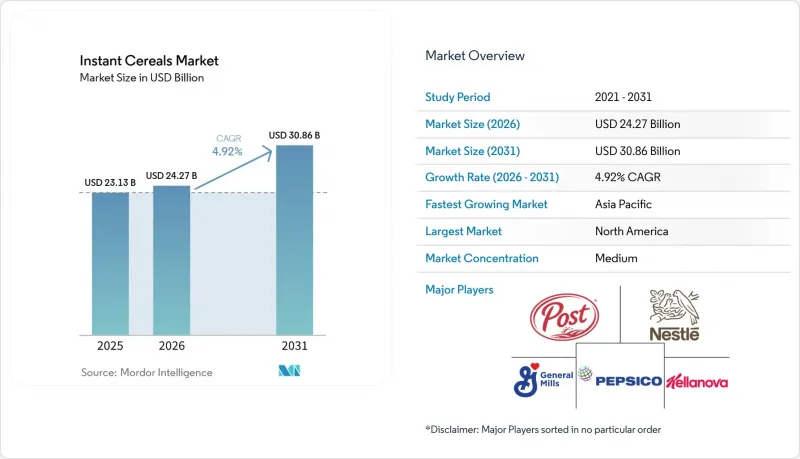

Instant Cereals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the instant cereals market size is expected to increase from USD 23.13 billion in 2025 to USD 24.27 billion in 2026 and reach USD 30.86 billion by 2031, growing at a CAGR of 4.92% over 2026-2031.

This report is Segmented by Product Type (Oats, Wheat, Rice, Corn, Others), Flavor (Flavored, Unflavored), Category (Conventional, Organic), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online Retail Stores, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Instant Cereals Market Trends and Insights

Rising Health Focus on Whole-Grain and High-Protein Formulations

Consumer demand for functional breakfast options has catalyzed a fundamental reformulation trend across the instant cereals industry, with manufacturers increasingly positioning products as vehicles for essential nutrients rather than mere convenience foods. The USDA's emphasis on making half of grain consumption whole grains has created regulatory tailwinds, while research demonstrating that breakfast cereal consumption correlates with higher vitamin and mineral intake provides scientific validation for health claims. The protein fortification movement has gained particular traction among younger demographics. This health positioning strategy extends beyond protein to encompass fiber enhancement, with manufacturers leveraging B-glucan extraction technologies to maximize the cholesterol-lowering benefits that provide FDA-approved health claims for oat-based products. The convergence of regulatory support, scientific validation, and consumer demand creates a self-reinforcing cycle that positions health-focused formulations as the primary growth engine for premium market segments.

Demand for Convenience and On-the-Go Breakfasts

In Asia-Pacific megacities, where many workers face commutes exceeding 90 minutes, urbanization is shrinking the time available for breakfast preparation. This has led to a surge in the popularity of single-serve instant porridge formats, which can be rehydrated in under three minutes. This quick rehydration time is backed by peer-reviewed studies, highlighting an optimized instant cereal drink's rehydration at just 2.73 seconds. Furthermore, the U.S. Department of Agriculture's move to allow SNAP online purchases at over 390 retailer chains by 2025 has made instant cereals more accessible to lower-income families. This shift has effectively eliminated a previous distribution hurdle, which had limited premium instant oatmeal sales to specialty brick-and-mortar stores. Meanwhile, PepsiCo's initiatives, like the Quaker Bowl of Growth in India and Quaker Qrece in Guatemala and Mexico, showcase how global giants are customizing portion sizes and flavors to resonate with local breakfast habits. This approach not only taps into established distribution channels but also reduces the risks associated with reformulating products.

Sugar-Content Scrutiny and High Fat, Sugar, and Salt (HFSS) Regulations

Regulatory pressure surrounding sugar content has intensified globally, with the United Kingdom's implementation of HFSS advertising restrictions effective October 2025 serving as a bellwether for broader regulatory trends that could reshape product formulations and marketing strategies across the instant cereals industry. The United Kingdom regulations impose a 9 pm watershed for television advertising and complete online advertising bans for products exceeding specific sugar, fat, and salt thresholds, directly impacting traditional breakfast cereal marketing approaches. The regulatory environment has created a bifurcated market where compliant products gain competitive advantages in regulated channels while traditional formulations face increasing distribution constraints. The regulatory trend extends beyond sugar to encompass broader nutritional profiling models that evaluate products holistically, creating complexity for manufacturers who must balance taste preferences, regulatory compliance, and cost considerations while maintaining brand positioning and consumer loyalty in an increasingly regulated environment.

Other drivers and restraints analyzed in the detailed report include:

- Introduction of New Flavors, Plant-Based Ingredients, and Regional Customizations

- Increasing availability for diverse dietary preferences

- Competition from Alternative Breakfast Options

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, oats held a 48.31% share of the instant cereals market, driven by their association with heart health and whole-grain benefits. Bob's Red Mill reported a 6.4% sales increase, reaching USD 132.86 million by December 28, 2025, fueled by its Overnight Protein Oats launch with 10 grams of protein per serving. Quaker Oats introduced Protein Standard oats in spring 2025, targeting fitness enthusiasts seeking muscle recovery benefits. Oat prices dropped to USD 3.12 per bushel in January 2026 from USD 3.92 in 2023-2024, easing reformulation costs for manufacturers. Finland's annual oatmeal consumption of 30-34 kilograms per person highlights oats' cultural significance in Nordic breakfasts. However, HFSS regulations penalizing sugary flavored oatmeal are pushing producers toward unflavored or naturally sweetened options.

Corn-based instant cereals are projected to grow at a 5.26% CAGR from 2026 to 2031, the fastest among all types, due to their gluten-free and allergen-friendly appeal. Research shows adding 20% quinoa at 650 rpm extrusion improves protein and fiber while maintaining texture, supporting corn-based functional cereals. Corn fits well with traditional dishes like Mexico's atole and Southeast Asia's congee, easily adapted to instant formats. In January 2026, corn's Market Year Average price was USD 4.10 per bushel, remaining cost-competitive against wheat (USD 5.01) and rice (USD 13.60 per hundredweight). Improved supply chains, exports, logistics, and storage have boosted corn availability, reducing risks seen in 2021-2022. Flavor innovations, such as sweet-savory blends and global cuisine influences, are helping corn-based cereals attract younger consumers seeking variety in breakfast options.

In 2025, flavored instant cereals held a 70.92% market share, driven by consumer demand for variety and the convenience of pre-sweetened options. Post Consumer Brands launched OREO PUFFS in January 2025, leveraging its confectionery brand to attract younger consumers. Similarly, Kellogg's introduced High Protein Bites in April 2025, offering 13-14 grams of protein to compete with protein bars. However, flavored cereals face challenges like the USDA's 6-gram added sugar limit for Child and Adult Care Food Program cereals, forcing reformulations with non-nutritive sweeteners or smaller portions. Additionally, HFSS advertising restrictions in the UK and Scotland limit promotions of high-sugar cereals during peak hours and in prominent retail spaces.

Unflavored instant cereals are growing at a 6.08% CAGR from 2026 to 2031, the fastest among flavor types, as health-conscious consumers seek customization and sugar control. Purely Elizabeth's sales grew 40% year-over-year to USD 12.85 million by December 28, 2025, showing demand for organic, lightly sweetened oatmeal that consumers enhance with fresh ingredients. Unflavored cereals align with clean-label trends and meet USDA and HFSS standards without reformulation, ensuring access to institutional buyers. A 2026 study on jali and garut flour-based cereals achieved a high desirability score of 0.996, proving unflavored options can succeed with good texture and mouthfeel. The segment also benefits from savory cereals with vegetables and herbs, appealing to Asian and European tastes. Premium pricing in organic and specialty markets offsets lower sales volumes with higher margins.

Geography Analysis

North America maintains a dominant market position with 35.88% share in 2025. This leadership stems from established consumer breakfast habits, comprehensive cold-chain distribution infrastructure, and strong brand loyalty that creates entry barriers for international competitors. The region's mature retail networks, marketing capabilities, and supportive regulatory frameworks enable health claims and product innovation. However, North America faces growth limitations from market saturation, evolving demographic preferences, and increasing competition from alternative breakfast options.

Asia-Pacific demonstrates the highest growth rate at 6.89% CAGR through 2031. This growth results from urbanization, increasing disposable incomes, and a shift toward Western breakfast habits, expanding beyond traditional rice-based morning meals. China and India's large populations, improving retail infrastructure, and growing health consciousness among urban consumers support market expansion. The region's diverse cultural preferences create opportunities for localized products, including rice-based cereals that combine traditional preferences with modern convenience.

Europe maintains a stable market position with established organic and health-focused consumer segments driving premium product demand. The region adapts to HFSS regulatory requirements that influence marketing strategies and product formulations. The Middle East and Africa, and South America represent emerging markets with growth potential driven by urbanization, infrastructure development, and increasing Western breakfast adoption. These regions offer market expansion opportunities but require consideration of local preferences, price sensitivity, and distribution challenges. Success depends on manufacturers' ability to invest in market development and consumer education.

- Kellogg Company

- General Mills Inc.

- PepsiCo Inc.

- Nestle S.A.

- Post Holdings Inc.

- Bob's Red Mill Natural Foods

- Nature's Path Foods

- Weetabix Ltd.

- B&G Foods

- Marico Ltd.

- Bagrry's India Ltd.

- TreeHouse Foods Inc.

- Hain Celestial

- Freedom Foods Group Ltd.

- Hero Group

- Danone S.A.

- Abbott Nutrition

- Catalina Crunch Co.

- Magic Spoon Inc.

- MOM Brands

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for convenience and on-the-go breakfasts

- 4.2.2 Rising health focus on whole-grain and high-protein formulations

- 4.2.3 Introduction of new flavors, plant-based ingredients, and regional customizations

- 4.2.4 Increasing availability for diverse dietary preferences

- 4.2.5 Advances in food processing technology

- 4.2.6 Influence of urbanization and modern lifestyles

- 4.3 Market Restraints

- 4.3.1 Sugar-content scrutiny and High Fat, Sugar, and Salt (HFSS) regulations

- 4.3.2 Competition from alternative options

- 4.3.3 High raw material costs

- 4.3.4 Quality perceptions regarding high processing

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Supplier Power

- 4.7.2 Buyer Power

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Oats

- 5.1.2 Wheat

- 5.1.3 Rice

- 5.1.4 Corn

- 5.1.5 Others

- 5.2 By Flavor

- 5.2.1 Flavored

- 5.2.2 Unflavored

- 5.3 By Category

- 5.3.1 Conventional

- 5.3.2 Organic

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Specialty Stores

- 5.4.3 Online Retail Stores

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share for key companies, Products, and Recent Developments)

- 6.4.1 Kellogg Company

- 6.4.2 General Mills Inc.

- 6.4.3 PepsiCo Inc.

- 6.4.4 Nestle S.A.

- 6.4.5 Post Holdings Inc.

- 6.4.6 Bob's Red Mill Natural Foods

- 6.4.7 Nature's Path Foods

- 6.4.8 Weetabix Ltd.

- 6.4.9 B&G Foods

- 6.4.10 Marico Ltd.

- 6.4.11 Bagrry's India Ltd.

- 6.4.12 TreeHouse Foods Inc.

- 6.4.13 Hain Celestial

- 6.4.14 Freedom Foods Group Ltd.

- 6.4.15 Hero Group

- 6.4.16 Danone S.A.

- 6.4.17 Abbott Nutrition

- 6.4.18 Catalina Crunch Co.

- 6.4.19 Magic Spoon Inc.

- 6.4.20 MOM Brands

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK