PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062230

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062230

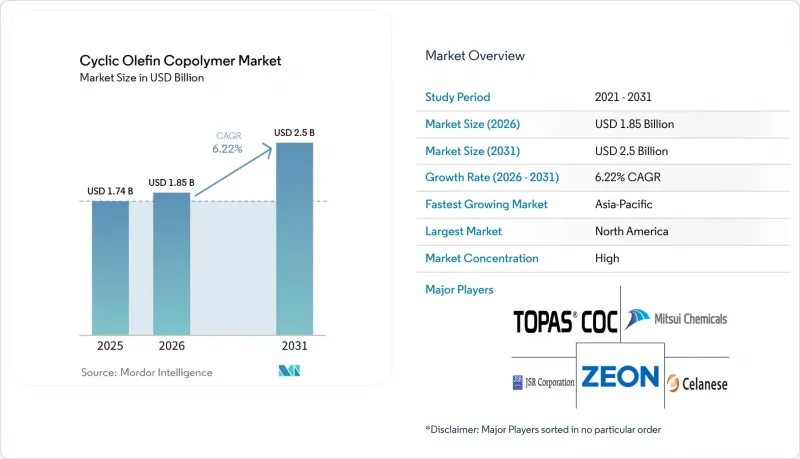

Cyclic Olefin Copolymer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the cyclic olefin copolymer market size is expected to increase from USD 1.74 billion in 2025 to USD 1.85 billion in 2026 and reach USD 2.5 billion by 2031, growing at a CAGR of 6.22% over 2026-2031.

This report is Segmented by Type (Amorphous COC and Semi-Crystalline COC), Grade (Injection-Molding Grade, Blow-Molding Grade, Film and Sheet Grade, and More), End-User Industry (Healthcare and Medical, Electronics and Optoelectronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Cyclic Olefin Copolymer Market Trends and Insights

Rising Demand for Pharmaceutical Blister Packs, Pre-filled Syringes and Vials

Glass surfaces promote protein adsorption that degrades biologics, whereas COC's 26 mN/m surface energy curbs binding and maintains drug potency. ZEONEX medical-grade syringes retain impact strength at -194°C, enabling mRNA and cell-therapy distribution in ultra-cold chains. Monomaterial COC blisters reach moisture-vapor transmission rates below 0.1 g/m2/day, rivaling foil laminates and aligning with EU recyclability rules. Zeon's vertically integrated C5 chain secures residual-unsaturation levels under 0.02 wt%, a prerequisite for FDA Drug Master File acceptance. Yet Daicel shifted its German start-up to Q1 2027 after 2026 order volumes fell 4%, exposing reliance on a few pharmaceutical accounts.

Adoption in Microfluidics and Point-of-Care Lab-on-Chip Devices

Polydimethylsiloxane absorbs hydrophobic reagents, whereas cyclic olefin copolymer market solutions show negligible small-molecule partitioning, sharpening assay accuracy. Fraunhofer trials achieved 10,000 pneumatic-valve cycles in elastomeric COC chips, extending device lifetimes versus rigid thermoplastics. COVID-19 fluorescence tests lowered autofluorescence noise to under 5% of signal when switching from polystyrene to COC substrates. Hybrid COC-PLGA microchannels are enabling wearable insulin pumps with integrated drug-delivery reservoirs. Divergent ISO 10993 test regimes between the EU and the USA create regulatory arbitrage that favors North American contract molders.

High Resin Cost Versus Polyolefin Commodity Plastics

Cyclic olefin copolymer market resin sells at 2.5-3.5 times linear low-density polyethylene because norbornene synthesis and metathesis polymerization require capital-heavy C5 crackers and multi-stage hydrogenation. Generic blister applications in emerging regions stay with polypropylene that meets 1-2 g/m2/day moisture targets at half the cost. Chinese suppliers undercut Japanese benchmarks by 15-20%, but pellet-drying lapses yield hydrolysis defects that rule them out of pharma and semiconductor supply chains. Cyclopentadiene feedstock prices spiked 18% in Q1 2025 after Asian crackers shut unexpectedly, squeezing converter margins locked into fixed drug-contract pricing. Customer reticence forced Daicel to delay its German plant commissioning, highlighting how price volatility suppresses long-term offtake deals.

Other drivers and restraints analyzed in the detailed report include:

- Growth of High-Resolution Display and LED Optical Films

- EU PPWR Push for Monomaterial Recyclable Pharma Blister Formats

- Limited Large-Scale Mechanical Recycling Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Amorphous COC controlled 58.27% cyclic olefin copolymer market share in 2025, owing to glass-like clarity and tight-tolerance injection molding for vials and microfluidics. These grades deliver glass-transition points of 101-154°C and modulus near 2,900 MPa, sustaining smartphone lenses where alignment tolerances stay within 5 µm. Semi-crystalline variants are pacing a 6.58% CAGR for the forecast period (2026-2031) as automotive head-up displays and ADAS (Advanced Driver Assistance Systems) cameras need higher heat-deflection ceilings above 120°C without haze growth.

Semi-crystalline resins, strengthened through novel copolymer chains, extend elongation from 4% to 245%, permitting foldable display backplanes that endure 10,000 flex cycles. ZEONEX 360R's ultralow birefringence supports augmented-reality optics because color shift remains under 5 nm retardation. Sumitomo's photocurable COC hybridizes thermoplastic processing with thermoset dimensional stability, responding to semiconductor lithography's need for solvent-resistant photoresists. Tight ISO 9001 controls cap refractive-index variance at +-0.001, a threshold demanded by phone-camera OEMs.

Geography Analysis

North America accounted for 31.16% of 2025 sales. U.S. drug-delivery firms value COC syringes that survive -194°C transport without cracks. Zeon's domestic depots shorten lead times to one week, a clear edge over ocean freight from Europe. Canadian microfluidic start-ups pivot from Polydimethylsiloxane (PDMS) to COC for low dye absorption, while Mexican lens molders adopt APEL for ADAS cameras that function at 120°C.

Asia-Pacific is the fastest-growing geography with a 7.02% CAGR to 2031. Zeon's JPY 70 billion (USD 470 million) Tokuyama East complex will lift Japanese output 30% to 54 kilotons/year by 2028, easing resin allocations for South Korean display fabs. Korean research that multiplies tensile elongation fivefold positions regional suppliers at the forefront of rollable OLED substrates. China added 10 kilotons/year of low-cost injection resin in 2024, yet still captures a very low share of the pharmaceutical business because pellets exceed moisture specs. India explores COC blister webs for high-humidity APIs but remains price sensitive.

Europe accelerates blister-format validation following the 2025 VerpackG fee hike. Still, Polyplastics deferred its Leuna start-up to 2027 amid weak early-stage PPWR spending. Nordic insulin-vial pilots showcase COC's less than 0.1 g/m2/day moisture rate, protecting 24-month shelf lives. South America and MEA lag because freight costs and import duties add 10-15% to already premium resin, restricting use to top-tier biologics.

- Asahi Kasei Corporation

- Avantor Inc.

- BOREALIS GMBH.

- Celanese Corporation

- Daikyo Seiko Ltd.

- ExxonMobil Corp.

- JSR Corporation

- Mitsui Chemicals, Inc.

- Polysciences

- RTP Company

- SABIC

- Sumitomo Chemical Co., Ltd.

- TOPAS Advanced Polymers / Polyplastics

- ZEON CORPORATION

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for pharmaceutical blister packs, pre-filled syringes and vials

- 4.2.2 Adoption in micro-fluidics and point-of-care lab-on-chip devices

- 4.2.3 Growth of high-resolution display and LED optical films

- 4.2.4 EU-PPWR push for monomaterial recyclable pharma blister based on COC

- 4.2.5 COC backplane substrates enabling ultra-thin foldable micro-LED panels

- 4.3 Market Restraints

- 4.3.1 High resin cost versus polyolefin commodity plastics

- 4.3.2 Limited large-scale mechanical recycling infrastructure

- 4.3.3 Supply-chain concentration with lesser global resin producers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Amorphous COC

- 5.1.2 Semi-crystalline COC

- 5.2 By Grade

- 5.2.1 Injection-Molding Grade

- 5.2.2 Blow-Molding Grade

- 5.2.3 Film and Sheet Grade

- 5.2.4 Medical and Pharmaceutical Grade

- 5.3 By End-user Industry

- 5.3.1 Healthcare and Medical

- 5.3.2 Electronics and Optoelectronics

- 5.3.3 Packaging

- 5.3.4 Automotive and Transportation

- 5.3.5 Other End-user Industries (Consumer Goods, and More)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Asahi Kasei Corporation

- 6.4.2 Avantor Inc.

- 6.4.3 BOREALIS GMBH.

- 6.4.4 Celanese Corporation

- 6.4.5 Daikyo Seiko Ltd.

- 6.4.6 ExxonMobil Corp.

- 6.4.7 JSR Corporation

- 6.4.8 Mitsui Chemicals, Inc.

- 6.4.9 Polysciences

- 6.4.10 RTP Company

- 6.4.11 SABIC

- 6.4.12 Sumitomo Chemical Co., Ltd.

- 6.4.13 TOPAS Advanced Polymers / Polyplastics

- 6.4.14 ZEON CORPORATION

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment