PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062231

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062231

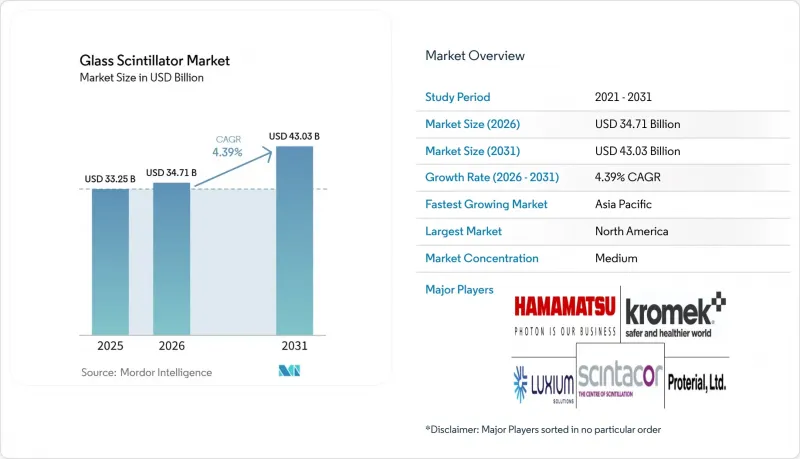

Glass Scintillator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the glass scintillator market size is expected to grow from USD 33.25 billion in 2025 to USD 34.71 billion in 2026 and is forecast to reach USD 43.03 billion by 2031 at 4.39% CAGR over 2026-2031.

This report is Segmented by Composition (Lithium-Based Glass Scintillators, Boron-Based Glass Scintillators, and More), Application (Medical Imaging, Nuclear Power Plants and Radiation Monitoring, and More), End-User Industry (Healthcare, Energy and Power, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Glass Scintillator Market Trends and Insights

Rising Demand in Radiation Detection and Nuclear Security

National programs to strengthen fixed and mobile radiation-monitoring networks are expanding, with the UK pre-qualifying wearable, handheld, and portal systems under its Radiological Nuclear Detection Framework in 2024. Lithium-glass assemblies utilize Li-6's 940-barn thermal-neutron cross-section, providing integrators with a compact dual-mode detector that replaces bulkier He-3 tubes. The June 2025 U.S. DHS backpack-detector survey highlighted emerging NaI(Li) configurations that combine neutron capture with≤ 8% FWHM gamma energy resolution at 662 keV. ANSI N42.53 compliance has become a critical purchasing criterion, narrowing awards to vendors with proven isotope-enrichment ties and hermetic-sealing expertise. As border crossings, seaports, and transit hubs require simultaneous neutron and gamma detection, glass scintillator market penetration is expected to grow where supply chains can deliver large-area Li-6 panels alongside low-background crystals.

Expanding Adoption in Medical Imaging (PET/CT)

Multi-modality gantries that integrate PET, SPECT, and CT in one suite are becoming the oncology standard, as demonstrated by FDA clearance of Mediso's AnyScan 3.0 in December 2025. While these systems rely on crystals for core gamma cameras, auxiliary detector banks designed for high-throughput, lower-resolution tasks can use glass arrays to reduce material costs and enable larger footprints. The expansion of oncology centers in China and India's public-private diagnostics initiatives is increasing unit volumes, driving interest in cerium-doped glass-ceramics with a 50 nGy/s detection limit suitable for low-dose CT workflows. Regulatory alignment with NEMA NU 2-2018 ensures stringent energy-resolution specifications. Pilot installations indicate that glass panels can handle attenuation correction and scout imaging without disrupting clinician workflows. These operational advantages position glass scintillators for broader adoption in provincial and midsize hospitals, where cost per scan is prioritized over sub-5 mm spatial resolution.

Lower Light Yield Compared to Crystal Scintillators

Commercial glass scintillators emit 2,000-3,500 photons/MeV, significantly lower than lanthanum bromide's 40,000 photons/MeV, resulting in energy-resolution limits of 13-18% FWHM at 662 keV. While Ce3+-doped lithium silicates have achieved 7,058 photons per thermal neutron in laboratory settings, these prototypes require scale-up and radiation-hardness validation before commercialization. The lower signal amplitude necessitates larger active areas or higher SiPM gains, both of which increase costs and noise. Vendors are exploring co-doping with manganese to enhance energy-transfer cascades and developing glass-ceramic nanocomposites that nucleate scintillating phases in situ. However, these innovations add manufacturing complexity and quality control requirements. Until production yields consistently exceed 10,000 photons/MeV, glass scintillators will remain less competitive in premium spectroscopy applications dominated by crystal scintillators.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Industrial Non-Destructive Testing (NDT)

- Surge in Homeland-Security Investments Post-2025

- High Costs and Process Complexity for Li-6/B-10 Glasses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-based glass scintillators accounted for 42.26% of 2025 revenue, with enriched Li-6 glass dominating neutron-sensitive applications such as backpack detectors and oil-well logging tools. These applications benefit from compact geometries and a 940-barn capture cross-section. Phosphate glass scintillators are expected to grow at a 5.11% CAGR through 2031, driven by cerium- and terbium-co-doped chemistries that enhance photon yields, making them suitable for dual-mode gamma-neutron applications.

Laboratory advancements in Ce3+-doped lithium glass have achieved neutron light yields 18% higher than GS20 and gamma suppression ratios near 0.23, approaching performance parity with crystal references. Boron-rich glasses remain a niche solution, particularly in scenarios where Li-6's reactivity poses challenges, such as sealed neutron tubes operating at pressures up to 15 atm. Emerging hybrid glasses incorporating POPOP or anthracene have reduced decay times to under 5 ns, a feature highly valued for kilohertz radioscopic inspections. As commercial scaling progresses, the market for phosphate and hybrid glass scintillators is expected to grow faster than lithium-based scintillators. However, lithium-based scintillators are projected to maintain a market share above 35% through 2031 due to their established applications.

Geography Analysis

North America held 40.77% of 2025 revenue, driven by robust budgets from the DHS, DOE, and DOD for backpack and portal detectors, as well as specialized neutron-gated imaging systems. Mirion Technologies expanded its Tennessee facility in 2025, adding 60 employees to meet growing nuclear instrumentation demand. The United States also leads CubeSat radiation sensor programs, supported by Small Business Innovation Research (SBIR) grants to university spin-offs. In Canada, detector sales are tied to CANDU reactor monitoring and cross-border cargo screening, while Mexico focuses on seaport portal monitors under International Atomic Energy Agency (IAEA) guidance.

Asia-Pacific is projected to achieve the highest regional CAGR of 5.87% through 2031. China's Gen-III reactor construction requires perimeter radiation systems, while Japan's phased nuclear restarts necessitate upgraded spent-fuel pool monitors. India's diagnostic partnerships are driving PET/CT installations, creating opportunities for glass attenuation panels. South Korea and Taiwan are investing in CubeSat gamma-burst payloads that specify molded glass windows to reduce mass. ASEAN countries, including Vietnam, Thailand, and Indonesia, are deploying cost-effective backpack and portal detectors co-funded by the IAEA, boosting demand for mid-tier detector assemblies.

Europe's market is led by the UK, Germany, and France. The UK Radiological Nuclear Detection Framework has established a pre-approved vendor list and is midway through multi-million-pound contracts. German aerospace consortia are adopting inline CT with fast-decay glass screens, while France's 56-reactor fleet follows a fixed 10-year replacement cycle for boundary monitors. Sanctions have limited Western OEM access to Russia, prompting domestic glass research. Elsewhere, Brazil's research reactor modernization and Saudi Arabia's feasibility studies contribute small but strategic contracts, expanding the market footprint.

- Amcrys

- Berthold Technologies GmbH & Co. KG

- Collimated Holes, Inc.

- Dynasil Corporation

- Epic Crystal Co.

- Geebee Internationa

- Hamamatsu Photonics K.K.

- Jiaxing AOSITE Photonics Technology Co.,Ltd.

- Kinheng Crystal Material

- Kromek

- Ludlum Measurements

- Luxium Solutions

- Mirion Technologies

- Proterial, Ltd.

- Radiation Monitoring Devices (RMD)

- Rexon Components Inc.

- Saint-Gobain Ceramics & Plastics

- Scintacor

- Shanghai SICCAS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand in radiation detection and nuclear security

- 4.2.2 Expanding adoption in medical imaging (PET/CT)

- 4.2.3 Growth of industrial non-destructive testing (NDT)

- 4.2.4 Surge in homeland-security investments post-2025

- 4.2.5 Integration with photonic-chip sensors

- 4.2.6 CubeSat and small-sat missions need ultra-light detectors

- 4.3 Market Restraints

- 4.3.1 Lower light yield vs. crystal scintillators

- 4.3.2 High cost and process complexity for Li-6/B-10 glasses

- 4.3.3 Scarcity and price volatility of enriched isotopes

- 4.3.4 Radiation-induced glass darkening beyond 103 Gy

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Composition

- 5.1.1 Lithium-based Glass Scintillators

- 5.1.1.1 Natural-Li Glass

- 5.1.1.2 Enriched-Li-6 Glass

- 5.1.2 Boron-based Glass Scintillators

- 5.1.3 Phosphate Glass Scintillators

- 5.1.4 Other Compositions

- 5.1.1 Lithium-based Glass Scintillators

- 5.2 By Application

- 5.2.1 Medical Imaging (PET, PET/CT, SPECT)

- 5.2.2 Nuclear Power Plants and Radiation Monitoring

- 5.2.3 High-Energy Physics and Research

- 5.2.4 Industrial Inspection/NDT

- 5.2.5 Security and Defense

- 5.2.6 Space-borne and Astrophysics Detectors

- 5.2.7 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Healthcare

- 5.3.2 Energy and Power

- 5.3.3 Industrial Manufacturing

- 5.3.4 Defense and Homeland Security

- 5.3.5 Research and Academia

- 5.3.6 Oil and Gas Services

- 5.3.7 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Amcrys

- 6.4.2 Berthold Technologies GmbH & Co. KG

- 6.4.3 Collimated Holes, Inc.

- 6.4.4 Dynasil Corporation

- 6.4.5 Epic Crystal Co.

- 6.4.6 Geebee Internationa

- 6.4.7 Hamamatsu Photonics K.K.

- 6.4.8 Jiaxing AOSITE Photonics Technology Co.,Ltd.

- 6.4.9 Kinheng Crystal Material

- 6.4.10 Kromek

- 6.4.11 Ludlum Measurements

- 6.4.12 Luxium Solutions

- 6.4.13 Mirion Technologies

- 6.4.14 Proterial, Ltd.

- 6.4.15 Radiation Monitoring Devices (RMD)

- 6.4.16 Rexon Components Inc.

- 6.4.17 Saint-Gobain Ceramics & Plastics

- 6.4.18 Scintacor

- 6.4.19 Shanghai SICCAS

7 Market Opportunities and Future Outlook

- 7.1 Advanced glass formulations for higher light yield

- 7.2 White-space and Unmet-Need Assessment