PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062243

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062243

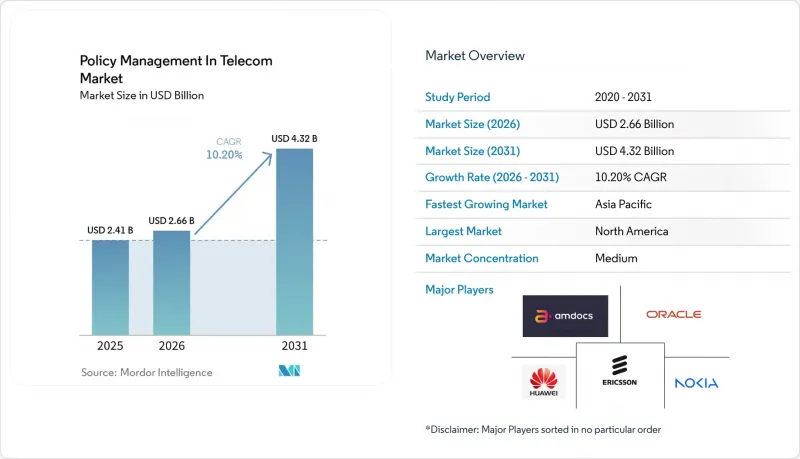

Policy Management In Telecom - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the policy management in the telecom industry market size is projected to expand from USD 2.41 billion in 2025 and USD 2.66 billion in 2026 to USD 4.32 billion by 2031, registering a CAGR of 10.20% between 2026 and 2031.

This report is Segmented by Component (Solutions, and More), Deployment Model (Cloud-Based, and More), Application (Mobile Data Policy Control, Voice/VoLTE and IMS Policy, Security/Parental-Control and Content Policy, and More), Operator Type (Mobile Network Operators, Fixed/Broadband Operators, and More), and Geography (Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Policy Management In Telecom Market Trends and Insights

Rising Mobile-Data Traffic And Fair-Usage Enforcement

Video streaming, cloud gaming, and augmented reality push data volumes upward, compelling operators to refine fair-usage rules that preserve customer experience while curbing congestion. Sub-100-millisecond decision cycles enabled by cloud-native policy engines let networks throttle or reprioritize flows the instant a cell reaches capacity. Operators in high-growth markets are therefore automating rule execution instead of relying on manual policy updates that once took hours. Upgrades to 400 Gbps internet-exchange backbones show the investment scale needed to match data growth, and the practice illustrates why real-time congestion mitigation now sits at the heart of every strategic roadmap.

CSP Transition To Cloud-Native 5G-Core Architectures

Containerized policy control function micro-services conforming to 3GPP Release 15 and Release 16 specifications replace monolithic appliances, unlocking continuous integration pipelines and elastic scaling. Operators migrating to these architectures trim upfront hardware spending by nearly 40% and roll out new rules in hours rather than weeks. Hybrid deployments keep latency-sensitive transactions on premises to meet data residency laws, while non-critical analytics move to public clouds, balancing compliance with cost. Markets that solve integration pain points first gain earlier access to service-based monetization models such as network slicing.

Legacy PCRF And BSS Integration Complexity

Operators running proprietary interfaces between older billing platforms and legacy policy engines often face multi-year cutovers, which significantly impact operational efficiency. During this transition, parallel operations are required, effectively doubling overhead costs until the decommissioning process is complete. This prolonged migration not only stretches budgets but also diverts critical engineering talent that could be utilized to develop and refine monetization use cases. Additionally, the reliance on custom mediation layers further extends payback periods, delaying the realization of returns on investment. These challenges also hinder the timely deployment of advanced service-based architecture features, limiting the ability to offer innovative services to customers. As a result, operators face significant delays in modernizing their infrastructure and achieving operational agility.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push For Real-Time Roaming Bill-Shock Prevention

- Monetisation Needs For Network Slicing And Enterprise SLAs

- Operator CAPEX Constraints In Low-ARPU Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions held 61.90% of 2025 revenue within the policy management in telecom industry market size, underscoring the importance of license-driven software elements such as policy control function instances and convergent charging engines. These solutions are critical for enabling telecom operators to manage network policies effectively while ensuring seamless customer experiences. Managed services are growing at a 12.40% CAGR as carriers increasingly shift operational risks to external specialists to focus on core business functions. The convergence of charging, policy orchestration, and revenue assurance within outcome-based contracts is becoming a preferred approach for operators. This trend is driven by the need for predictable operating expenses over periodic capital expenditure spikes, which can strain budgets. Additionally, the growing complexity of telecom networks further emphasizes the importance of robust policy management solutions.

Skills shortages in the telecom industry are also driving demand for service providers who offer comprehensive solutions. These providers often bundle migration consulting, slice lifecycle management, and artificial-intelligence-driven assurance into multi-year agreements, addressing the operational challenges faced by carriers. As more telecom operators transition to cloud-native cores, the demand for managed services is expected to grow significantly. Service revenue is likely to close the gap with solutions revenue, as ongoing optimization and compliance validation require continuous external support. This shift highlights the increasing reliance on external expertise to manage the complexities of modern telecom networks. Furthermore, the adoption of advanced technologies and regulatory compliance needs are expected to sustain the growth of managed services in the forecast period.

Cloud variants commanded 71.20% market share in 2025, establishing the cloud as the primary platform for new policy deployments. Public clouds cater to small and mid-size operators that lack the resources to maintain large-scale data centers. In contrast, private and sovereign clouds are preferred by tier-one operators that must adhere to stringent data residency and security regulations. Hybrid models are gaining traction, combining on-premises real-time enforcement with analytics offloaded to hyperscaler regions. This approach allows operators to balance compliance requirements with the scalability and flexibility offered by cloud solutions. As a result, the cloud continues to dominate as the preferred choice for policy management in the telecom industry.

On-premises systems are experiencing a decline in market share but remain relevant in regions with limited public-cloud infrastructure or strict national-security restrictions. These systems are often the only viable option in jurisdictions where public-cloud adoption is hindered by regulatory or technological barriers. However, hybrid cloud models are gradually bridging this gap by demonstrating successful use cases that combine the benefits of both on-premises and cloud-based solutions. Over time, these hybrid deployments are expected to reduce resistance to cloud adoption and encourage a shift toward multi-tenant infrastructure. This transition is anticipated to further solidify the cloud's role as a critical driver of growth in telecom policy management.

Geography Analysis

North America delivered 28.20% of 2025 revenue for the policy management in telecom industry market thanks to early 5G standalone deployments, robust hyperscaler ecosystems, and enterprise appetite for private networks. Operators leverage Citizens Broadband Radio Service rules to embed policy control inside on-premises enterprise networks, broadening addressable demand beyond traditional consumer bases. Artificial-intelligence-powered orchestration sees rapid pilot-to-production cycles, buttressing growth.

Asia-Pacific is forecast to record a 15.80% CAGR through 2031, the fastest globally, as massive 5G subscriber additions in China and policy-linked government programs in India fuel new rollouts. Standalone core expansion to hundreds of thousands of base stations generates unprecedented volumes of policy transactions, forcing carriers to adopt elastic, cloud-native control planes. Early adoption of intent-based networking in Japan and South Korea further solidifies the region's forward momentum.

Europe shows measured progress, paced by mandates for real-time roaming alerts and strong data privacy regimes that skew architecture toward hybrid clouds. Middle Eastern operators invest aggressively in 6G research and spectrum harmonization, positioning the Gulf Cooperation Council as a test bed for next-generation policy architectures. Sub-Saharan Africa and South America remain constrained by capital budgets, yet managed service models, tied to revenue share rather than heavy upfront fees, carve a sustainable pathway to modernization.

- Amdocs Ltd.

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- Huawei Technologies Co., Ltd.

- Oracle Corporation

- Netcracker Technology Corporation

- Cisco Systems, Inc.

- Hewlett Packard Enterprise Company

- MATRIXX Software, Inc.

- Comarch S.A.

- Intracom Telecom S.A.

- CSG Systems International, Inc.

- Openet Telecom Ltd. (Amdocs Subsidiary)

- ZTE Corporation

- Tecnotree Oyj

- Optiva Inc.

- Alepo Technologies, Inc.

- Sterlite Technologies Ltd.

- DigitalRoute AB

- Accuris Networks Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Mobile-Data Traffic and Fair-Usage Enforcement

- 4.2.2 CSP Transition to Cloud-Native 5G-Core Architectures

- 4.2.3 Regulatory Push for Real-Time Roaming Bill-Shock Prevention

- 4.2.4 Monetisation Needs for Network Slicing and Enterprise SLAs

- 4.2.5 AI-Assisted Dynamic QoS and Intent-Based Policies

- 4.2.6 Private-Network PCC Demand from Industry 4.0 Campuses

- 4.3 Market Restraints

- 4.3.1 Legacy PCRF/BSS Integration Complexity

- 4.3.2 Operator CAPEX Constraints in Low-ARPU Markets

- 4.3.3 Security Concerns Around Multi-Vendor Cloud Deployments

- 4.3.4 Edge-Cloud Orchestration Immaturity

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 On-Premises

- 5.2.2 Cloud-Based (Public, Private, Hybrid)

- 5.3 By Application

- 5.3.1 Mobile Data Policy Control

- 5.3.2 Voice/VoLTE and IMS Policy

- 5.3.3 Roaming and Interconnect Policy

- 5.3.4 Security/Parental-Control and Content Policy

- 5.4 By Operator Type

- 5.4.1 Mobile Network Operators (MNO)

- 5.4.2 Fixed/Broadband Operators

- 5.4.3 Mobile Virtual Network Operators (MVNO)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Russia

- 5.5.2.8 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 ASEAN

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Turkey

- 5.5.4.4 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Nigeria

- 5.5.5.3 Egypt

- 5.5.5.4 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amdocs Ltd.

- 6.4.2 Telefonaktiebolaget LM Ericsson

- 6.4.3 Nokia Corporation

- 6.4.4 Huawei Technologies Co., Ltd.

- 6.4.5 Oracle Corporation

- 6.4.6 Netcracker Technology Corporation

- 6.4.7 Cisco Systems, Inc.

- 6.4.8 Hewlett Packard Enterprise Company

- 6.4.9 MATRIXX Software, Inc.

- 6.4.10 Comarch S.A.

- 6.4.11 Intracom Telecom S.A.

- 6.4.12 CSG Systems International, Inc.

- 6.4.13 Openet Telecom Ltd. (Amdocs Subsidiary)

- 6.4.14 ZTE Corporation

- 6.4.15 Tecnotree Oyj

- 6.4.16 Optiva Inc.

- 6.4.17 Alepo Technologies, Inc.

- 6.4.18 Sterlite Technologies Ltd.

- 6.4.19 DigitalRoute AB

- 6.4.20 Accuris Networks Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment