PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062247

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062247

High Strength Aluminum Alloys - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

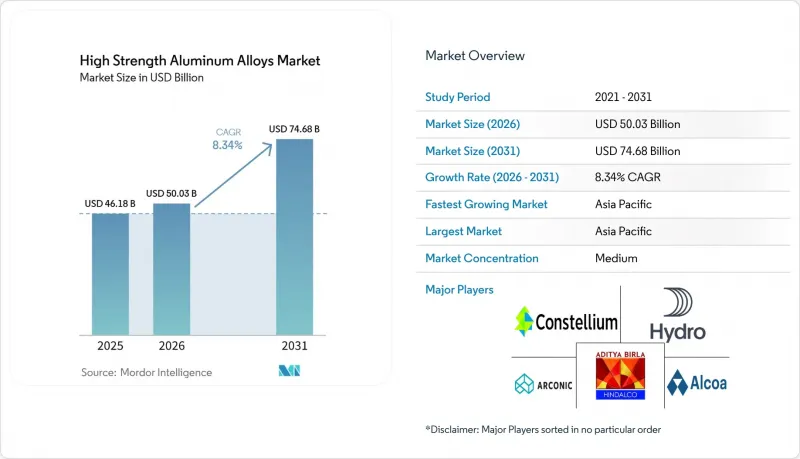

According to Mordor Intelligence, the high strength aluminum alloys market size is expected to grow from USD 46.18 billion in 2025 to USD 50.03 billion in 2026 and is forecast to reach USD 74.68 billion by 2031 at 8.34% CAGR over 2026-2031.

This report is Segmented by Grade (6xxx Series, and More), Product Form (Plates and Sheets, and More), Processing Technique (Heat-Treated, and More), End-User Industry (Aerospace and Defense, Automotive and Transportation, and More), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global High Strength Aluminum Alloys Market Trends and Insights

Growing Demand from Aerospace and Defense for Lightweighting

Airframe manufacturers are embedding high strength aluminum alloys market specifications into new platforms to hit stringent fuel-burn targets. Boeing and Airbus increased single-aisle build rates to 38 and 75 units per month, respectively, in 2026, each fuselage skin containing more than 800 kg of 7xxx and 2xxx plate. In naval programs, the U.S. Navy's DDG-51 Flight III destroyer mandates 5xxx-series marine plate to cut topside weight by 12%, permitting heavier radar systems without compromising stability. Rocket manufacturers such as SpaceX employ Al-Li stringers in reusable stages to survive repeated cryogenic cycles. Regulators at the European Union Aviation Safety Agency (EASA) and the Federal Aviation Administration (FAA) enforce AMS 4999 and AMS 7003 compliance, driving mills to tighten process control. The cumulative effect lifts multi-year demand visibility, incentivizing integrated producers to expand forging and heat-treat capacity adjacent to final-assembly lines.

Increasing Adoption in EV Battery Enclosures and Platforms

Automotive architects are converging on aluminum-intensive underbodies to offset battery mass. Novelis shipped more than 500,000 tons of 6xxx automotive sheet in 2025, half earmarked for battery enclosures that outperform steel in IIHS crash protocols. One-piece extrusion trays eliminate up to 40 fasteners, cutting assembly time 15% and reducing warranty claims tied to water ingress. China's MIIT awards subsidies to EVs under 12 kWh/100 km, nudging OEMs toward aluminum-rich platforms like BYD Seal. While thicker gauges are needed versus press-hardened steel, total curb-weight savings of 80-100 kg justify a USD 150-200 per vehicle material premium. Suppliers co-locate extrusion, stamping, and friction-stir welding cells near OEM plants to shorten design iterations.

High Cost of Processing and Critical Alloying Elements

Solution heat treatment at up to 530°C and artificial aging regimes consume 1,500 kWh per ton, exposing European mills to energy shocks that pushed electricity prices 40% higher in 2024. Scandium master alloy trades around USD 4,000/kg, 200 times base aluminum, restricting economic viability to aerospace bulkheads or cryogenic tanks. Lithium at USD 12,000-15,000/ton also stresses cost structures, and geopolitical concentration heightens risk. Kaiser Aluminum shuttered its Spokane heat-treat line, citing unsustainable power tariffs, underscoring a two-tier market where only integrated producers running renewable power can achieve sub-USD 1,800/ton cash costs.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of High-Speed Rail and Urban Transit Projects

- Lightweighting Push in Construction and Industrial Equipment

- Weldability and Stress-Corrosion Sensitivities in Some Grades

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 6xxx series remains the volume leader, securing 39.65% market share in 2025 on the back of EV battery-enclosure contracts and rail-car extrusions. The high-strength aluminum alloys market share advantage is expected to narrow as cost-effective scandium micro-additions enable thinner 6xxx profiles without sacrificing crashworthiness. Meanwhile, 2xxx and 5xxx series maintain niche defensibility in legacy wide-body aircraft and cryogenic tanks, respectively, with research and development dollars mostly channeling toward aluminum-lithium hybrids for next-generation reusable launchers.

The 7xxx series is projected to expand at 9.22% CAGR to 2031. High zinc content delivers ultimate tensile strength above 570 MPa, indispensable for fuselage frames and naval radar masts. Boeing's and Airbus's production surges anchor forward-purchase agreements through 2030, ensuring consistent mill utilization. Additive manufacturing further lifts 7xxx demand as LPBF achieves density within 0.5% of wrought plate after HIP consolidation.

Plates and sheets delivered 41.02% revenue share in 2025 by serving aircraft skins, rail roofs, and EV body panels. However, powders, foils, and wires are forecast to outpace with a 9.57% CAGR, riding on additive manufacturing and solid-state battery opportunities. The high-strength aluminum alloys market size for ultra-thin battery foil alone is projected to increase significantly between 2026 and 2031 as solid-state developers specify 10-20 micron collectors.

Extrusions continue to underpin automotive and building segments thanks to favorable weight-to-stiffness economics and mature welding methods. Forgings secure ultra-high reliability niches, landing gear, and naval shafts, where grain-flow orientation and fatigue life trump cost. Mass-reduction imperatives nonetheless steer capital toward powder atomization and ultra-thin rolling capabilities, reshuffling the profitability hierarchy among semi-fabricators.

Geography Analysis

Asia-Pacific held 44.69% of 2025 demand and will compound at 9.56% CAGR through 2031, fueled by China's rail build-out and Japan's aerospace forgings export program. India's extrusion hubs in Gujarat and Maharashtra supply European tier-1s, leveraging labor advantages to offset logistics costs. Southeast Asian nations chase substitution opportunities as OEMs de-risk China exposure.

North America scales capacity under reshoring mandates: Alcoa's San Ciprian rebuild, and Novelis's Bay Minette mill inject a combined 675,000 tons of annual sheet and forging output by 2027. Defense budgets channel steady 7xxx orders, while the U.S. Infrastructure Act allocates rail modernizations that consume 6xxx extrusions.

Europe balances aggressive carbon policy with automotive lightweighting. Norsk Hydro's hydropower smelters supply premium low-carbon billet, qualifying for CBAM relief. Rail corridor investments and OEM multi-material bodies force mills to juggle plate, extrusion, and foil specialties. South America and the Middle East stay sub-scale but attract 5xxx plate demand for LNG carriers and offshore wind-support vessels.

- Akshay Aluminium Alloys

- Alcoa Corporation

- Aluminum Corporation of China (Chalco)

- AMAG Austria Metall AG

- Arconic

- Belmont Metals

- Constellium SE

- ElvalHalcor

- Emirates Global Aluminium PJSC

- Fischer Group

- GARMCO

- Granges

- Hindalco Industries Ltd.

- Kaiser Aluminum Corp.

- KOBE STEEL, LTD.

- Norsk Hydro ASA

- Rio Tinto

- UACJ Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand from aerospace and defence for lightweighting

- 4.2.2 Increasing adoption in EV battery enclosures and platforms

- 4.2.3 Expansion of high-speed rail and urban transit projects

- 4.2.4 Light-weighting push in construction and industrial equipment

- 4.2.5 Uptake in cryogenic hydrogen-storage vessels (H2 economy)

- 4.2.6 Demand from satellite constellations and re-usable launchers

- 4.3 Market Restraints

- 4.3.1 High cost of processing and critical alloying elements

- 4.3.2 Weldability and stress-corrosion sensitivities in some grades

- 4.3.3 Competition from advanced steels and carbon-composite hybrids

- 4.3.4 Supply-risk of scandium/lithium for ultra-high-strength series

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Grade

- 5.1.1 6xxx Series (Al-Mg-Si)

- 5.1.2 2xxx Series (Al-Cu)

- 5.1.3 5xxx Series (Al-Mg)

- 5.1.4 7xxx Series (Al-Zn)

- 5.1.5 Other High-Strength Grades (Sc, Li-Al, and More)

- 5.2 By Product Form

- 5.2.1 Plates and Sheets

- 5.2.2 Extrusions

- 5.2.3 Forgings

- 5.2.4 Castings

- 5.2.5 Bars, Rods and Tubes

- 5.2.6 Other Forms (Powders, Foils, and Wires)

- 5.3 By Processing Technique

- 5.3.1 Heat-Treated

- 5.3.2 Non-Heat-Treated

- 5.3.3 Cold-Worked

- 5.3.4 Powder Metallurgy and Additive Manufacturing

- 5.4 By End-user Industry

- 5.4.1 Aerospace and Defence

- 5.4.2 Automotive and Transportation

- 5.4.3 Marine and Shipbuilding

- 5.4.4 Construction and Infrastructure

- 5.4.5 Electronics and Electrical

- 5.4.6 Industrial Equipment

- 5.4.7 Other End-users (Energy and Packaging)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.5.4 Rest of MEA

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)}

- 6.4.1 Akshay Aluminium Alloys

- 6.4.2 Alcoa Corporation

- 6.4.3 Aluminum Corporation of China (Chalco)

- 6.4.4 AMAG Austria Metall AG

- 6.4.5 Arconic

- 6.4.6 Belmont Metals

- 6.4.7 Constellium SE

- 6.4.8 ElvalHalcor

- 6.4.9 Emirates Global Aluminium PJSC

- 6.4.10 Fischer Group

- 6.4.11 GARMCO

- 6.4.12 Granges

- 6.4.13 Hindalco Industries Ltd.

- 6.4.14 Kaiser Aluminum Corp.

- 6.4.15 KOBE STEEL, LTD.

- 6.4.16 Norsk Hydro ASA

- 6.4.17 Rio Tinto

- 6.4.18 UACJ Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Next-gen alloy development for aerospace electrification and EV batteries