PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062256

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062256

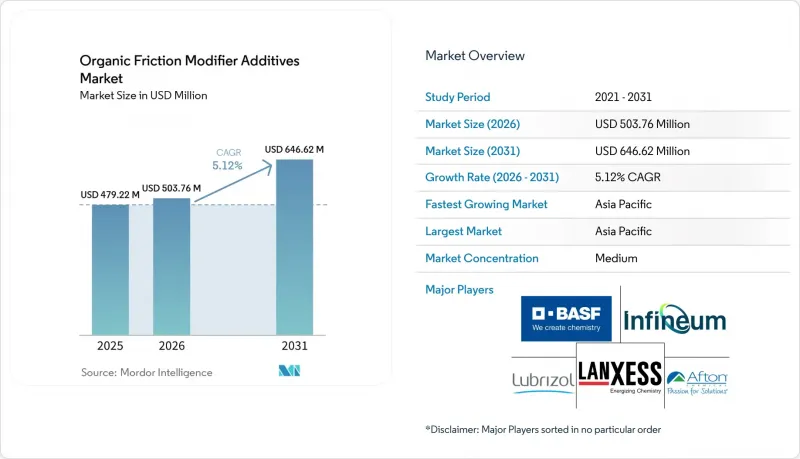

Organic Friction Modifier Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the organic friction modifier additives market size is projected to be USD 479.22 million in 2025, USD 503.76 million in 2026, and reach USD 646.62 million by 2031, growing at a CAGR of 5.12% from 2026 to 2031.

This report is Segmented by Type (Ester-Based Friction Modifiers, Amide-Based Friction Modifiers, and More), Form (Liquid and Solid), Application (Engine Oils, Gear Oils, Greases and More), End-User Industry (Marine and Rail and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle- East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Organic Friction Modifier Additives Market Trends and Insights

Stricter Environmental Regulations on Engine-Oil Formulations

Regulatory agencies are capping phosphorus, sulfur, and sulfated ash, which forces blenders to shift from metallic to organic friction modifiers. The EU's 2024 REACH reclassification of short-chain chlorinated paraffins created an immediate need for ashless alternatives. The United States Environmental Protection Agency finalized Tier 4 limits in 2025 that require diesel lubricants compatible with after-treatment devices. China's GB 11121-2024 specification restricts phosphorus to 0.06%, making glycerol mono-oleate and PIB-succinimide derivatives indispensable. These simultaneous rules are accelerating the adoption curve for ester and amide molecules that hold friction coefficients below 0.08 without poisoning catalytic hardware. Suppliers that completed field trials ahead of the 18-month OEM approval cycle now enjoy first-mover pricing power.

Growing Penetration of Automatic and Dual-Clutch Transmissions

Automatic and dual-clutch units represented 68% of 2025 passenger-car builds, up seven points from 2023, with Asia-Pacific adding most of the volume. Dual-clutch boxes rely on organic modifiers dosed at 0.3%-0.8% to keep clutch friction steady between -40°C and 150°C. Chinese output reached 5.5 million dual-clutch cars in 2025 as BYD and Geely moved to seven- and eight-speed designs to meet 4.0 L/100 km fuel targets. Continuously variable units need thermally robust amides to stabilize belt traction, while North American OEMs pushed eight- and ten-speed automatics to 42% penetration, further lifting demand. Longer 10-year warranties oblige fluids to hold oxidation stability beyond 100,000 km, which is reshaping additive treat packages.

Raw-Material Supply Risks (Oleochemicals, Esters, Amines)

Palm-oil levies in Indonesia lifted oleic-acid prices by 34% in Q1 2025 and squeezed additive margins for blenders without integrated feedstock positions. Only 40% of spot palm oil meets the less than 2 mg KOH/g acid-value spec, forcing upstream purification or premium sourcing. Propylene-oxide capacity trails downstream needs, creating a looming 1.1-million-ton shortfall by 2031, which is inflating costs for amine modifiers. Petronas Chemicals opened a 50,000-tons/year oleochemical hub in Johor in 2025 to secure a captive supply and cut volatility. Castor oil and algae pathways are still under 5% of feedstock, but pilot projects aim for 10% by 2028.

Other drivers and restraints analyzed in the detailed report include:

- Development of High-Temperature Long-Drain Synthetic Lubricants

- Formulation Synergies with Ionic-Liquid Boosters in Hybrid Powertrains

- Compatibility Issues with Certain Base Oils and Additive Packs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ester-based molecules secured 41.11% of the organic friction modifier additives market share in 2025, owing to excellent thermal stability and low-viscosity compatibility demanded by GF-6B and ACEA C5 oils. Glycerol mono-oleate and sorbitan esters deliver friction coefficients near 0.07 at 0.5%-1.0% dosages, whereas di(2-ethylhexyl) adipate has become the e-axle benchmark because of low conductivity. Amide products priced 25% below esters are catching up fast, led by oleamide in transmission fluids that promise a 5.63% CAGR during the forecast period (2026-2031).

Amide durability tapers above 130°C, which limits usage in high-temperature sump environments. Mixed ester-amine hybrids under BASF's 2025 patent aim to merge ester heat stability with amine polarity for friction below 0.06 in 0W-12 oils. Acid-based modifiers stay niche in greases and metal-forming fluids, while multifunctional polymeric dispersants are gaining share in heavy-duty diesel oils that require simplified additive slates.

Liquid products comprised 83.34% of the organic friction modifier additives market size in 2025 because they blend easily into Group III and polyalphaolefin oils through automated dosing. Precise treat-rate control down to 0.3% lets OEMs target exact friction curves, which secures strong demand.

Solid (powder/dispersible) is set for a 5.99% CAGR to 2031, mainly through molybdenum disulfide and graphite packages used in sealed EV bearings. Nanometer-scale PTFE introduced by Shamrock in 2025 resists sedimentation for 12 months and meets servo-valve cleanliness in aerospace hydraulics. EU micro-plastics policy could, however, cap further carbon-based powder growth if particle persistence triggers new disposal rules.

Geography Analysis

Asia-Pacific led with 52.22% of 2025 revenue and is forecast for a 6.26% CAGR through 2031. China built 30.5 million vehicles, including 9.8 million EVs, each unit demanding low-viscosity oils that depend on organic friction modifiers for compliance with China-6b limits. India's 5.8 million-unit output and 21.2 million two-wheelers also adopt BS-VI Phase 2 oils that cap particulates at 4.5 mg/km. ASEAN investment surged after Petronas opened a regional additive hub in Johor in 2025. Japan and South Korea continue as innovation centers for ionic-liquid hybrids.

In North America, the United States light-vehicle builds climbed to 10.8 million, while Class 8 trucks hit 320,000 units and now need API CK-4 oils containing ashless modifiers for after-treatment durability. Canadian winter grades such as 0W-16 rely on ester friction modifiers for -40°C pumpability. Afton doubled its Monterrey capacity in 2025 to serve Mexican exports. EPA Tier 4 off-road mandates and California LEV rules are prompting faster metal-free adoption.

In Europe, Germany's 3.8 million vehicles, including 1.2 million EVs, require ultra-low-friction e-axle fluids. Pending micro-plastics limits triggered EUR 45 million in research and development for biodegradable esters by BASF and Lubrizol in 2025. Norway's 90% EV share spurred demand for -30°C-capable e-axle lubricants. South America's market share is led by Brazil's 2.3 million vehicles, while the Middle East and Africa share is supported by mining and petrochemical hydraulics.

- ADEKA CORPORATION

- Afton Chemical

- BASF

- Cargil Incorporated

- Infineum International Ltd.

- King Industries, Inc.

- LANXESS

- Lubrizol

- Nouryon

- Petronas Chemicals Group Berhad

- R.T. Vanderbilt Holding Company, Inc.

- Shamrock Technologies

- The W Corporation

- Yasho Industries Limited

- ZSCHIMMER & SCHWARZ, INC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter environmental regulations on engine-oil formulations

- 4.2.2 Growing penetration of automatic and dual-clutch transmissions

- 4.2.3 Development of high-temperature, long-drain synthetic lubricants

- 4.2.4 Formulation synergies with ionic-liquid boosters in hybrid powertrains

- 4.2.5 OEM warranty extensions for ultra-low-friction e-axle lubricants

- 4.3 Market Restraints

- 4.3.1 Raw-material supply risks (oleochemicals, esters, amines)

- 4.3.2 Compatibility issues with certain base oils and additive packs

- 4.3.3 Pending EU micro-plastics legislation on long-chain alkyl esters

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Ester-Based Friction Modifiers

- 5.1.2 Amide-Based Friction Modifiers

- 5.1.3 Acid-Based Friction Modifiers

- 5.1.4 Amine-Based Friction Modifiers

- 5.1.5 Other Organic Friction Modifiers

- 5.2 By Form

- 5.2.1 Liquid

- 5.2.2 Solid (Powder / Dispersible)

- 5.3 By Application

- 5.3.1 Engine Oils

- 5.3.2 Transmission Fluids (ATF, DCTF, CVTF)

- 5.3.3 Gear Oils

- 5.3.4 Hydraulic Fluids

- 5.3.5 Greases

- 5.3.6 Metalworking Fluids

- 5.3.7 Other Specialty Lubricants

- 5.4 By End-user Industry

- 5.4.1 Automotive and Transportation

- 5.4.2 Industrial Manufacturing and Machinery

- 5.4.3 Aerospace and Aviation

- 5.4.4 Energy and Power Generation

- 5.4.5 Marine and Rail

- 5.4.6 Other End-user Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 ADEKA CORPORATION

- 6.4.2 Afton Chemical

- 6.4.3 BASF

- 6.4.4 Cargil Incorporated

- 6.4.5 Infineum International Ltd.

- 6.4.6 King Industries, Inc.

- 6.4.7 LANXESS

- 6.4.8 Lubrizol

- 6.4.9 Nouryon

- 6.4.10 Petronas Chemicals Group Berhad

- 6.4.11 R.T. Vanderbilt Holding Company, Inc.

- 6.4.12 Shamrock Technologies

- 6.4.13 The W Corporation

- 6.4.14 Yasho Industries Limited

- 6.4.15 ZSCHIMMER & SCHWARZ, INC.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment