PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062259

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062259

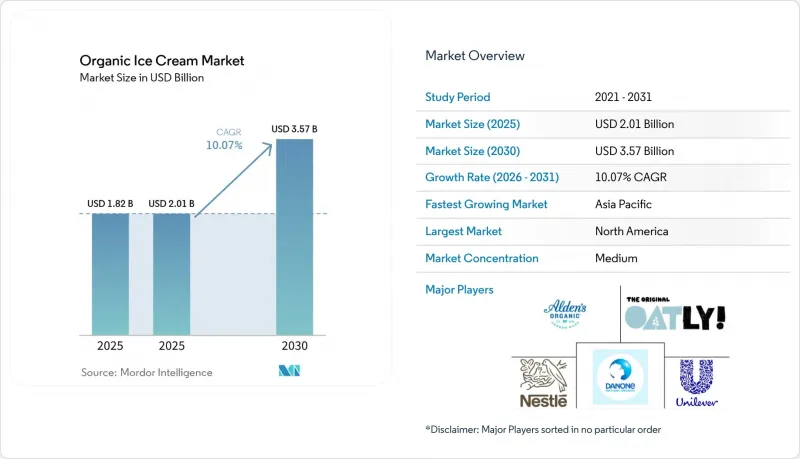

Organic Ice Cream - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the organic ice cream market size was valued at USD 1.82 billion in 2025 and estimated to grow from USD 2.01 billion in 2026 to reach USD 3.57 billion by 2031, at a CAGR of 10.07% during the forecast period (2026-2031).

This report is Segmented by Ingredient Source (Dairy-Based, Non-Dairy-Based), Flavor (Vanilla, Chocolate, Fruit-Flavored, Others), Product Type (Pints, Cones, Bars, Others), Distribution Channel (Foodservice, Retail), and Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Global Organic Ice Cream Market Trends and Insights

Organic dairy sourcing as a premium trust signal

Certified organic dairy sourcing has emerged as a decisive brand differentiator, particularly as consumers scrutinize supply-chain transparency and animal welfare practices. The global organic farmland base reached 98.9 million hectares in 2023, representing 2.1% of total agricultural land, with Oceania (53.2 million hectares), Europe (19.5 million hectares), and Latin America (10.3 million hectares) leading in certified acreage according to The Research Institute of Organic Agriculture FiBL. Organic dairy cows in Argentina increased 5.7% to 4,618 head in 2024, supporting export-oriented organic ice cream ingredient supply chains targeting North America and Europe, according to SENASA Argentina. U.S. organic milk exports surged 102.6% year-over-year in the first nine months of 2025, though 74% of shipments remained within North America under USMCA tariff-free provisions, limiting immediate impact on Asia-Pacific ingredient availability, as per NODPA. This dynamic creates a two-tier market: established North American and European brands leverage domestic organic dairy networks to reinforce provenance claims, while Asia-Pacific entrants face higher import costs or must develop nascent local organic dairy infrastructure. Global consumers indicate a willingness to pay more for natural or all-natural claims and for packaged foods with natural ingredients.

Flavor Innovation using organic inclusions

Flavor innovation anchored in organic inclusions is driving differentiation and repeat purchase, particularly as vanilla's 31.37% share in 2025 signals saturation risk for single-note offerings. Fruit-flavored variants are accelerating at 10.75% CAGR through 2031, propelled by organic berry, mango, passion fruit, and exotic inclusions that command premium pricing and appeal to adventurous consumers. Organic vanilla pricing volatility, driven by cyclone damage in Madagascar and supply concentration, has incentivized formulators to diversify into organic cocoa, coffee, matcha, and botanical extracts sourced from certified fair-trade cooperatives. Whitey's Ice Cream introduced dairy-free pea protein flavors in February 2026, incorporating organic fruit purees and adaptogens to target wellness-oriented consumers. The technical challenge lies in maintaining flavor stability and color vibrancy without synthetic preservatives or artificial colors; natural vegetable-derived colors (carrot, beet, turmeric) and fermentation-derived flavor enhancers are gaining traction as clean-label alternatives, though they introduce cost premiums and processing complexity, according to the Institute of Food Technologists. Inclusion innovation extends to texture: organic cookie dough, brownie chunks, and nut-based swirls must meet organic certification standards while delivering indulgent sensory cues that justify premium pricing.

High cost of certified organic dairy and ingredients

Certified organic dairy commands substantial cost premiums, compressing manufacturer margins and limiting mass-market penetration. Pennsylvania organic milk averaged USD 38.43 per hundredweight in December 2024, while Northeast regional pay prices ranged from USD 35-45 per hundredweight for grain and pasture-fed organic milk, USD 38-50+ for grass-fed, and USD 50-60 for regenerative organic or A2A2 certified milk, according to the USDA. Dutch organic milk processor guaranteed prices stood at EUR 63.50 per 100 kilograms (USD 65.08) in January 2025, down slightly from December but still reflecting elevated input costs driven by organic feed grain inflation. Organic feed corn traded at USD 8.23 per bushel and organic feed soybeans at USD 22.57 per bushel in November 2025, well above conventional equivalents, according to the USDA AMS. Retail pricing reflects these upstream pressures: organic ice cream (48-64 ounce packages) averaged USD 8.42 nationally in March 2026, a USD 4.08 premium over conventional products, limiting purchase frequency among price-sensitive households. Brands unable to secure long-term organic ingredient contracts or pass through cost increases face margin erosion, while smaller artisanal producers struggle to achieve procurement scale economies, constraining market entry and expansion.

Other drivers and restraints analyzed in the detailed report include:

- Growth of lactose-free organic dairy variants

- Strengthening food safety and organic certification standards

- Shorter shelf life due to clean-label formulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dairy-based organic ice cream commanded 65.83% market share in 2025, underpinned by consumer familiarity, superior creaminess from milkfat, and established organic dairy supply chains in North America and Europe. Traditional organic dairy formulations leverage butterfat content (10-16%) to deliver an indulgent mouthfeel and flavor-carrying capacity, remaining the sensory benchmark for premium frozen desserts. Regulatory compliance frameworks under USDA NOP and EU Regulation 2018/848 permit organic certification for both dairy and non-dairy products, provided that all agricultural ingredients meet organic production standards and that processing aids (enzymes, cultures) derive from non-GMO sources. Whitey's Ice Cream introduced pea protein-based organic flavors in February 2026, positioning them as high-protein (8-10 grams per serving) to attract fitness-oriented consumers. The technical challenge for non-dairy organic formulations lies in replicating dairy's fat globule structure and protein matrix. Plant proteins lack casein's emulsifying properties and require higher stabilizer loads or precision fermentation ingredients (such as Perfect Day's whey protein) to achieve comparable texture and freeze-thaw stability. Patent activity reflects this innovation focus: China leads global ice cream patents with over 40% of active filings, followed by Western multinationals Unilever and Nestle, with plant-based base formulations, natural stabilizers, and energy-efficient freezing processes dominating recent applications.

Non-dairy organic variants are expanding at 11.86% CAGR through 2031, driven by plant-based bases including oat, pea protein, cashew, almond, and hemp milk that appeal to vegan, lactose-intolerant, and environmentally conscious consumers. Unilever's Ben & Jerry's reformulated its non-dairy line with oat bases in 2024, capitalizing on oat milk's neutral flavor profile and creamy texture that more closely mimics dairy than earlier coconut or almond formulations. The non-dairy segment faces ingredient sourcing constraints, organic oat, almond, and pea protein supplies are concentrated in North America and Europe, with limited certified production in Asia-Pacific, elevating import dependency and cost for regional manufacturers. Conversely, dairy-based organic ice cream confronts supply volatility: Pennsylvania organic milk production volumes fell 24% from October to December 2024 due to drought and feed scarcity, tightening cream availability for ice cream manufacturers. This supply-demand imbalance is pushing dairy-based brands toward vertical integration strategies (direct farm partnerships, cooperative ownership) to secure consistent organic milk flows, while non-dairy entrants leverage flexible ingredient sourcing across multiple plant-base platforms to mitigate single-commodity risk.

Vanilla captured 31.37% flavor share in 2025, reflecting its role as the foundational profile for mix-ins, toppings, and multi-flavor pints, yet its growth trajectory is moderating as consumers seek novelty and functional benefits beyond classic offerings. Vanilla's enduring share reflects its versatility and lower formulation risk, but brands over-indexed to vanilla face commoditization pressure and must differentiate via bean origin (Madagascar, Tahitian, Mexican), extraction method (cold-pressed, alcohol-free), or stacked certifications (organic, fair trade, regenerative) to justify premium pricing in an increasingly crowded segment. Flavor innovation is increasingly tied to functional positioning: organic matcha ice cream delivers antioxidant claims, coffee variants incorporate fair-trade certified beans, and adaptogen-infused flavors (ashwagandha, reishi mushroom) target wellness-oriented buyers. Straus Family Creamery's gluten-free organic cookie dough launch in January 2025 exemplifies cross-functional innovation, addressing allergen concerns while maintaining indulgent flavor delivery.

Fruit-flavored organic ice cream is accelerating at 10.75% CAGR through 2031, propelled by organic berry (strawberry, blueberry, raspberry), tropical (mango, passion fruit, guava), and stone fruit (peach, cherry) variants that leverage seasonal harvest cycles and regional sourcing narratives. Chocolate remains a stable secondary segment, benefiting from organic cocoa certification growth in Latin America (Ecuador, Peru, Dominican Republic) and West Africa, though cocoa price volatility and ethical sourcing scrutiny require brands to maintain transparent supply-chain documentation. Other flavors, encompassing coffee, matcha, salted caramel, and botanical infusions (lavender, rose, earl grey), are gaining traction in specialty channels and artisanal brands targeting experiential consumers willing to pay premiums for limited-edition releases and hyper-seasonal offerings. The technical complexity of fruit-flavored organic formulations centers on color and flavor stability, natural fruit purees and juices oxidize and degrade faster than synthetic flavors, requiring careful pH management, antioxidant addition (ascorbic acid from organic sources), and cold-chain discipline to preserve vibrancy through shelf life.

Geography Analysis

North America accounted for 38.64% of global organic ice cream revenue in 2025, underpinned by the United States' well-established organic dairy ecosystem, strong consumer familiarity with organic labeling, and extensive retail penetration across supermarkets, specialty outlets, and e-commerce platforms. Regulatory clarity through the USDA National Organic Program (NOP), combined with the long-standing credibility of the USDA Organic seal, continues to reinforce consumer trust and support premium pricing. Canada is seeing steady expansion as provincial organic standards align with federal frameworks, while Mexico's rising middle class and growing health awareness are boosting demand for both imported and locally produced organic frozen desserts. The region also remains highly innovation-driven, with brands introducing new certified and specialty offerings that emphasize product differentiation and justify higher price points.

Asia-Pacific is projected to be the fastest-growing region, with a CAGR of 11.59% through 2031, fueled by rising disposable incomes, rapid urbanization, and improving cold-chain logistics. Increasing awareness of food safety and health benefits is accelerating demand across major markets such as China, India, Japan, and Australia. Strategic investments and consolidation activity highlight the region's potential, as multinational players expand their presence through acquisitions and partnerships that combine global branding with local production and distribution capabilities. However, growth is tempered by regulatory fragmentation, as countries maintain distinct organic certification systems, increasing compliance complexity for exporters. Additionally, limited domestic organic dairy supply means many producers rely on imported ingredients, exposing the market to higher costs and currency risks.

Europe remains a significant contributor to the organic ice cream market, supported by stringent regulatory standards, high per-capita organic consumption, and a strong preference for locally sourced and artisanal products. Markets such as Germany, France, Austria, and the Netherlands drive demand, while established certification systems and cross-border regulatory alignment facilitate trade despite post-Brexit complexities affecting the UK. In contrast, South America and the Middle East & Africa are still emerging markets. South America shows long-term promise with improving organic agriculture infrastructure and growing urban demand, though consumption remains concentrated in major cities and constrained by distribution channel. Meanwhile, the Middle East and Africa are characterized by limited organic production and certification systems, with demand largely centered in affluent urban areas and driven by imports. Across these regions, future growth will depend on infrastructure development, regulatory progress, and increasing consumer awareness of organic products.

- Unilever

- Danone

- Oatly Group AB

- Alden's Organic

- Straus Family Creamery

- Cosmic Bliss

- NadaMoo!

- Coconut Bliss

- Jeni's Splendid Ice Creams

- Blue Marble Ice Cream

- Amul

- Graeter's Ice Cream

- Perry's Ice Cream

- Stonyfield Farm

- Three Twins Ice Cream

- Van Leeuwen Ice Cream

- Organic Valley

- Yeo Valley

- Remeo Gelato

- Booja-Booja

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Organic dairy sourcing as a premium trust signal

- 4.2.2 Premiumization and indulgent organic products

- 4.2.3 Flavor innovation using organic inclusions

- 4.2.4 Growth of lactose-free organic dairy variants

- 4.2.5 Strengthening food Safety and organic certification standards

- 4.2.6 Artisanal small-batch organic positioning

- 4.3 Market Restraints

- 4.3.1 High cost of certified organic dairy and ingredients

- 4.3.2 Shorter shelf life due to clean-label formulations

- 4.3.3 Fragmented organic standards across regions

- 4.3.4 Limited organic milk supply

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Ingredient Source

- 5.1.1 Dairy Based

- 5.1.2 Non-dairy Based

- 5.2 By Flavor

- 5.2.1 Vanilla

- 5.2.2 Chocolate

- 5.2.3 Fruit-Flavored

- 5.2.4 Others

- 5.3 By Product Type

- 5.3.1 Pints

- 5.3.2 Cones

- 5.3.3 Bars

- 5.3.4 Others

- 5.4 By Distribution Channel

- 5.4.1 Foodservice

- 5.4.2 Retail

- 5.4.2.1 Supermarkets/Hypermarkets

- 5.4.2.2 Specialty Stores

- 5.4.2.3 Convenience Stores

- 5.4.2.4 Online Retail Stores

- 5.4.2.5 Other Distribution Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 Thailand

- 5.5.3.7 Singapore

- 5.5.3.8 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Unilever

- 6.4.2 Danone

- 6.4.3 Oatly Group AB

- 6.4.4 Alden's Organic

- 6.4.5 Straus Family Creamery

- 6.4.6 Cosmic Bliss

- 6.4.7 NadaMoo!

- 6.4.8 Coconut Bliss

- 6.4.9 Jeni's Splendid Ice Creams

- 6.4.10 Blue Marble Ice Cream

- 6.4.11 Amul

- 6.4.12 Graeter's Ice Cream

- 6.4.13 Perry's Ice Cream

- 6.4.14 Stonyfield Farm

- 6.4.15 Three Twins Ice Cream

- 6.4.16 Van Leeuwen Ice Cream

- 6.4.17 Organic Valley

- 6.4.18 Yeo Valley

- 6.4.19 Remeo Gelato

- 6.4.20 Booja-Booja

7 MARKET OPPORTUNITIES AND FUTURE TRENDS