PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062267

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062267

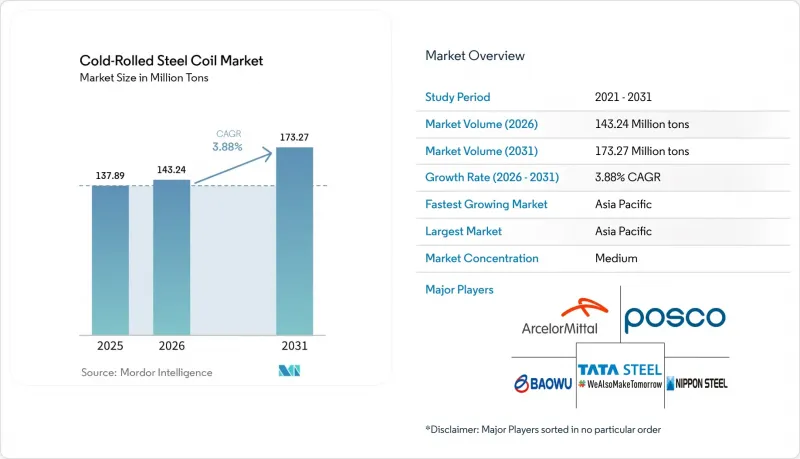

Cold-Rolled Steel Coil - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the cold-Rolled steel coil market size is expected to increase from 137.89 Million tons in 2025 to 143.24 Million tons in 2026 and reach 173.27 Million tons by 2031, growing at a CAGR of 3.88% over 2026-2031.

This report is Segmented by Grade (Low-Carbon Steel, High-Carbon Steel, High-Strength Low-Alloy (HSLA) Steel, and More), Application (Automotive Body and Structural Parts, Consumer Appliances, Industrial Machinery and Equipment, and More), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Global Cold-Rolled Steel Coil Market Trends and Insights

Growing Demand From Automotive And Appliance Industries

Battery-electric-vehicle output reached 14 million units in 2025, each platform consuming 15%-20% more AHSS than its internal-combustion predecessor to offset battery mass and meet crash requirements. SSAB launched EV-optimized AHSS in 2025 with tensile strengths beyond 1,500 MPa, allowing automakers to trim gauge thickness 10%-15% while holding structural integrity. Refrigerator and washing-machine makers in China and India shifted to 0.4-0.5 mm pre-painted coil from traditional 0.6-0.7 mm, reducing material costs up to 12% and cutting energy-label penalties. These twin pulls sustain the cold-rolled steel coil market even where vehicle assembly flattens in mature economies. Mills with tight-tolerance rolling and advanced coating are best placed to capture expanding margins, whereas commodity producers face intensified import competition.

Increasing Use In Construction And Infrastructure Projects

North American building codes adopted cold-formed steel framing for multi-story and seismic applications in 2024-2025, widening addressable demand beyond single-family housing. Data-center construction in Virginia, Texas, and Ireland alone consumed roughly 1.2 million tons of coil in 2025 for framing, HVAC ducting, and cable trays. GCC countries registered an increase in steel-demand growth in 2025, channeling cold-rolled products into solar-farm roofing and desalination cladding. Modular building in Europe and North America adds 300,000-400,000 tons annually but stays price sensitive, exposing suppliers to substitution if steel premiums exceed 20% of framing cost. Regulatory alignment and labor shortages continue to favor cold-formed solutions, supporting the cold-rolled steel coil market trajectory in non-automotive sectors.

Volatile Raw-Material Prices

Iron ore traded between USD 90 and USD 130 per ton in 2025, while U.S. scrap ranged from USD 300 to USD 450 per ton, squeezing margins by 200-300 basis points for producers lacking captive resources. Integrated mills such as Tata Steel or Cleveland-Cliffs cushioned swings through internal transfer pricing, whereas merchant mills faced spot-market exposure. EAF operators benefited during scrap troughs but lost cost edge when scrap rose USD 100 above pig-iron parity. This asymmetry will persist into 2027, complicating price negotiations in the cold-rolled steel coil market.

Other drivers and restraints analyzed in the detailed report include:

- High-Strength And Surface-Finish Advantages Over Hot-Rolled Steel

- Manufacturing Expansion In Emerging Economies

- Energy-Intensive Processing And Carbon Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Low-carbon steel controlled 46.61% of 2025 volume in the cold-rolled steel coil market, yet Advanced High-Strength Steel (AHSS) is forecast to grow at 4.55% to 2031 as OEMs replace conventional grades to meet fleet-average emission targets.

Stainless cold-rolled coil remains a niche but lucrative slice, especially for food equipment and chemical processing, where Outokumpu and SSAB supply low-carbon variants meeting EU ecodesign norms at 40%-60% margin uplifts. High-carbon and HSLA steels trail overall growth as electrification reduces drivetrain steel content. Mills are unable to produce AHSS or specialty stainless risk margin compression within the cold-rolled steel coil market.

Geography Analysis

Asia-Pacific commanded 59.94% of 2025 volume, expanding at 4.36% through 2031 on the back of Indian and Southeast Asian capacity additions and Chinese appliance exports. India alone commissioned 3.5 million tons of new capacity across Tata Steel, JSW Steel, AM/NS India, and Shyam Metalics during 2024-2025 to satisfy domestic demand and EU-bound exports. Vietnam reached 8 million tons capacity in 2025 with delivered costs 10%-15% under Northeast Asian mills.

North America's cold-rolled steel coil market's growth is propelled by EAF investments such as Nucor's 3-million-ton West Virginia mill and Hyundai Steel's USD 5.8 billion U.S. greenfield EAF announced in March 2026. Mexico's 1.5 million-ton Pesqueria complex positions the country as a regional hub under USMCA rules.

Europe faces slower growth given stagnant auto output and high energy costs, yet CBAM incentives are triggering capacity reshoring to Poland, Spain, and Italy. South America's growth is led by Brazilian and Argentine automotive recovery, while the Middle East and Africa will advance on Saudi and UAE infrastructure pipelines, including EMSTEEL's AED 625 million expansion targeting GCC HVAC and construction buyers.

- ArcelorMittal

- China Baowu Steel Group Corporation Limited

- Cleaveland-Cliffs Inc.

- CRS Holdings, LLC.

- Hyundai Steel

- JFE Steel Corporation

- JSW Steel

- Nippon Steel Corporation

- Nucor Corporation

- Outokumpu

- POSCO

- Salzgitter Flachstahl GmbH

- SSAB AB

- Tata Steel

- Thyssenkrupp Steel Europe

- United States Steel Corporation.

- Voestalpine Stahl GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand from Automotive and Appliance Industries

- 4.2.2 Increasing Use in Construction and Infrastructure Projects

- 4.2.3 High-Strength and Surface-Finish Advantages over Hot-Rolled Steel

- 4.2.4 Manufacturing Expansion in Emerging Economies

- 4.2.5 Cold-Formed Steel Framing in Modular and Data-Center Builds

- 4.3 Market Restraints

- 4.3.1 Volatile Raw-Material (Iron-Ore And Scrap) Prices

- 4.3.2 Energy-Intensive Processing and Carbon Dioxide Regulations

- 4.3.3 Aluminium and Composites Substitution in Lightweighting

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Grade

- 5.1.1 Low-Carbon Steel

- 5.1.2 High-Carbon Steel

- 5.1.3 High-Strength Low-Alloy (HSLA) Steel

- 5.1.4 Advanced High-Strength Steel (AHSS)

- 5.1.5 Stainless Steel

- 5.2 By Application

- 5.2.1 Automotive Body and Structural Parts

- 5.2.2 Consumer Appliances

- 5.2.3 Construction (Roofing, Wall Panels, Framing)

- 5.2.4 Industrial Machinery and Equipment

- 5.2.5 Furniture And Storage Systems

- 5.2.6 Packaging (Drums, Barrels, Containers)

- 5.2.7 Electrical And HVAC

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 ArcelorMittal

- 6.4.2 China Baowu Steel Group Corporation Limited

- 6.4.3 Cleaveland-Cliffs Inc.

- 6.4.4 CRS Holdings, LLC.

- 6.4.5 Hyundai Steel

- 6.4.6 JFE Steel Corporation

- 6.4.7 JSW Steel

- 6.4.8 Nippon Steel Corporation

- 6.4.9 Nucor Corporation

- 6.4.10 Outokumpu

- 6.4.11 POSCO

- 6.4.12 Salzgitter Flachstahl GmbH

- 6.4.13 SSAB AB

- 6.4.14 Tata Steel

- 6.4.15 Thyssenkrupp Steel Europe

- 6.4.16 United States Steel Corporation.

- 6.4.17 Voestalpine Stahl GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment