PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062268

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062268

Arbitrary Waveform Generator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

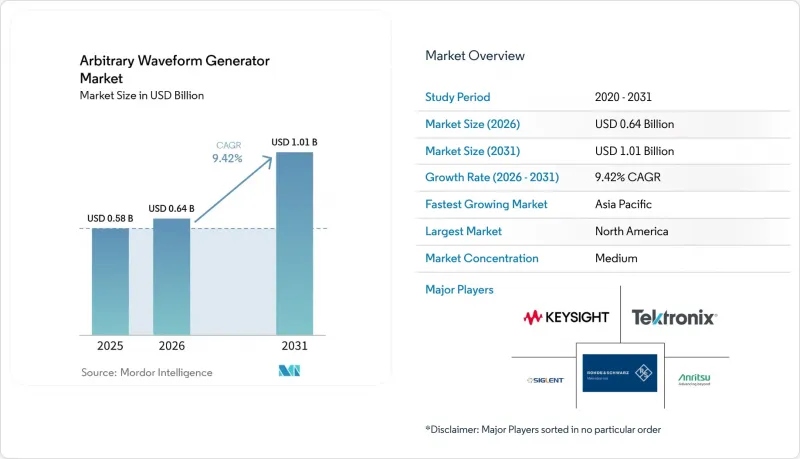

According to Mordor Intelligence, the arbitrary waveform generator market size is expected to grow from USD 0.58 billion in 2025 to USD 0.64 billion in 2026 and is forecast to reach USD 1.01 billion by 2031 at a 9.42% CAGR over 2026-2031.

This report is Segmented by Technology (Direct Digital Synthesis AWG, Variable-Clock AWG, and Combined AWG), Product (Single-Channel, and Dual-Channel), Frequency Range (Up To 1 GHz, 1 GHz To 5 GHz, and Above 5 GHz), End-User Industry (IT and Telecommunications, Aerospace and Defense, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Arbitrary Waveform Generator Market Trends and Insights

Rising Complexity of 5G and 6G RF Signal Testing

6G research prototypes reach carriers near 300 GHz and integrate sensing with communications, forcing test labs to generate terahertz-scale waveforms with sub-picosecond timing accuracy. Field trials in South Korea and Japan confirmed that beam-steering errors under 0.5 degrees at 100 GHz halve link range, so engineers now replicate multipath fading, antenna-array defects, and Doppler shifts inside the arbitrary waveform generator itself rather than external software. The IEEE 802.11be Wi-Fi 7 amendment, ratified in 2024, likewise added 320 MHz channels and 4096-QAM, demanding 80 dB spurious-free dynamic range to avoid masking adjacent-channel leakage. Vendors responded by embedding field-programmable-gate-array impairment engines that let users adjust phase noise or I-Q imbalance on the fly, cutting reload times from minutes to seconds. Activity is concentrated in regions leading 6G spectrum allocation, yet the resulting specification uplift is permeating every major wireless laboratory.

Semiconductor Rapid Prototyping and Automated Test-Equipment Growth

Automated-test spending surged as foundries raced to qualify 3 nm and 2 nm nodes, requiring waveform generators that emulate PCIe 6.0 and USB4 Version 2.0 lanes at 64 GT-s and 80 Gb-s. Taiwan- and South Korea-based fabs installed multi-channel platforms supporting femtosecond-level coherence across 8 or 16 outputs to validate die-to-die chiplet links. Because any delay in delivery stalls billion-dollar product launches, lead times for high-end units stretched beyond six months. North American and European design houses also need short-lived prototypes before committing to tape-out, so demand concentrates in the 0-to-2-year window, underpinning the short-term growth outlook.

Capital Spending Freezes at Mid-Tier Device OEMs

Component inflation and soft consumer demand narrowed margins at many mid-tier manufacturers, prompting 38% of surveyed firms to postpone waveform-generator upgrades planned for 2026. These customers extended legacy-instrument life through firmware patches and third-party calibration, depressing mid-range unit shipments even as high-end backlogs swelled. Vendors now offer leasing and pay-per-use lab access, but data-sovereignty and latency concerns confine uptake to non-critical tasks. The impact should ease within two years once macro visibility improves.

Other drivers and restraints analyzed in the detailed report include:

- Quantum-Computing Demand for Ultra-Channel Pulse Control

- Automotive Radar Systems Migrating Beyond 77 GHz

- Lack of Skilled Operators for Ultra-Fast Gear

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Direct digital synthesis held 55.22% revenue share in 2025, benefiting from deterministic phase control and spurious-free dynamic range beyond 80 dBc, attributes vital for coherent-optical modulation and qubit manipulation. This dominance reinforced the arbitrary waveform generator market size leadership of the segment, yet combined architectures are projected to expand at a 9.10% CAGR because they merge variable-clock agility with RF precision in a single chassis.

Variable-clock models remain relevant where sample-rate flexibility outweighs phase coherence, for example when mimicking irregular sensor outputs or generating pulse-width-modulation signals for power electronics. IEEE 1658 revisions favor direct digital synthesis on dynamic-linearity metrics, but Zurich Instruments' hybrid platform illustrates how vendors can bridge use cases without forcing labs to purchase multiple boxes, protecting adoption across mixed-signal environments.

Dual-channel units captured 60.22% share in 2025 and are forecast to grow at a 10.20% CAGR. Their ability to drive I-Q modulators or dual-polarization photonics transceivers cements their lead, and falling cost premiums encourage even cost-sensitive labs to adopt two outputs. Keysight's flagship 65 GS-s model became the benchmark reference for coherent-optical research, illustrating how a single module can generate four baseband channels for 400 Gb-s links, thereby raising the arbitrary waveform generator market share concentration within high-performance tiers.

Single-channel instruments still serve applications such as clock-jitter injection or university teaching labs, but their relevance erodes as integrated platforms like Liquid Instruments' 4-output device enter the sub-USD 20,000 price band. This democratization broadens adoption yet simultaneously cements dual-channel as the de facto baseline for mainstream RF and photonics validation.

Geography Analysis

In 2025, North America accounted for 36.82% of the revenue, driven by its well-established quantum-computing hubs, robust aerospace procurement activities, and the presence of leading semiconductor design houses. These factors collectively reinforce the region's dominant position in the arbitrary waveform generator market, ensuring its continued leadership. The region's advanced technological infrastructure and strong R&D capabilities further contribute to its market strength.

Meanwhile, the Asia-Pacific region is projected to grow at a notable 10.67% CAGR, fueled by significant investments from countries such as China, South Korea, and Japan. These nations are focusing on developing domestic semiconductor fabrication facilities (fabs) and establishing 6G research clusters, which are expected to drive substantial growth in the region. This strategic focus on innovation and infrastructure development is gradually shifting the center of volume growth toward the east.

Europe maintains a solid foundation in the market, supported by Germany's expertise in automotive radar technologies and the European Union's funding for photonics projects. These initiatives underscore the region's commitment to technological advancement and its ability to sustain a competitive edge. On the other hand, South America and the Middle East, while still in the early stages of market development, are emerging as strategically important regions. They are poised to play a critical role in future applications such as smart-city projects and satellite backhaul systems, which are expected to gain traction in the coming years.

- Keysight Technologies

- Tektronix Inc.

- Rohde & Schwarz GmbH & Co KG

- Tabor Electronics Ltd.

- Active Technologies Srl

- Berkeley Nucleonics Corporation

- Zurich Instruments AG

- National Instruments Corporation

- Siglent Technologies

- B&K Precision Corporation

- Teledyne LeCroy Inc.

- Anritsu Corporation

- Rigol Technologies Co., Ltd.

- Liquid Instruments Pty. Ltd.

- Pico Technology Ltd.

- GW Instek (Good Will Instrument Co., Ltd.)

- Spectrum Instrumentation GmbH

- GaGe (DynamicSignals LLC)

- Yokogawa Electric Corporation

- Stanford Research Systems Inc.

- OPAL-RT Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Complexity of 5G/6G RF Signal Testing

- 4.2.2 High-Resolution DACs Becoming Industry Standard

- 4.2.3 Automotive Radar Systems Shifting Beyond 77 GHz

- 4.2.4 Semiconductor Rapid Prototyping and ATE Growth

- 4.2.5 Quantum Computing Demands Ultra-Channel Pulse Control

- 4.2.6 Adoption of Photonic-Integrated AWGs for Optical I/O

- 4.3 Market Restraints

- 4.3.1 Capital Spending Freezes at Mid-Tier Device OEMs

- 4.3.2 Lack of Skilled Operators for Ultra-Fast Gear

- 4.3.3 Rising Competition from Vector Signal Generators

- 4.3.4 Uncertainty Around Cryogenic IC Development

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value / Supply-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Direct Digital Synthesis AWG

- 5.1.2 Variable-Clock AWG

- 5.1.3 Combined AWG

- 5.2 By Product

- 5.2.1 Single-Channel

- 5.2.2 Dual-Channel

- 5.3 By Frequency Range

- 5.3.1 Up to 1 GHz

- 5.3.2 Above 1 GHz to 5 GHz

- 5.3.3 Above 5 GHz

- 5.4 By End-User Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 Aerospace and Defense

- 5.4.3 Electronics and Semiconductor

- 5.4.4 Automotive

- 5.4.5 Healthcare

- 5.4.6 Education and Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Russia

- 5.5.2.6 Rest of Europe

- 5.5.3 South America

- 5.5.3.1 Brazil

- 5.5.3.2 Argentina

- 5.5.3.3 Rest of South America

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Kuwait

- 5.5.5.4 Bahrain

- 5.5.5.5 Turkey

- 5.5.5.6 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Keysight Technologies

- 6.4.2 Tektronix Inc.

- 6.4.3 Rohde & Schwarz GmbH & Co KG

- 6.4.4 Tabor Electronics Ltd.

- 6.4.5 Active Technologies Srl

- 6.4.6 Berkeley Nucleonics Corporation

- 6.4.7 Zurich Instruments AG

- 6.4.8 National Instruments Corporation

- 6.4.9 Siglent Technologies

- 6.4.10 B&K Precision Corporation

- 6.4.11 Teledyne LeCroy Inc.

- 6.4.12 Anritsu Corporation

- 6.4.13 Rigol Technologies Co., Ltd.

- 6.4.14 Liquid Instruments Pty. Ltd.

- 6.4.15 Pico Technology Ltd.

- 6.4.16 GW Instek (Good Will Instrument Co., Ltd.)

- 6.4.17 Spectrum Instrumentation GmbH

- 6.4.18 GaGe (DynamicSignals LLC)

- 6.4.19 Yokogawa Electric Corporation

- 6.4.20 Stanford Research Systems Inc.

- 6.4.21 OPAL-RT Technologies Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment