PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062274

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062274

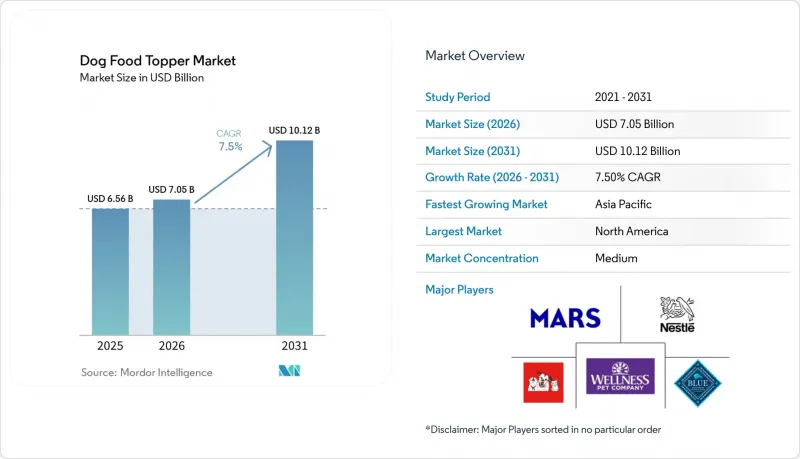

Dog Food Topper - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the dog food topper market size was valued at USD 6.56 billion in 2025 and is estimated to grow from USD 7.05 billion in 2026 to reach USD 10.12 billion by 2031, at a CAGR of 7.5% during the forecast period (2026-2031).

This report is Segmented by Product Type (Freeze-Dried Toppers and More), by Ingredient Source (Animal-Based Protein and More), by Form (Dry/Dehydrated and Liquid/Fresh), by Distribution Channel (Supermarkets and Hypermarkets, and More), by Dog Size (Small Breed and More), and by Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Dog Food Topper Market Trends and Insights

Premiumization of Pet Diets

Pet owners are allocating more resources to premium dog food toppers that prioritize human-grade ingredients, transparency, and functional health benefits, driven by the rising trend of pet humanization. Millennials and Generation Z together represent approximately 57% of pet ownership, playing a significant role in driving demand for high-quality and specialized pet nutrition products. . Brands are focusing on aspects such as product provenance, recyclable packaging, and visible ingredient inclusions to enhance feeding experiences. The willingness to pay a premium stems from the perception of customization while retaining core kibble products. Growth is most rapid in North America and Europe, with a rising trend in the Asia-Pacific region as urban consumers adopt premium human-food-inspired habits.

Surge in Freeze-Dried and Raw-Inspired Formats

Freeze-dried toppers have transitioned from niche treats to mainstream enhancements, offering raw-like nutrition without the need for refrigeration. These toppers appeal to pet owners due to their ability to retain nutrients and provide texture variety, which encourages repeat purchases. Additionally, air-dried hybrid options are gaining traction as they help reduce energy costs during production. The increasing availability of these formats in mass retail stores highlights their growing acceptance among consumers. This trend is significantly contributing to the expansion of the dog food topper market, as more pet owners seek convenient and nutritious meal enhancements for their pets.

Pricing Premium versus Conventional Kibble

The price disparity between premium dog food toppers and conventional kibble remains a significant restraint in the dog food topper market. Toppers are often considerably more expensive than traditional dry kibble, limiting both trial and repeat purchases among cost-sensitive households. According to the American Pet Products Association, U.S. pet food spending surpassed USD 64 billion in 2023, but a large portion of this spending is still directed toward conventional dry food due to its affordability . While toppers are marketed as premium dietary additions for pets, their high cost poses a barrier to broader adoption.

Other drivers and restraints analyzed in the detailed report include:

- Rising Pet Obesity Driving Functional Toppers

- Growing Adoption of Direct-to-Consumer Subscription Models

- Regulatory Uncertainty on Novel Ingredients

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Freeze-dried toppers accounted for the largest 82.5% of the dog food topper market share in 2025, and the market size is projected to achieve the fastest growth with a CAGR of 12.0% from 2026 to 2031. This segment benefits from attributes such as raw-like nutrition, ambient storage, and ease of functional fortification. Hybrid air-dried inclusions offer reduced processing energy requirements and expanded pricing options. Liquid gravies and bone broths' growth is driven by their hydration and joint support benefits, although their reliance on refrigeration limits their market penetration. Powdered seasonings provide a cost-effective entry point but require consumer education on proper reconstitution methods.

Freeze-dried brands are differentiating through protein variety and visible chunks designed to appeal to canine sensory preferences. Examples include West Paw's postbiotic-fortified cubes and Stella and Chewy's raw-coated kibble, reflecting the trend of combining health benefits with enhanced texture. Liquid product lines focus on ingredients such as collagen, glucosamine, and electrolytes, while innovations like bone broth drum-pouch packaging improve shelf visibility. As manufacturers continue to innovate, format selection increasingly emphasizes balancing freshness perception, cost efficiency, and shipping durability, contributing to greater competitive diversity within the dog food topper market.

Animal-based proteins accounted for the largest 71.0% of the dog food topper market share in 2025, while the insect-based proteins market size is anticipated to grow at the fastest CAGR of 14.5% from 2026 to 2031, following the approval of dried mealworm meal in the United States. Key drivers of this growth include rising consumer interest, environmental benefits, and high digestibility. These factors are encouraging experimentation within the market. Meanwhile, plant-based proteins address hypoallergenic needs but require amino acid fortification to meet nutritional standards, limiting their standalone use in dog food toppers.

Ynsect's expansion initiatives in France and Mexico, along with Tyson's investment in Protix, are contributing to increased insect protein availability. Research highlights that black soldier fly larvae have limitations in palatability at higher inclusion levels, guiding blend ratios in formulations. Manufacturers are strategically integrating insect, animal, and plant-based ingredients to achieve a balance between flavor, cost, and sustainability. This strategy addresses consumer preferences while enhancing the resilience of raw material sourcing, ensuring a stable supply and adaptability in the evolving dog food topper market.

Geography Analysis

North America led the market with a 38.0% of the dog food topper market share in 2025, driven by advanced pet humanization trends and higher disposable income levels. Pet owners in the region increasingly treat their pets as family members, leading to a growing demand for premium and specialized dog food toppers. The region is witnessing increased adoption of direct-to-consumer subscriptions and freeze-dried formats, as consumers prioritize convenience, shelf stability, and functional benefits such as enhanced nutrition and digestibility. North America is leading the way in testing fresh and cultivated meat toppers, supported by clear regulations that encourage innovation.

The Asia-Pacific market size is projected to register the fastest CAGR of 11% from 2026 to 2031, fueled by urban millennials in countries like China and Japan who align their pets' diets with personal wellness trends. This demographic is increasingly willing to spend on high-quality, health-focused pet food products, reflecting their own lifestyle choices. The rising adoption of e-commerce platforms has simplified access to dog food toppers, offering a wide range of options to consumers in both urban and rural areas. However, fragmented regulations surrounding insects and cultivated proteins necessitate localized compliance strategies, as brands must navigate varying legal frameworks across countries.

Europe's stringent novel-food regulations are shaping a cautious approach to the introduction of insect-based and cell-based ingredients. These regulations ensure consumer safety but also slow down the pace of innovation in the market. Sustainability labels and organic certifications strongly appeal to consumers, as environmental concerns and ethical considerations increasingly influence purchasing decisions. This has driven demand for low-carbon protein options, such as insect-based and plant-based toppers, which align with the region's focus on reducing environmental impact.

- WellPet LLC

- Mars, Incorporated

- Nestle Purina PetCare Company

- Stella & Chewy's, LLC

- The Honest Kitchen, Inc.

- Blue Buffalo Company, Ltd.

- Primal Pet Foods, Inc.

- Instinct (Nature's Variety)

- Natoo Pet Foods Ltd.

- Freshpet, Inc.

- Open Farm Inc.

- Nulo, Inc.

- Canidae Pet Food Company, LLC

- Diamond Pet Foods, Inc.

- Hill's Pet Nutrition, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Premiumization of pet diets

- 4.2.2 Surge in freeze-dried and raw-inspired formats

- 4.2.3 Rising pet obesity driving functional toppers

- 4.2.4 Growing Adoption of direct-to-consumer subscription models

- 4.2.5 AI-enabled personalized nutrition algorithms

- 4.2.6 Fermentation-derived postbiotic additions for gut health

- 4.3 Market Restraints

- 4.3.1 Pricing premium versus conventional kibble

- 4.3.2 Regulatory uncertainty on novel ingredients

- 4.3.3 Cold-chain cost for fresh/liquid toppers

- 4.3.4 Limited palatability data for insect protein

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Force Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Freeze-Dried Toppers

- 5.1.2 Air-Dried Toppers

- 5.1.3 Wet/Gravy Toppers

- 5.1.4 Bone Broth Toppers

- 5.1.5 Powdered/Seasoning Toppers

- 5.1.6 Functional and Supplement-Infused Toppers

- 5.2 By Ingredient Source

- 5.2.1 Animal-Based Protein

- 5.2.2 Plant-Based Protein

- 5.2.3 Insect-Based Protein

- 5.2.4 Mixed/Hybrid Proteins

- 5.3 By Form

- 5.3.1 Dry/Dehydrated

- 5.3.2 Liquid/Fresh

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets and Hypermarkets

- 5.4.2 Pet Specialty Stores

- 5.4.3 Veterinary Clinics

- 5.4.4 Online Retail and Direct-to-Consumer

- 5.5 By Dog Size

- 5.5.1 Small Breed

- 5.5.2 Medium Breed

- 5.5.3 Large Breed

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.1.4 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 WellPet LLC

- 6.4.2 Mars, Incorporated

- 6.4.3 Nestle Purina PetCare Company

- 6.4.4 Stella & Chewy's, LLC

- 6.4.5 The Honest Kitchen, Inc.

- 6.4.6 Blue Buffalo Company, Ltd.

- 6.4.7 Primal Pet Foods, Inc.

- 6.4.8 Instinct (Nature's Variety)

- 6.4.9 Natoo Pet Foods Ltd.

- 6.4.10 Freshpet, Inc.

- 6.4.11 Open Farm Inc.

- 6.4.12 Nulo, Inc.

- 6.4.13 Canidae Pet Food Company, LLC

- 6.4.14 Diamond Pet Foods, Inc.

- 6.4.15 Hill's Pet Nutrition, Inc.

7 Market Opportunities and Future Outlook