PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062296

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062296

Middle East E-commerce Warehouse - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

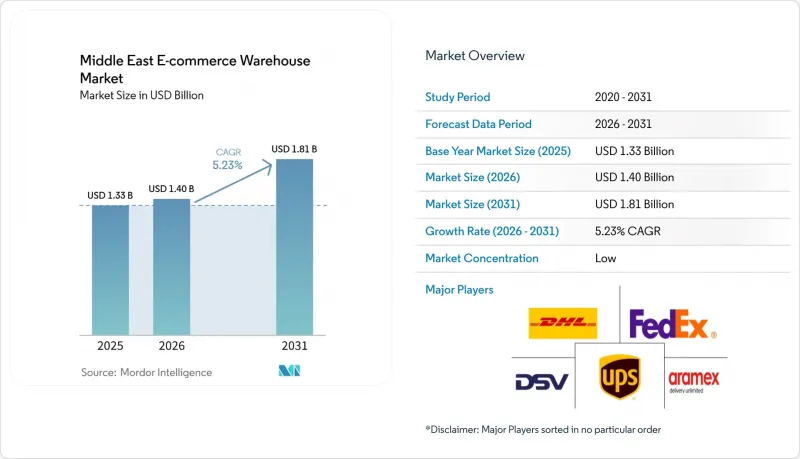

According to Mordor Intelligence, the middle east e-commerce warehousing market size is projected to be USD 1.33 billion in 2025, USD 1.40 billion in 2026, and reach USD 1.81 billion by 2031, growing at a CAGR of 5.23% from 2026 to 2031.

The market is expanding as fast-growing online retail volumes, wider digital-payment adoption, and new cross-border trade agreements shorten fulfillment cycles and push operators to build smarter, better-located facilities. [1] General Authority for Statistics, "Monthly Wholesale and Retail Indices," stats.gov.sa Investments are flowing into temperature-controlled buildings, last-mile dark stores, and AI-enabled inventory systems, while sovereign wealth funds continue to bankroll mega-logistics parks that integrate ports, airports, and free zones. This report is Segmented by Warehouse Type (Fulfilment Centers, Distribution Centers, and More), by Service Type (Storage, Picking & Packing, Value-Added Services), by Automation Level (Manual, Semi-Automated, Automated), by End-User Industry (Apparel & Footwear, Grocery & FMCG, and More), and by Geography (Saudi Arabia, and More). The Market Forecasts are Provided in Terms of Value (USD).

Middle East E-commerce Warehouse Market Trends and Insights

Expanding Digital-Payment Penetration Unlocking Prepaid Fulfillment Capacity

Digital wallets and buy-now-pay-later options have moved cash handling out of the warehouse and onto fintech rails. Prepaid orders reduce working-capital lockups, enable leaner safety stocks, and allow fulfillment teams to promise same-day dispatch without cash-on-delivery reconciliation steps. Lower theft risk and insurance premiums add a cost bonus, and banks' real-time confirmation APIs now trigger warehouse wave picking within minutes of checkout. Faster cash cycles are particularly evident in the UAE, where prepaid penetration already tops 70% of online orders, giving operators room to scale without proportional inventory buildup.

Regional Free-Trade Pacts Shrinking Intra-GCC Customs Cycle Times

The January 2025 expansion of the GCC Integrated Customs Tariff has turned formerly national networks into one regional pool. Harmonized codes and single-window clearance allow a fulfillment center in Riyadh to replenish shoppers in Kuwait or Oman in under 72 hours with no re-declaration paperwork. Saudi Arabia's 50-year tax exemptions inside new Special Integrated Logistics Zones accelerate the hub-and-spoke shift, while Dubai leverages its bonded corridors to keep ports and airports synchronized. Trade friction is falling fastest for high-velocity goods such as smartphones and fast fashion, giving operators new options to stock inventory once and sell it many times across the Gulf.

Scarcity of Grade-A Logistics Land Outside Free-Trade Zones Inflating Lease Premiums

Most modern warehouses sit inside free zones, and land beyond them often lacks height allowances, fire systems, or foreign-ownership clarity. Rents in Dubai's prime corridors rose by double digits in 2025 as supply lagged demand, pushing second-tier operators into outlying plots with weaker road links. Speculative developers are breaking ground, but permitting cycles take years, so capacity tightness will linger. Build-to-suit deals lock in tenants yet require long leases that smaller brands hesitate to sign, keeping market entry tough for new players.

Other drivers and restraints analyzed in the detailed report include:

- Post-Pandemic Shift Toward Online-First Grocery & Pharmacy Replenishment

- Plug-And-Play 4PL Control Towers Enabling SME Cross-Border Scaling

- Volatile Industrial Electricity Tariffs Eroding Cold-Chain Profit Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fulfillment centers accounted for 43.81% of the Middle East e-commerce warehousing market share in 2025, reflecting their role as multi-channel inventory pools that feed line-haul, parcel, and click-and-collect networks. Typically sized 10,000-50,000 m2, they sit on peri-urban land that balances rent with access to ports and highways. Operators outfit them with high-bay racking, mezzanines for value-added services, and WMS integrations that sync with carrier APIs. Demand is steady as merchants shift from single-store rooms to shared third-party sites where they gain scale without owning assets.

Urban dark stores and micro-fulfillment centers post the fastest growth at a 10.68% CAGR through 2031, driven by quick-commerce apps promising 30-minute grocery or pharmacy delivery. These 300-2,000 m2 nodes specialize in top-selling SKUs, use dense tote-based grids, and benefit from AI that predicts neighborhood demand by hour. The Middle East e-commerce warehousing market size for micro-fulfillment is still modest, yet land scarcity inside city limits has sparked creative solutions such as mall basements and rooftop conversions. Kuehne + Nagel's 23,000 m2 site in Dubai's EZDubai zone shows how legacy 3PLs mix large fulfillment halls with adjacent micro hubs to cover both bulk storage and ultrafast delivery.

Storage services generated 50.07% of the Middle East e-commerce warehousing market size in 2025, because e-commerce still rests on safe, climate-controlled inventory holding. Pallet positions, clear height, and fire protection remain the primary leasing criteria for most tenants. However, commoditization keeps margins thin, and operators search for stickier income streams. Value-added services, expanding at a 10.15% CAGR, include kitting, postponement manufacturing, personalized packaging, and photo studios. The Middle East e-commerce warehousing market size linked to such services rises as brands demand local customization to shorten supply chains and comply with language or regulatory labeling rules.

Expeditors' 23,200 m2 Dubai South facility illustrates the shift, offering order management, returns grading, and export documentation under one roof. Brands pay premiums for last-minute localization that enables region-specific launches or seasonal bundles. Picking and packing remain essential, yet automation here, voice-directed headsets, pick-to-light shelves, reduces labor minutes per order, focusing competitive positioning on higher-value assembly or customization tasks instead of basic cartons-in, cartons-out.

List of Companies Covered in this Report:

- Aramex

- DSV (Including DH Schenker)

- DHL Supply Chain

- UPS Supply Chain Solutions

- FedEx Logistics

- Gulf Warehousing Company

- Naqel Express

- RSA Global

- iMile

- J&T Express Middle East

- Wared Logistics

- SAL Saudi Logistics

- Bahri Logistics

- DP World Logistics

- Emirates Logistics

- Etihad Cargo Logistics

- Al-Futtaim Logistics

- AJEX

- GAC

- CMA CGM (Including CEVA Logistics)*

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Digital-Payment Penetration Unlocking Prepaid Fulfillment Capacity

- 4.2.2 Regional Free-Trade Pacts Shrinking Intra-GCC Customs Cycle-Times

- 4.2.3 Post-Pandemic Shift Toward Online-First Grocery & Pharmacy Replenishment

- 4.2.4 Plug-And-Play 4PL Control-Towers Enabling SME Cross-Border Scaling

- 4.2.5 Rapid Rise of Circular-Economy Recommerce Platforms Spurring Dedicated Returns Hubs

- 4.2.6 AI-Driven Inventory-Prediction Engines Justifying High-Throughput Automation

- 4.3 Market Restraints

- 4.3.1 Scarcity of Grade-A Logistics Land Outside Free-Trade Zones Inflating Lease Premiums

- 4.3.2 Volatile Industrial Electricity Tariffs Eroding Cold-Chain Profit Margins

- 4.3.3 ESG Disclosure Mandates Escalating Capex for Solar-Powered & Carbon-Neutral Warehouses

- 4.3.4 Cash-On-Delivery Persistence Complicating Reverse-Logistics Flows & Cash Recovery

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Warehouse Rental Pricing Trends

5 Market Size & Growth Forecasts

- 5.1 By Warehouse Type

- 5.1.1 Fulfilment Centres

- 5.1.2 Distribution Centres (DCs)

- 5.1.3 Cold-Chain Warehouses

- 5.1.4 Dark Stores / Micro-Fulfillment Centers

- 5.1.5 Others (Reverse Logistics Hubs, Bonded Warehouses, Hybrid-use Spaces, etc.)

- 5.2 By Service Type

- 5.2.1 Storage

- 5.2.2 Picking & Packing

- 5.2.3 Value-Added Services and Others (Kitting, Labelling)

- 5.3 By Automation Level

- 5.3.1 Manual

- 5.3.2 Semi-Automated

- 5.3.3 Automated

- 5.4 By End-User Industry

- 5.4.1 Apparel and Footwear

- 5.4.2 Consumer Electronics

- 5.4.3 Grocery and FMCG

- 5.4.4 Pharmaceuticals, Beauty and Wellness

- 5.4.5 Home Essentials and Furnishings

- 5.4.6 Others

- 5.5 By Country (Value)

- 5.5.1 United Arab Emirates

- 5.5.2 Saudi Arabia

- 5.5.3 Qatar

- 5.5.4 Kuwait

- 5.5.5 Bahrain

- 5.5.6 Oman

- 5.5.7 Egypt

- 5.5.8 Rest of Middle East

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Aramex

- 6.4.2 DSV (Including DH Schenker)

- 6.4.3 DHL Supply Chain

- 6.4.4 UPS Supply Chain Solutions

- 6.4.5 FedEx Logistics

- 6.4.6 Gulf Warehousing Company

- 6.4.7 Naqel Express

- 6.4.8 RSA Global

- 6.4.9 iMile

- 6.4.10 J&T Express Middle East

- 6.4.11 Wared Logistics

- 6.4.12 SAL Saudi Logistics

- 6.4.13 Bahri Logistics

- 6.4.14 DP World Logistics

- 6.4.15 Emirates Logistics

- 6.4.16 Etihad Cargo Logistics

- 6.4.17 Al-Futtaim Logistics

- 6.4.18 AJEX

- 6.4.19 GAC

- 6.4.20 CMA CGM (Including CEVA Logistics)*

7 Market Opportunities and Future Outlook