PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062317

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062317

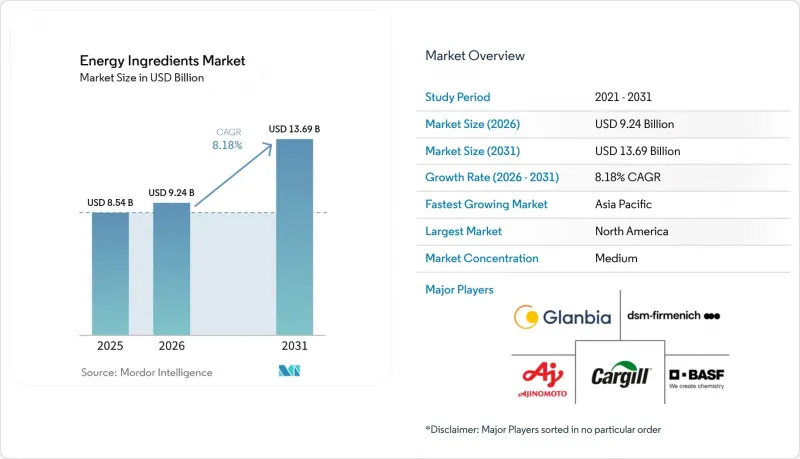

Energy Ingredients - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the energy ingredients market size expanded from USD 8.54 billion in 2025 to USD 9.24 billion in 2026 and is forecast to reach USD 13.69 billion by 2031, advancing at a CAGR of 8.18% over 2026-2031.

This report is Segmented by Ingredient Type (Caffeine, Taurine, Adaptogenic Botanicals, and More), Source (Natural, and Synthetic), Application (Energy Drinks and RTD Beverages, Functional Foods and Snacks, Dietary Supplements, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Energy Ingredients Market Trends and Insights

Rising demand for energy drinks and functional beverages

The increasing consumption of energy drinks and functional beverages is significantly driving growth in the energy ingredients market. Consumers are seeking convenient beverage options that provide quick energy, improved concentration, and enhanced physical performance, particularly in fast-paced urban environments. This has led to rising demand for ready-to-drink energy beverages, fortified coffees, functional teas, and energy shots formulated with ingredients such as caffeine, taurine, guarana, and B-vitamins. Additionally, younger demographics and fitness-oriented consumers are increasingly incorporating these beverages into daily routines to support active lifestyles. Manufacturers are also introducing low-sugar, zero-calorie, and plant-based formulations, which further expands the use of natural energy ingredients. The growing popularity of cold brew coffee, sports drinks, and performance beverages is strengthening product innovation across the category. Wide availability in convenience stores, supermarkets, gyms, and online retail platforms is further accelerating consumption.

Growing focus on physical performance and mental alertness

Growing focus on physical performance and mental alertness is a significant driver of the energy ingredients market, as consumers increasingly prioritize productivity, endurance, and cognitive well-being in their daily lives. Rising academic pressure, demanding work environments, and active lifestyle trends are encouraging greater consumption of products that support sustained energy and improved focus. This has led to strong demand for energy drinks, functional beverages, and dietary supplements containing ingredients such as caffeine, taurine, ginseng, and B-vitamins. Fitness enthusiasts and athletes are also incorporating energy-boosting formulations to enhance workout performance and recovery. Additionally, the growing popularity of gaming and extended screen-time activities has increased demand for cognitive-enhancing energy products. Manufacturers are responding by developing advanced formulations targeting both physical stamina and mental clarity. Clean-label and natural energy ingredients, including adaptogenic botanicals, are further gaining traction among health-conscious consumers. According to research by CBI ministry of foreign affairs, clean-label products are projected to constitute over 70% of portfolios in 2025 and 2026, increasing from 52% in 2021. Overall, the emphasis on improving both physical and mental performance continues to accelerate demand for energy ingredients across multiple end-use sectors.

Stringent regulatory compliance and approval processes

The FDA's decision to potentially eliminate self-affirmed GRAS pathways has significantly tightened the regulatory landscape. Manufacturers must now actively submit detailed safety data and secure FDA notification before introducing new ingredients to the market. Recent FDA data reveals a sharp decline in GRAS approvals, as only a small number of submissions have received "no questions" letters. This trend highlights the FDA's shift towards a more rigorous and thorough review process. Similarly, the European Food Safety Authority (EFSA) has intensified its regulatory oversight. EFSA's recent quarterly approvals have primarily focused on modifying existing authorizations, with fewer approvals granted for new ingredients. These regulatory changes have driven companies to allocate more resources and increase their compliance budgets to meet the heightened requirements. As a result, many manufacturers are strategically targeting markets with clearer and more transparent regulatory frameworks, avoiding the complexities of pursuing simultaneous approvals across multiple global regions.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of sports nutrition and active lifestyle trends

- Increasing adoption of natural and plant-based energy ingredients

- Health concerns related to excessive caffeine and sugar consumption affecting demand

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Caffeine accounted for 48.13% of the ingredient-type segment in 2025, making it the largest contributor to the energy ingredients market. Its dominance is primarily attributed to widespread usage across energy drinks, ready-to-drink coffee, functional beverages, and dietary supplements. Manufacturers prefer caffeine due to its well-established efficacy in improving alertness, enhancing mental focus, and boosting physical performance. The ingredient is also highly versatile, allowing incorporation into multiple product formats such as powders, capsules, shots, and beverages. Additionally, the strong consumer familiarity with caffeine-based products supports continued demand, particularly among working professionals, athletes, and students. The expansion of energy drink brands and RTD coffee consumption across developed and emerging markets further reinforces caffeine's leading position.

Adaptogenic botanicals are projected to register the fastest growth, advancing at a CAGR of 9.84% through 2031. This growth is driven by increasing consumer preference for natural and plant-based energy solutions that offer sustained energy without the crash associated with traditional stimulants. Adaptogens such as ashwagandha, ginseng, rhodiola, and maca are gaining popularity due to their perceived benefits in stress management, endurance enhancement, and cognitive support. Beverage manufacturers are increasingly incorporating these ingredients into functional drinks, herbal energy beverages, and clean-label supplements. The trend toward holistic wellness and preventive health is also accelerating adoption of adaptogenic ingredients among health-conscious consumers. Additionally, demand for low-caffeine and caffeine-free energy formulations is encouraging brands to explore botanical alternatives.

Geography Analysis

North America retained a 33.86% share of the energy ingredients market in 2025, making it the largest regional segment. The region's dominance is supported by strong consumption of energy drinks, ready-to-drink beverages, and dietary supplements across the United States and Canada. High consumer awareness regarding functional ingredients such as caffeine, taurine, and B-vitamins has encouraged widespread adoption across beverage and nutrition products. Additionally, the presence of leading energy drink manufacturers and ingredient suppliers contributes to continuous product innovation and formulation advancements. The growing demand for performance-enhancing beverages among athletes, fitness enthusiasts, and working professionals further strengthens market growth. Expansion of clean-label and sugar-free energy products also supports sustained demand in the region.

Asia-Pacific is projected to register the fastest growth, expanding at a CAGR of 9.73% during the forecast period. This rapid growth is driven by rising urbanization, increasing disposable income, and growing demand for functional beverages across countries such as China, India, Japan, and South Korea. Consumers in the region are increasingly shifting toward energy drinks, RTD teas, and fortified beverages to support busy lifestyles. Additionally, the expanding youth population and growing fitness awareness are accelerating adoption of energy ingredients in sports nutrition and functional foods. Local manufacturers are introducing region-specific flavors and herbal energy formulations, further driving market penetration. The increasing popularity of plant-based and adaptogenic ingredients is also contributing to strong growth in Asia-Pacific.

Europe represents a mature but steadily growing market, supported by demand for clean-label energy beverages and functional nutrition products. Consumers in countries such as Germany, the United Kingdom, and France are increasingly preferring natural energy ingredients and reduced-sugar formulations. South America is witnessing moderate growth, driven by rising energy drink consumption and increasing availability of affordable RTD beverages, particularly in Brazil and Mexico. Meanwhile, the Middle East and Africa region is experiencing gradual expansion due to growing urban populations, rising tourism, and increasing demand for convenient energy drinks.

- Cargill, Incorporated

- DSM-Firmenich AG

- Glanbia plc

- Ajinomoto Co., Inc.

- BASF SE

- Archer Daniels Midland Company

- Kerry Group plc

- Ingredion Incorporated

- Tate & Lyle PLC

- Roquette Freres

- Givaudan SA

- Lonza Group AG

- Balchem Corporation

- Corbion N.V.

- AAK AB

- Nexira SAS

- FrieslandCampina Ingredients

- Associated British Foods plc

- IFF (International Flavors & Fragrances Inc.)

- Prinova Group LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for energy drinks and functional beverages

- 4.2.2 Growing focus on physical performance and mental alertness

- 4.2.3 Expansion of sports nutrition and active lifestyle trends

- 4.2.4 Increasing adoption of natural and plant-based energy ingredients

- 4.2.5 Surging consumption among young consumers and professionals

- 4.2.6 Product innovation including sugar-free formulations

- 4.3 Market Restraints

- 4.3.1 Stringent regulatory compliance and approval processes

- 4.3.2 Health concerns related to excessive caffeine and sugar consumption affecting demand

- 4.3.3 Shift toward low-stimulant or non-caffeinated alternatives limiting growth

- 4.3.4 Supply chain disruptions and price volatility affecting profitability

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Ingredient Type

- 5.1.1 Caffeine

- 5.1.2 Taurine

- 5.1.3 Adaptogenic Botanicals

- 5.1.4 Amino Acids

- 5.1.5 Others

- 5.2 By Source

- 5.2.1 Natural

- 5.2.2 Synthetic

- 5.3 By Application

- 5.3.1 Energy Drinks and RTD Beverages

- 5.3.2 Functional Foods and Snacks

- 5.3.3 Dietary Supplements

- 5.3.4 Sports Nutrition Products

- 5.3.5 Pharmaceutical and Clinical Nutrition

- 5.3.6 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Italy

- 5.4.2.4 France

- 5.4.2.5 Spain

- 5.4.2.6 Netherlands

- 5.4.2.7 Poland

- 5.4.2.8 Belgium

- 5.4.2.9 Sweden

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Indonesia

- 5.4.3.6 South Korea

- 5.4.3.7 Thailand

- 5.4.3.8 Singapore

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Chile

- 5.4.4.5 Peru

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 Morocco

- 5.4.5.7 Turkey

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cargill, Incorporated

- 6.4.2 DSM-Firmenich AG

- 6.4.3 Glanbia plc

- 6.4.4 Ajinomoto Co., Inc.

- 6.4.5 BASF SE

- 6.4.6 Archer Daniels Midland Company

- 6.4.7 Kerry Group plc

- 6.4.8 Ingredion Incorporated

- 6.4.9 Tate & Lyle PLC

- 6.4.10 Roquette Freres

- 6.4.11 Givaudan SA

- 6.4.12 Lonza Group AG

- 6.4.13 Balchem Corporation

- 6.4.14 Corbion N.V.

- 6.4.15 AAK AB

- 6.4.16 Nexira SAS

- 6.4.17 FrieslandCampina Ingredients

- 6.4.18 Associated British Foods plc

- 6.4.19 IFF (International Flavors & Fragrances Inc.)

- 6.4.20 Prinova Group LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK