PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062332

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062332

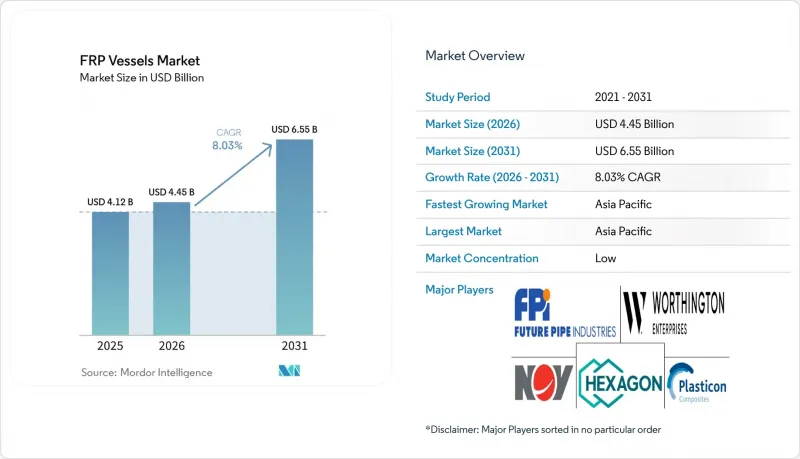

FRP Vessels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the fRP vessels market size is projected to be USD 4.12 billion in 2025, USD 4.45 billion in 2026, and reach USD 6.55 billion by 2031, growing at a CAGR of 8.03% from 2026 to 2031.

This report is Segmented by Vessel Type (Tanks, Columns, and More), Pressure Classification (Low Pressure (<=10 Bar), and More), Fiber Type (Glass Fiber, Carbon Fiber, and More), Application (Water and Wastewater Treatment, Power and Energy, and More), End-User Industry (Industrial and Chemical, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Value (USD).

Global FRP Vessels Market Trends and Insights

Adoption of Lightweight, Corrosion-Resistant Materials

FRP vessels reduce weight by approximately 70% compared to steel, easing transport and lowering foundation loads in retrofits. Offshore platforms and marine desalination sites prefer composites to eliminate galvanic corrosion, extending service life beyond 30 years without coatings. Chemical plants integrate dual-laminate designs for acids and alkalis, avoiding liner delamination seen in steel. Encore Arabia supplied such tanks to the Saudi Water Conversion Corporation in 2025, reinforcing FRP's viability in high-temperature seawater service. The lifetime-cost advantage outweighs higher upfront prices in harsh operating environments.

Rising Demand from Water and Wastewater Utilities

North American municipalities accelerated steel-to-FRP replacements in 2024-2025 after corrosion failures, with the Zone 7 Water Agency and the Florida Governmental Utility Authority citing lower maintenance and NSF/ANSI 61 compliance. First Line's 3,019-unit order for Qinghai lithium projects shows cross-sector pull between industrial water and mining. India's prefabricated sewage systems increasingly specify FRP for chloride-rich waste streams, leveraging modular moving-bed biofilm designs for rapid installation. Deferred maintenance backlogs now fuel a multiyear procurement wave.

High Initial CAPEX and Installation Costs

Composite vessels cost 1.5-to-2.5X steel alternatives, deterring budget-constrained utilities despite lower lifecycle totals. Large-diameter winders exceed USD 500,000, and specialized lifting gear adds another 10-15% to the delivered price. Retrofit sites may need foundation upgrades due to altered load paths, inflating civil budgets. Familiarity bias also steers buyers toward steel even after corrosion failures shorten tank life.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Chemical and Petrochemical Processing Capacity

- Growth in Renewable Energy and Desalination Projects

- Limited Recyclability and End-of-Life Pathways

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tanks accounted for 41.76% of the 2025 revenue, maintaining their dominance in the FRP vessels market due to their extensive use in water treatment and chemical storage. Reactors are projected to grow at a CAGR of 8.69% through 2031, driven by their reliability in handling chemical and thermal stress in process industries. Hybrid tank-reactor designs, incorporating mixers and jackets, are redefining traditional categories, while sanitary fermenters for food and biotech applications contribute to additional market demand.

Process plants increasingly specify ASME RTP-1 or BPE-compliant reactors to avoid pitting issues associated with stainless steel. Pharmaceutical manufacturers are adopting 1,000-20,000 L filament-wound vessels for their smooth inner surfaces, which facilitate CIP operations. Food processors are utilizing FRP fermenters for products like soy sauce and vinegar, while hydrogen mobility is driving the adoption of spherical cylinder bundles in fleet depots. The FRP vessels market continues to emphasize application-specific engineering over standardized solutions.

Medium pressure vessels (10-250 bar) contributed 46.01% of the 2025 revenue, dominating the FRP vessels market across industrial gases and municipal networks. High pressure vessels (>=250 bar) are expected to grow at a CAGR of 8.92% through 2031, driven by demand for 350-bar logistics and 700-bar mobility cylinders.

The ASME RTP-1:2023 standard governs sub-1 bar vessels, while UN R134, TPED, and ISO 14692 regulate high pressure hydrogen applications, leading to increased testing costs. The Welding Research Council's 2025 Bulletin 601 provides guidance for in-service inspections, addressing owner concerns. While code convergence remains a challenge, progress is being made through collaborative working groups.

Geography Analysis

Asia-Pacific captured 44.89% of the 2025 revenue and is projected to grow at a CAGR of 9.18% through 2031, supported by China's 600-unit-per-day RO vessel production facility and India's water renewal programs. South Korea's goal of deploying 6.2 million fuel-cell vehicles by 2040 sustains demand for high pressure cylinders, while ASEAN countries adopt FRP for palm-oil and aquaculture facilities. Government subsidies and local fiber supply chains help maintain low production costs, reinforcing the region's dominance.

North America benefits from steel infrastructure replacements and shale-gas water handling. Zone 7 and Florida authorities installed FRP potable-water tanks in 2025, reporting reduced maintenance costs. Hexagon Purus increased its Maryland production capacity to 10,000 cylinders annually, while Canada's oil sands adopted FRP for tailings water management. The U.S. Inflation Reduction Act's hydrogen credits are supporting the establishment of new high pressure vessel plants.

Europe blends strict circular-economy regulations with hydrogen development initiatives. The EU Clean Hydrogen Partnership funds R&D, and German facilities produce 40,000 cylinders annually. Southern Europe and North Africa are opting for FRP housings in desalination pipelines to prevent seawater corrosion. The Middle-East relies on composites for large-scale desalination and petrochemical projects, with Saudi Aramco partnering with Future Pipe Industries to localize supply. Latin America is showing early momentum with Mexico's hydrogen-cylinder order and Brazil's chemical expansions, though its capacity lags behind Asia-Pacific.

- Aquanomics Systems Limited

- Creative Composites Group

- EPP Composites Pvt Ltd.

- Fiber Tech Composite Pvt. Ltd.

- Fibro Plastichem

- Future Pipe Industries

- Hengshui Jiubo Composites Co., Ltd.

- Hexagon Composites ASA

- International Fiberglass LLC

- Jiangsu Jiuding New Material Co., Ltd.

- Mitsubishi Chemical Infratec Co., Ltd.

- NOV

- Plasticon

- RPS Composites

- Shalin Composites (India) Private Ltd.

- Worthington Enterprises

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption of lightweight, corrosion-resistant materials

- 4.2.2 Rising demand from water and wastewater utilities

- 4.2.3 Expansion of chemical and petrochemical processing capacity

- 4.2.4 Growth in renewable-energy and desalination projects

- 4.2.5 Rapid hydrogen storage roll-out for fuel-cell mobility

- 4.2.6 National green-hydrogen mandates unlocking long-run captive demand

- 4.3 Market Restraints

- 4.3.1 High initial CAPEX and installation costs

- 4.3.2 Limited recyclability and end-of-life pathways

- 4.3.3 Skilled-labour shortages in large-diameter filament winding

- 4.3.4 Inconsistent global codes and standards for FRP pressure vessels

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Vessel Type

- 5.1.1 Tanks

- 5.1.2 Columns

- 5.1.3 Pipes

- 5.1.4 Reactors

- 5.1.5 Spherical Bundles (Type-IV H2 storage)

- 5.2 By Pressure Classification

- 5.2.1 Low Pressure (<=10 bar)

- 5.2.2 Medium Pressure (10-250 bar)

- 5.2.3 High Pressure (>=250 bar)

- 5.3 By Fiber Type

- 5.3.1 Glass Fiber

- 5.3.2 Carbon Fiber

- 5.3.3 Aramid Fiber

- 5.3.4 Hybrid Fiber (Glass-Carbon/Glass-Basalt)

- 5.4 By Application

- 5.4.1 Water and Wastewater Treatment

- 5.4.2 Chemical Processing and Storage

- 5.4.3 Oil, Gas and Petrochemical Upstream

- 5.4.4 Food and Beverage Processing

- 5.4.5 Power Generation and Desalination

- 5.4.6 Hydrogen and Alternative-Fuels Storage

- 5.4.7 Pharmaceutical and Biotech Fluids

- 5.5 By End-user Industry

- 5.5.1 Industrial and Chemical

- 5.5.2 Oil, Gas and Petrochemicals

- 5.5.3 Municipal and Private Water Utilities

- 5.5.4 Power and Energy

- 5.5.5 Food and Beverage

- 5.5.6 Other End-user Industries (Pulp and Paper, Mining, Pharma)

- 5.6 By Geography

- 5.6.1 Asia-Pacific

- 5.6.1.1 China

- 5.6.1.2 Japan

- 5.6.1.3 India

- 5.6.1.4 South Korea

- 5.6.1.5 ASEAN Countries

- 5.6.1.6 Rest of Asia-Pacific

- 5.6.2 North America

- 5.6.2.1 United States

- 5.6.2.2 Canada

- 5.6.2.3 Mexico

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle-East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle-East and Africa

- 5.6.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Aquanomics Systems Limited

- 6.4.2 Creative Composites Group

- 6.4.3 EPP Composites Pvt Ltd.

- 6.4.4 Fiber Tech Composite Pvt. Ltd.

- 6.4.5 Fibro Plastichem

- 6.4.6 Future Pipe Industries

- 6.4.7 Hengshui Jiubo Composites Co., Ltd.

- 6.4.8 Hexagon Composites ASA

- 6.4.9 International Fiberglass LLC

- 6.4.10 Jiangsu Jiuding New Material Co., Ltd.

- 6.4.11 Mitsubishi Chemical Infratec Co., Ltd.

- 6.4.12 NOV

- 6.4.13 Plasticon

- 6.4.14 RPS Composites

- 6.4.15 Shalin Composites (India) Private Ltd.

- 6.4.16 Worthington Enterprises

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment