PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062336

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062336

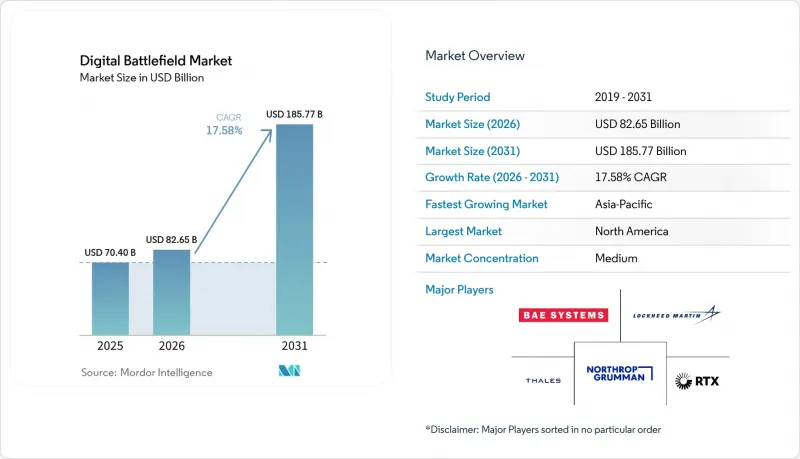

Digital Battlefield - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the digital battlefield market was valued at USD 70.40 billion in 2025 and is projected to grow from USD 82.65 billion in 2026 to USD 185.77 billion by 2031, at a 17.58% CAGR from 2026 to 2031.

This report is Segmented by Platform (Land, Air, Naval, and Space), Component (Hardware, Software, and Services), Technology (Artificial Intelligence (AI) and Big-Data Analytics, and More), Application (Warfare Platforms, and More), End-User (Army, Navy, and Air Force), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Digital Battlefield Market Trends and Insights

Growing Military Adoption of IoT-Enabled Sensors and Devices

The digital battlefield market is gaining from a steady rise in sensor density at the tactical edge. Peer-reviewed research in Discover Internet of Things shows that military IoT deployments depend on solving interoperability, energy management, security, and network resilience simultaneously, which is pushing procurement toward more specialized battlefield hardware and secure onboarding models as a denser sensor mesh improves the common operating picture and shortens the time between detection and response without requiring a full redesign of every command post. The US DoD reinforced this direction through its July 2025 zero-trust memorandum, which explicitly extends compliance expectations to IoT and edge devices and gives buyers a clearer baseline for vendor qualification. As these security and interoperability rules become clearer, the digital battlefield market is benefiting from lower deployment friction for wearables, sensors, and connected battlefield nodes. The result is a procurement cycle that increasingly treats tactical connectivity and sensor ingestion as core mission capabilities rather than as a support layer.

Rising Defense Budgets for Network-Centric Warfare Capabilities

The digital battlefield market is also supported by a broader rearmament cycle that is shifting budgets toward network-centric warfare and data-linked operations. In the US, congressional defense materials for FY2026 show large allocations for C4I, space systems, missile warning, and related digital capabilities, confirming that battlefield digitization is embedded in mainstream defense planning rather than in experimental lines. Japan is moving in the same direction with its FY2026 budget request, where cross-domain operational capability and stand-off defense remain central themes. France also moved to strengthen its military digital base through a new defense digital authority and additional public support for cyber and digital resilience, indicating that European programs are becoming more centralized and faster to execute. These shifts are important because the digital battlefield market now sits closer to cloud infrastructure, data management, and secure software operations than to traditional stand-alone equipment replacement. That is gradually expanding the set of relevant suppliers beyond defense hardware firms alone.

Cybersecurity Vulnerabilities and Data-Breach Risks

The digital battlefield market carries a wider attack surface as more devices, radios, sensors, and edge processors are connected to shared mission networks. France's National Cybersecurity Strategy for 2026 to 2030 also raised reporting and resilience expectations, which signals higher compliance obligations for contractors operating across allied defense programs. These pressures can slow procurement in the digital battlefield market because buyers increasingly require secure update paths, stronger auditability, and more evidence of system hardening before wider deployment. The result is not a collapse in demand, but a longer and more expensive path from demonstration to field use.

Other drivers and restraints analyzed in the detailed report include:

- Advances in AI and Big-Data Analytics for Real-Time Decision-Making

- Expansion of 5G/SATCOM Networks for Resilient Connectivity

- Ethical-Legal Concerns Over Autonomous Lethal Decision-Making

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Land platforms held 43.35% of the market in 2025, maintaining their position as the largest platform group on the digital battlefield. This position reflects the large installed base of soldier systems, vehicle command nodes, battlefield radios, and ground sensing equipment already embedded in force structures. Land remains central because army formations still account for the broadest operational demand across command, logistics, ISR, and tactical communications. Even so, the platform mix is starting to widen as air, naval, and space programs absorb a larger part of new digital spending.

The faster shift is visible in space, where the segment is projected to grow at a 19.66% CAGR through 2031. The US defense materials for FY2026 included USD 34 billion in space procurement and R&D. This part of the digital battlefield market is driven by the need for low-latency relaying, resilient sensing, and theater-wide connectivity that ground networks alone cannot provide. A growing share of defense planning now treats space assets as an operational data transport layer rather than as a remote support function. That shift should keep diluting the relative weight of legacy, ground-heavy spending, even as land remains the largest installed base.

Hardware accounted for 48.67% of component value in 2025, which made it the largest component group in the digital battlefield market. That lead is still supported by radios, computing modules, sensors, displays, and mission equipment that must be fielded at scale. Hardware also remains essential because open architecture still depends on compatible physical nodes that can host software, transport data, and survive military operating conditions. Even so, the greatest change in buying behavior is occurring outside of one-time equipment delivery.

Services are forecast to grow at a 20.43% CAGR through 2031, making it the fastest-growing component of the digital battlefield market, reflecting a clear move toward managed support, data-layer maintenance, cyber compliance, software maintenance, and ongoing model updates throughout a program's life. Lockheed Martin's NGC2 work has shown how iterative development and recurring field feedback are becoming part of routine delivery rather than a separate prototype phase. The same pattern appears in General Dynamics Information Technology's USD 988 million Navy C5ISR support award, where long-duration support carries much of the value rather than a narrow hardware shipment. In practical terms, the digital battlefield industry is becoming increasingly dependent on recurring service contracts to maintain mission readiness after hardware is fielded.

Geography Analysis

North America accounted for 32.78% of the global market value in 2025, maintaining its position as the largest regional block in the digital battlefield market. The region benefits from the scale of US defense spending, a dense contractor base, and procurement frameworks that shape allied procurement behavior. Congressional defense materials for FY2026 show the depth of US spending across C4I, space, and missile warning functions, which supports continuing program momentum. The region also sets important vendor standards through zero-trust and private 5G security frameworks that influence qualification beyond the United States.

Asia-Pacific is projected to expand at a 18.39% CAGR through 2031, making it the fastest-growing region in the digital battlefield market. Growth is being supported by large digitization programs across China, India, Japan, and South Korea, with demand spanning AI-enabled command tools, secure communications, cyber cooperation, and networked operations. Japan's FY2026 defense budget request continued to emphasize cross-domain capabilities and stand-off digital connectivity, reinforcing the view that regional military planning is moving toward more integrated battlefield systems. India and South Korea also expanded their defense technology cooperation in 2026 through a joint strategic vision that covered cyber, innovation, and advanced technology areas relevant to connected operations.

Europe, the Middle East, and Africa remain important growth corridors for the digital battlefield market. Europe is moving faster on defense digitization through greater centralized digital authority and a stronger focus on interoperability across allied programs. The UK's Babel Fish exercise with Lockheed Martin Skunk Works in April 2026 showed practical progress in sharing F-35 data with ground-effector command networks, which is critical for coalition operations. South America remains the smallest regional segment, where spending is more concentrated in border surveillance and maritime ISR than in full-scale digital transformation.

- Lockheed Martin Corporation

- RTX Corporation

- Northrop Grumman Corporation

- BAE Systems plc

- Thales Group

- L3Harris Technologies, Inc.

- General Dynamics Corporation

- Saab AB

- Rafael Advanced Defense Systems Ltd.

- Elbit Systems Ltd.

- Leonardo S.p.A.

- Airbus SE

- Israel Aerospace Industries Ltd.

- Indra Sistemas, S.A.

- CACI International Inc.

- QinetiQ Group

- Honeywell International Inc.

- Rohde & Schwarz GmbH & Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advances in AI and big-data analytics for real-time decision-making

- 4.2.2 Growing military adoption of IoT-enabled sensors and devices

- 4.2.3 Rising defense budgets for network-centric warfare (NCW) capabilities

- 4.2.4 Expansion of 5G/SATCOM networks for resilient connectivity

- 4.2.5 Adoption of digital twin tech for combat-scenario simulation

- 4.2.6 Demand for energy-autonomous edge devices to cut logistical burden

- 4.3 Market Restraints

- 4.3.1 Cybersecurity vulnerabilities and data-breach risks

- 4.3.2 Interoperability hurdles with legacy C4ISR systems

- 4.3.3 Ethical-legal concerns over autonomous lethal decision-making

- 4.3.4 Supply-chain shortages of radiation-hardened semiconductors

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform

- 5.1.1 Land

- 5.1.2 Air

- 5.1.3 Naval

- 5.1.4 Space

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By Technology

- 5.3.1 Artificial Intelligence (AI) and Big-Data Analytics

- 5.3.2 Internet of Things (IoT) and Edge Computing

- 5.3.3 5G/SATCOM Connectivity

- 5.3.4 Augmented Reality (AR) and Virtual Reality (VR)

- 5.3.5 Digital Twin and Simulation

- 5.4 By Application

- 5.4.1 Warfare Platforms

- 5.4.2 Situational Awareness and ISR

- 5.4.3 Command and Control (C2)

- 5.4.4 Logistics and Fleet Management

- 5.5 By End-User

- 5.5.1 Army

- 5.5.2 Navy

- 5.5.3 Air Force

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 France

- 5.6.2.3 Germany

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Israel

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Lockheed Martin Corporation

- 6.4.2 RTX Corporation

- 6.4.3 Northrop Grumman Corporation

- 6.4.4 BAE Systems plc

- 6.4.5 Thales Group

- 6.4.6 L3Harris Technologies, Inc.

- 6.4.7 General Dynamics Corporation

- 6.4.8 Saab AB

- 6.4.9 Rafael Advanced Defense Systems Ltd.

- 6.4.10 Elbit Systems Ltd.

- 6.4.11 Leonardo S.p.A.

- 6.4.12 Airbus SE

- 6.4.13 Israel Aerospace Industries Ltd.

- 6.4.14 Indra Sistemas, S.A.

- 6.4.15 CACI International Inc.

- 6.4.16 QinetiQ Group

- 6.4.17 Honeywell International Inc.

- 6.4.18 Rohde & Schwarz GmbH & Co. KG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment