PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062345

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062345

NVH Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

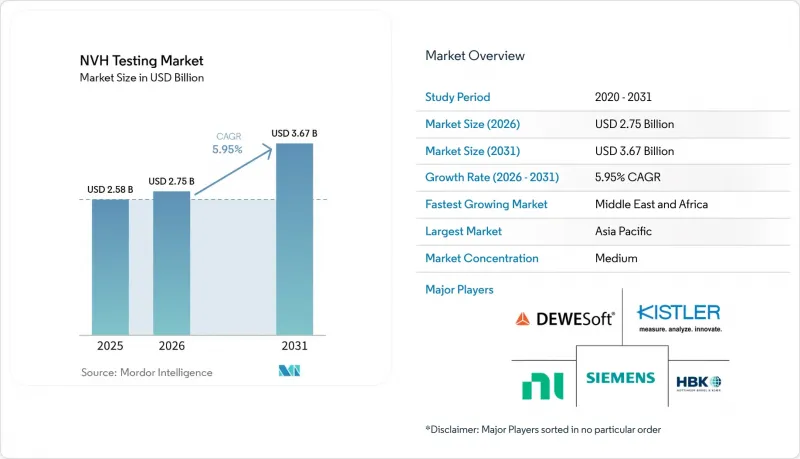

According to Mordor Intelligence, the nVH testing market size is projected to expand from USD 2.58 billion in 2025 and USD 2.75 billion in 2026 to USD 3.67 billion by 2031, registering a CAGR of 5.95% between 2026 and 2031.

This report is Segmented by Component (Hardware, Software, and Services), Testing Type (Modal Testing, Pass-By Noise Testing, Environmental-Chamber NVH, and More), End-Use Industry (Automotive, Aerospace and Defense, Industrial Machinery, Consumer Electronics, and More), Application (Powertrain, Interior Cabin, Exterior Noise, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global NVH Testing Market Trends and Insights

Electrified-Powertrain NVH Requirements

Battery-electric and plug-in hybrid models expose inverter pulse-width-modulation tones, gear-mesh whine, and tire-road interaction once masked by combustion engines, steering programs toward order-tracking analysis and psychoacoustic annoyance metrics between 1 kHz and 10 kHz. Luxury automakers saw customer NVH complaints rise to 78% of total quality issues in 2025, prompting validation budgets to climb by one-third. The European Automotive Research Partners Association has published methodologies that separate structure-borne and airborne paths, while UNECE R138 mandates sound-pressure levels of 56 dB(A) to 75 dB(A) below 20 km/h, merging customer comfort and pedestrian-safety objectives into a single compliance stream. As a result, electrified-powertrain NVH remains the primary catalyst for incremental test-bench hours through 2031.

Miniaturized MEMS Sensor Cost Declines

Unit prices for MEMS accelerometers and microphones fell roughly 15% year-on-year between 2024 and 2025, enabling 64- and 128-channel arrays that democratize operational modal analysis for mid-tier suppliers. DewesoftX 2026.1 introduced native Ethernet-linked MEMS support with sub-microsecond synchronization, and National Instruments' FieldDAQ FD-11634 extended ruggedized coverage to outdoor rocket-test scenarios. Lower acquisition cost also opens the door to continuous condition-based monitoring that can cut unplanned downtime by up to 40 % in manufacturing plants, making sensor affordability a short-cycle demand accelerator.

Shortage of Skilled NVH Engineers

CohanHR's 2025 workforce audit revealed a deficit of 120,000 to 150,000 NVH professionals, with China carrying roughly 50,000 to 60,000 unfilled roles. Ninety-five percent of postings require CAE fluency, yet few university curricula integrate Actran, MSC Nastran, or AVL EXCITE, forcing employers to extend hiring lead times by 6-12 months. Competition from artificial-intelligence roles siphons talent, while hands-on test-cell skills remain irreplaceable, delaying product launches and inflating external consulting spend.

Other drivers and restraints analyzed in the detailed report include:

- Stricter UNECE Exterior-Noise Rules

- Predictive-Maintenance Adoption in Industry 4.0

- High Capex for Modular Hemi-Anechoic Chambers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software claimed the fastest growth rate at a 6.83% CAGR, even though hardware held 42.19% of the NVH testing market share in 2025. Artificial-intelligence modules in Actran, AVL X-ion, and Siemens Simcenter TestLab automate transfer-path analysis and reduce post-processing labor by up to 70%, shrinking design loops and increasing license renewals. Services from HEAD acoustics and NVH Consulting LLC offset the talent shortfall by bundling turnkey validation, while cloud subscriptions blur hardware-software boundaries and commoditize front-end data acquisition.

Hardware remains irreplaceable for precision capture, so Kistler's March 2026 jBEAM Lab satellite test update and Dewesoft's MEMS-enabled platforms underline the hybrid future. As subscription models spread, vendors will tie analytics portals to sensor ecosystems, reinforcing switching costs and nudging procurement from capital expenditure toward operating expenditure, a shift that will further influence the NVH testing market size beyond 2031.

Powertrain NVH retained 29.06% of 2025 sales, yet environmental-chamber NVH is outpacing the total NVH testing market, with a 6.55% run rate, as UNECE limits tighten temperature-dependent pass-by certification. Modal testing, supported by Polytec's laser vibrometers, identifies lightweight-composite resonance in urban air-mobility airframes, while operational testing addresses regenerative-braking transients invisible to static rigs.

Ricardo's upgraded 344 kW dynamometer underscores the need for higher-torque electric-vehicle benchmarking, and Europe's QuieterRail project extends climate-controlled demand into high-speed rail. The widening application range means environmental chambers will narrow the revenue gap with powertrain benches by decade-end, reshaping NVH testing market share allocations across service catalogs.

Geography Analysis

Asia-Pacific accounted for 38.33% of 2025 revenue, as China produced 30% of the world's vehicles and Japan advanced modular chamber installations. Government subsidies for domestic electric-vehicle makers translate into brisk lab utilization, while India's Ecotone Systems expands turnkey chamber capacity to serve Tier-2 suppliers. A dense supplier base, broad manufacturing scale, and rising battery-electric penetration give the region structural advantages that will secure its leading NVH testing market share well past 2031.

Europe remains a regulatory bellwether: UNECE R51-03, ISO 362 updates, and TUV AUSTRIA's Bad Sobernheim track compel manufacturers to invest in local pass-by infrastructure. Hyundai's EUR 150 million Russelsheim campus spotlights premium-brand commitment, and EU-funded rail noise mitigation adds non-automotive volume. Continuous rule tightening keeps Europe's CAGR above the global mean even as its absolute NVH testing market size trails Asia-Pacific's larger base.

North America leverages near-shoring, channeling vehicle programs to Mexico and the U.S. Southeast, prompting AVL and HBK to expand their service offerings. Middle East infrastructure projects in Saudi Arabia and the United Arab Emirates yield the fastest 6.95% CAGR by embedding ISO 20816 vibration clauses into petrochemical and desalination tenders. South America grows from a small base through Brazil's Sonitus Engenharia, whereas Africa's share clusters around South Africa's export assembly. Regional dispersion will persist, but accelerated Middle East adoption nudges its stake from low to mid-single digits by 2031.

- Bruel & Kjaer Sound & Vibration Measurement A/S

- National Instruments Corporation

- Siemens AG

- HEAD acoustics GmbH

- Hottinger Bruel & Kjaer GmbH (HBK)

- Dewesoft d.o.o.

- Kistler Instrumente AG

- GRAS Sound & Vibration A/S

- m+p international Mess- und Rechnertechnik GmbH

- Prosig Ltd.

- Data Physics Corporation

- Polytec GmbH

- Signal.X Technologies, LLC

- IMV Corporation

- RION Co., Ltd.

- SoundPlan GmbH

- Ono Sokki Co., Ltd.

- PCB Piezotronics, Inc.

- Microflown Technologies B.V.

- CRYSOUND Acoustic Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electrified-Powertrain NVH Requirements

- 4.2.2 Miniaturised MEMS Sensor Cost Declines

- 4.2.3 Stricter UNECE Exterior-Noise Rules

- 4.2.4 Predictive-Maintenance Adoption in Industry 4.0

- 4.2.5 Growth of Urban Air-Mobility Prototypes

- 4.2.6 Real-Time Cloud-Based NVH Analytics

- 4.3 Market Restraints

- 4.3.1 Shortage of Skilled NVH Engineers

- 4.3.2 High Capex for Modular Hemi-Anechoic Chambers

- 4.3.3 Absence of Global Test-Protocol Harmonisation

- 4.3.4 Data-Security Concerns in Remote Testing

- 4.4 Industry Value-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Data Acquisition Systems

- 5.1.1.2 Sensors and Transducers

- 5.1.1.3 Analyzers

- 5.1.1.4 Other Hardware

- 5.1.2 Software

- 5.1.2.1 Signal Analysis

- 5.1.2.2 Simulation and Modelling

- 5.1.3 Services

- 5.1.3.1 Testing Services

- 5.1.3.2 Consulting and Training

- 5.1.1 Hardware

- 5.2 By Testing Type

- 5.2.1 Modal Testing

- 5.2.2 Pass-By Noise Testing

- 5.2.3 Operational / Dynamic NVH Testing

- 5.2.4 Environmental-Chamber NVH

- 5.2.5 Powertrain NVH

- 5.3 By End-Use Industry

- 5.3.1 Automotive

- 5.3.2 Aerospace and Defense

- 5.3.3 Industrial Machinery

- 5.3.4 Consumer Electronics

- 5.3.5 Railways

- 5.3.6 Marine

- 5.4 By Application

- 5.4.1 Powertrain

- 5.4.2 Interior Cabin

- 5.4.3 Exterior Noise

- 5.4.4 Electric and Hybrid Components

- 5.4.5 Structural Components

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Bruel & Kjaer Sound & Vibration Measurement A/S

- 6.4.2 National Instruments Corporation

- 6.4.3 Siemens AG

- 6.4.4 HEAD acoustics GmbH

- 6.4.5 Hottinger Bruel & Kjaer GmbH (HBK)

- 6.4.6 Dewesoft d.o.o.

- 6.4.7 Kistler Instrumente AG

- 6.4.8 GRAS Sound & Vibration A/S

- 6.4.9 m+p international Mess- und Rechnertechnik GmbH

- 6.4.10 Prosig Ltd.

- 6.4.11 Data Physics Corporation

- 6.4.12 Polytec GmbH

- 6.4.13 Signal.X Technologies, LLC

- 6.4.14 IMV Corporation

- 6.4.15 RION Co., Ltd.

- 6.4.16 SoundPlan GmbH

- 6.4.17 Ono Sokki Co., Ltd.

- 6.4.18 PCB Piezotronics, Inc.

- 6.4.19 Microflown Technologies B.V.

- 6.4.20 CRYSOUND Acoustic Technology Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment