PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062391

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062391

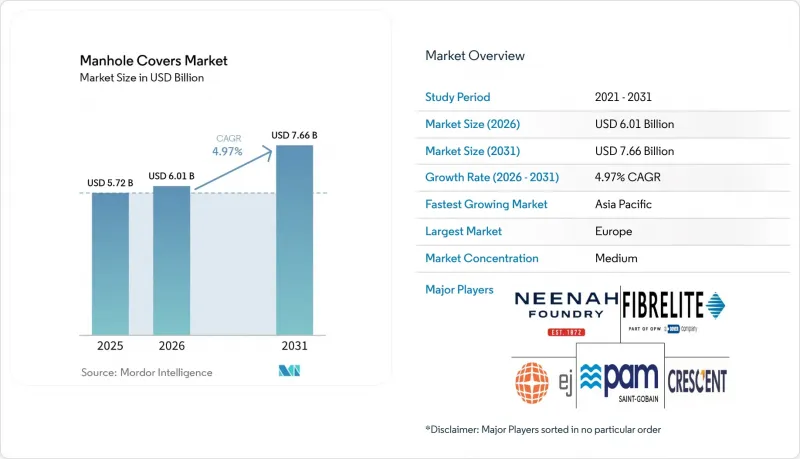

Manhole Covers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the manhole covers market size is expected to increase from USD 5.72 billion in 2025 to USD 6.01 billion in 2026 and reach USD 7.66 billion by 2031, growing at a CAGR of 4.97% over 2026-2031.

This report is Segmented by Material Type (Cast Iron, Ductile Iron, Steel, Reinforced Concrete, and More), Application (Road Infrastructure, Water and Waste-Water, Telecommunication and Data, Electric and Power Utility, Gas Distribution, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Manhole Covers Market Trends and Insights

Urbanization-Linked Megaproject Pipelines

Asia-Pacific infrastructure spending reached USD 1.7 trillion in 2025, embedding large-scale manhole procurement across road, rail, and utility projects. China's production capacity is expected to rise to 17.65 million units by 2030, surpassing domestic demand and intensifying price competition in ASEAN and the Middle-East. India's Smart Cities Mission allocated INR 48,000 crore (USD 5.8 billion), but 60% of tenders are still awarded to unorganized foundries that undercut certified suppliers. This fragmented sourcing delays IoT-ready upgrades and contributes to high theft rates; for example, Mumbai reported 791 cover thefts in 2023 despite grill retrofits costing USD 50-100 per site. Excess production in China is likely to cap regional average selling prices (ASPs) through 2029.

Smart-City Mandates for Real-Time Asset Monitoring

Pilot failures in Mumbai, where 40% of sensor units installed in 2021 malfunctioned within six months, highlight integration challenges when legacy cast-iron lids are reused. Fibrelite's FL60RF composite lids eliminate the need for external antenna mounts and reduce installation costs by 30%. Guangzhou Bangxun's NB-IoT lids, priced at USD 110-165 in bulk, support tilt and gas detection data streaming to city dashboards. Cities deploying sensor-ready covers have reduced emergency callouts by 25-35%. However, the presence of 50-70 million legacy lids in North America and Europe creates a gradual replacement cycle, with procurement phasing in smart lids during scheduled resurfacing to manage capital expenditures.

Volatile Ductile-Iron Scrap Prices Squeezing Margins

Scrap prices fluctuated between USD 1,800 and USD 2,200 per ton in 2025, reducing foundry EBITDA by approximately 18%. McWane's USD 80 million upgrade in Oskaloosa, which includes melt-efficiency furnaces and long-term scrap contracts, aims to mitigate raw material risks but will not fully address the issue until at least 2027. Smaller foundries, lacking hedging mechanisms, pass price spikes to municipalities with a six-month lag, prompting buyers to explore composites with stable resin pricing. In India, the use of low-grade scrap leads to premature lid failures, but cost considerations continue to dominate municipal tender decisions, leaving safety concerns unresolved.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Composite/Lightweight Anti-theft Covers

- Growth in Underground Fiber and 5G Densification

- Unorganized Small Foundries Limiting Standardization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Composite materials are projected to grow at a CAGR of 5.88% through 2031, while cast iron accounted for 45.89% of revenue in 2025. Ductile iron remains essential for F900 traffic loads, and McWane's Oskaloosa expansion positions the company to meet North American highway demands through 2030. Steel variants are utilized in rail and airfield applications but require galvanization, which increases costs by 20-25%. Reinforced concrete is a cost-effective option for water utilities but is prone to cracking under freeze-thaw conditions, leading desert municipalities to adopt polymer-concrete inserts that double the lifespan.

Composite materials, priced at USD 300-800, are approximately twice as expensive as cast iron but offer advantages such as theft prevention, reduced ergonomic risks, and compatibility with sensors. Fibrelite's RF-transparent products commanded a 40% premium in 2025 because telecom buyers prioritized signal integrity. Polymer-concrete variants resist acids but face regulatory challenges under EU leach rules, prompting suppliers to diversify into fiber-reinforced plastics. Material strategies are diverging: one supply chain focuses on weight-bearing ductile iron for heavy traffic, while another targets theft-prone, sensor-integrated urban areas, limiting competition between the two segments.

Geography Analysis

Europe accounted for 40.38% of the manhole covers market share in 2025, underpinned by EN 124:2015, which harmonizes load classes A15-F900. Germany, the UK, France, and Italy represent the majority of regional volume, and NORDIC utilities favor composites for freeze-thaw durability. Spain's Barcelona and Madrid pilots integrate LoRaWAN lids, yet decision rights lie with regional councils, slowing standard adoption. Russia relies on joint ventures to supply ductile-iron lids domestically, but sanctions have stunted technology upgrades.

Asia-Pacific will post the fastest 5.73% CAGR through 2031, propelled by China's capacity jump to 17.65 million units by 2030, which overhangs prices across ASEAN. India's non-standard tender rules allow unorganized shops, yet Smart Cities Mission funds still provide volume, making the region primarily price-led. Japan and South Korea enforce odor-filter mandates, producing a high-margin replacement cycle every 18-24 months. Belt-and-Road projects in Indonesia and Vietnam expand transport corridors but specify low-cost cast iron, so composite inroads stay niche.

North America faces a USD 176 billion wastewater backlog, and manhole upgrades fold into that capex. Charlotte Pipe's 2026 Neenah takeover consolidates cast-iron output, aiming for scale against margin volatility. Gilbert, Arizona's polymer-concrete rollout proves that documented lifecycle savings override upfront cost objections, but AASHTO M306 still guards highway segments for ductile iron. Mexico leans on industrial builds tied to near-shoring, while Brazil and Argentina stay price sensitive, adopting composites only in theft hot-spots. Middle-East megacities like NEOM issue large but lumpy tenders; thus, supplier forecasts hinge on a handful of giga-projects.

- ACO Pty Ltd.

- Aliaxis

- Clark-Drain Ltd.

- Crescent Foundry

- Ducast Factory LLC

- Eagle Technocast

- EJ Group, Inc.

- Fibrelite Composites Ltd.

- Fibrocast

- Forecourt Solutions

- HAURATON GmbH & Co. KG

- HYDROTEC Technologies AG

- McWane, LLC

- Neenah Foundry

- Polieco Group

- Poly Products (I) Pvt. Ltd.

- Prime Composites Australia Pty Ltd.

- PROLONG COMPOSITES INDIA PVT. LTD.

- Saint-Gobain PAM

- SMC BMC Manhole Cover

- Terra Firma Industries

- THERMODRAIN

- United States Foundries Inc.

- Vikrant Manhole Covers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Urbanisation-linked megaproject pipelines

- 4.2.2 Smart-city mandates for real-time asset monitoring

- 4.2.3 Shift toward composite/lightweight anti-theft covers

- 4.2.4 Growth in underground fibre and 5G densification

- 4.2.5 Mandated anti-odour bio-filter covers in high-density cities

- 4.3 Market Restraints

- 4.3.1 Volatile ductile-iron scrap prices squeezing margins

- 4.3.2 Unorganised small foundries limiting standardisation

- 4.3.3 Micro-plastic leach regulations curbing polymer-concrete use

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Cast Iron

- 5.1.2 Ductile Iron

- 5.1.3 Steel

- 5.1.4 Reinforced Concrete

- 5.1.5 Polymer Concrete

- 5.1.6 Composite Materials

- 5.1.7 Other Material Types (HDPE, FRP, etc.)

- 5.2 By Application

- 5.2.1 Road Infrastructure

- 5.2.2 Water and Waste-water

- 5.2.3 Telecommunication and Data

- 5.2.4 Electric and Power Utility

- 5.2.5 Gas Distribution

- 5.2.6 Rail and Airport

- 5.2.7 Industrial and Commercial Facilities

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 ACO Pty Ltd.

- 6.4.2 Aliaxis

- 6.4.3 Clark-Drain Ltd.

- 6.4.4 Crescent Foundry

- 6.4.5 Ducast Factory LLC

- 6.4.6 Eagle Technocast

- 6.4.7 EJ Group, Inc.

- 6.4.8 Fibrelite Composites Ltd.

- 6.4.9 Fibrocast

- 6.4.10 Forecourt Solutions

- 6.4.11 HAURATON GmbH & Co. KG

- 6.4.12 HYDROTEC Technologies AG

- 6.4.13 McWane, LLC

- 6.4.14 Neenah Foundry

- 6.4.15 Polieco Group

- 6.4.16 Poly Products (I) Pvt. Ltd.

- 6.4.17 Prime Composites Australia Pty Ltd.

- 6.4.18 PROLONG COMPOSITES INDIA PVT. LTD.

- 6.4.19 Saint-Gobain PAM

- 6.4.20 SMC BMC Manhole Cover

- 6.4.21 Terra Firma Industries

- 6.4.22 THERMODRAIN

- 6.4.23 United States Foundries Inc.

- 6.4.24 Vikrant Manhole Covers

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment