PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062425

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062425

Quantum Networking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

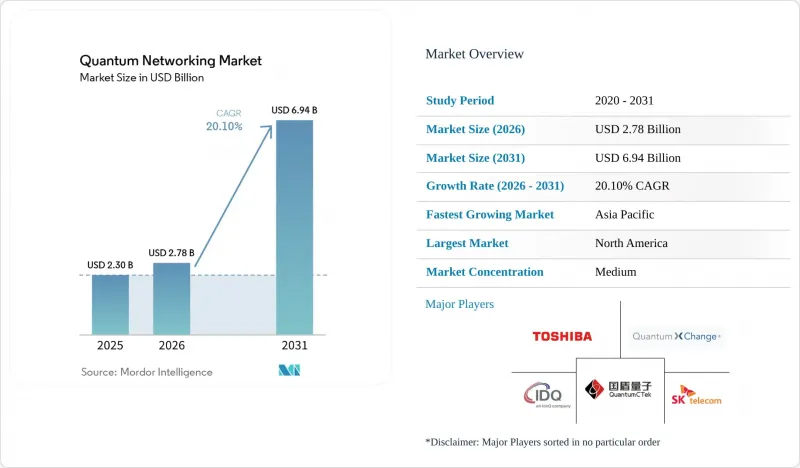

According to Mordor Intelligence, the quantum networking market size is projected to expand from USD 2.78 billion in 2026 to USD 6.94 billion by 2031, registering a CAGR of 20.1% over 2026-2031.

This report is Segmented by Component (Hardware, Software, and Services), Application (Quantum Key Distribution, Secure Cloud Communications, and More), End-User (Government and Defense, Large Enterprises, Telecom and IT, Financial Services, and More), Network Type (Terrestrial Fiber Networks, Free-Space Optical Links, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Quantum Networking Market Trends and Insights

Escalating Cybersecurity Threat from Quantum-Capable Adversaries

Harvest-now-decrypt-later campaigns are accelerating as nation-state actors cache encrypted traffic in anticipation of fault-tolerant quantum computers. With classical public-key cryptography vulnerable, QKD delivers provably secure keys that nullify brute-force decryption. The United States finalized post-quantum algorithms in 2024, yet retrofit efforts will take years, creating a window where QKD provides immediate risk mitigation.China extended its quantum backbone to Johannesburg in 2025, underscoring the geopolitical stakes of secure key exchange. Major banks such as JPMorgan Chase have already linked their trading desks via QKD, citing a 18% reduction in latency compared to software-only alternatives.

Rising Government Funding and National Programs

Public financing de-risks private investment. The U.S. Department of Energy allocated USD 625 million in 2025 for a nationwide quantum-internet prototype.Europe's EuroQCI funnels EUR 730 million (USD 823 million) into a 10,000-kilometer cross-border network. India's USD 750 million National Quantum Mission is constructing a 2,000-kilometer backbone, while Japan's 600-kilometer Tokyo-Osaka link exceeded 1 Mbps key rates in 2024.These coordinated programs accelerate alignment with standards and catalyze vendor ecosystems.

High CAPEX for Quantum Repeaters and Satellite Payloads

Extending QKD beyond 100 kilometers without trusted nodes requires deploying quantum repeaters, which cost approximately USD 2-5 million each. For instance, a 500-kilometer metro loop may require installing around 10 repeaters, significantly increasing costs, particularly in developing regions where budgets are constrained. Additionally, satellite payloads for QKD implementation add substantial expenses, ranging from USD 50-150 million per launch. This is further compounded by the cost of ground-station optics, which can exceed USD 20 million, as reported by spacenews.com. These high costs create significant barriers to large-scale rollouts, limiting adoption primarily to nations with substantial financial resources or those driven by strategic mandates to invest in advanced quantum communication technologies.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Progress in Fiber and Satellite QKD Field-Trials

- Integration Prospects with 6G Mobile Core Networks

- Lack of Global Interoperability Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware held 60.18% quantum networking market share in 2025. Quantum random-number generators, single-photon sources, and avalanche photodiodes form the bedrock of secure links. The quantum networking market size attributable to services is projected to grow sharply, with a 20.68% CAGR, as operators wrap managed offerings around these assets. Infineon's cryogenic-ready detector reached 85% efficiency at telecom wavelengths, lengthening viable fiber spans. Parallel foundry scale-ups, such as Quantum Computing Inc.'s thin-film lithium-niobate line, aim to ship 10,000 photonic circuits per quarter by 2027.

Service revenue is consolidating among carriers that can amortize the cost of costly repeaters across thousands of enterprise circuits. Orange Business Services' Quantum Defender prices QKD as a subscription, converting capital outlays into operating expenses. This model allows enterprises to adopt quantum key distribution without significant upfront investments, making it more accessible to a broader range of businesses. Additionally, software vendors are enhancing their offerings by layering key-management orchestration on top of QKD systems, enabling seamless integration with existing IT infrastructures. These solutions are also incorporating post-quantum algorithms to ensure backward compatibility with legacy systems, addressing concerns about future-proofing. As hardware becomes increasingly commoditized, the focus of competition is shifting toward software automation, service quality, and the ability to deliver comprehensive, scalable solutions that meet the evolving needs of enterprise customers.

Quantum key distribution accounted for 62.28% of the quantum networking market in 2025, yet distributed quantum computing is the fastest riser, with a 20.97% CAGR through 2031. Linking multiple processors via entanglement scales logical qubits beyond single-site ceilings, a capability IBM proved by accelerating a variational eigensolver 40% using a three-node network. Hyperscalers now pilot hybrid architectures that blend QKD with post-quantum cryptography to secure data-center interconnects at up to 100 Gbps.

Secure cloud communications are gaining significant traction as the European NIS2 directive mandates that critical infrastructure operators implement quantum-safe encryption measures. This directive has driven organizations to prioritize secure data transmission to ensure compliance with stringent regulations. Quantum sensor networks, while still a niche application, are drawing increasing interest from the defense sector due to their potential in precision timing and gravitational anomaly detection. These networks are expected to play a pivotal role in enhancing defense capabilities. Furthermore, as distributed computing continues to evolve, traffic patterns are anticipated to increasingly rely on entanglement-enabled backbones. This shift will further amplify demand for low-latency QKD (Quantum Key Distribution) links, which are essential for maintaining secure, efficient communication in advanced computing environments.

Geography Analysis

North America captured 50.49% revenue in 2025, driven by significant venture funding, stringent banking regulations, and the U.S. Department of Energy's 17-node quantum internet prototype. Canada invested CAD 360 million (USD 267 million) in 2025 to secure energy and telecom assets, while Mexico initiated pilot projects for university-run QKD links. The region's market leadership is attributed to a strong ecosystem of hyperscalers, defense contractors, and photonics startups concentrated in Silicon Valley, Boston, and Toronto.

Asia-Pacific is projected to grow at a CAGR of 20.88% through 2031. China operates a 10,000-kilometer, 145-node national backbone, highlighting its focus on sovereign technological advancements. Japan, South Korea, and Singapore are expanding metropolitan QKD clusters, while India has allocated USD 750 million for a 2,000-kilometer quantum spine by 2028. Australia is funding quantum memory research to extend the storage time of repeater states. Although regional standards remain fragmented, strong government support is accelerating scalability across the region.

Europe benefits from EUR 730 million (USD 849.9 million) in EuroQCI funding and cohesive regulatory frameworks. Deutsche Telekom's 30-kilometer entanglement teleportation has validated urban deployments, while NIS2 mandates are driving enterprise adoption. The United Kingdom, Germany, France, Italy, and Spain are developing national backbones that are expected to interconnect under EuroQCI by 2027. Smaller economies are following suit, although fragmented telecom markets are slowing uniform adoption. The Middle East and Africa, along with South America, are trailing but showing targeted progress. Saudi Arabia is securing offshore energy assets using QKD, and the UAE is piloting sovereign data links. South Africa has joined China's Beijing-Johannesburg quantum route, bypassing domestic capital expenditure constraints. Brazil is collaborating on satellite ground stations, and Chile is funding quantum sensing for mining applications. However, limited budgets in these regions are tempering large-scale deployments. Across emerging markets, hub-and-spoke satellite models are being explored to overcome limitations in the fiber infrastructure.

- Alibaba Group Holding Limited (Alibaba Quantum Laboratory)

- Alphabet Inc. (Google Quantum AI)

- Amazon Web Services, Inc.

- Anellos Photonics Inc.

- Atos SE

- Baidu, Inc.

- BT Group plc

- China Aerospace Science and Industry Corporation Limited

- D-Wave Quantum Inc.

- Fujitsu Limited

- Huawei Technologies Co., Ltd.

- ID Quantique SA

- Infineon Technologies AG

- IonQ, Inc.

- Nokia Corporation

- Quantum Xchange, Inc.

- QuTech (Stichting Veldhoven Institute)

- Rigetti and Co, LLC

- SK Telecom Co., Ltd.

- Toshiba Digital Solutions Corporation

- Verizon Communications Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Cybersecurity Threat from Quantum-Capable Adversaries

- 4.2.2 Rising Government Funding and National Programs

- 4.2.3 Rapid Progress in Fiber and Satellite QKD Field-Trials

- 4.2.4 Integration Prospects with 6G Mobile Core Networks

- 4.2.5 Photonic Chip Foundry Scale-Ups Lowering Component Costs

- 4.2.6 Hyperscaler Push for Hybrid Quantum-Secure Cloud Interconnect

- 4.3 Market Restraints

- 4.3.1 High CAPEX for Quantum Repeaters and Satellite Payloads

- 4.3.2 Lack of Global Interoperability Standards

- 4.3.3 Fiber PMD Limits Reach without Trusted Nodes

- 4.3.4 Shortage of Cryogenic Infrastructure in Emerging Economies

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Application

- 5.2.1 Quantum Key Distribution (QKD)

- 5.2.2 Secure Cloud Communications

- 5.2.3 Distributed Quantum Computing

- 5.2.4 Quantum Sensor Networks

- 5.2.5 Other Applications

- 5.3 By End-User

- 5.3.1 Government and Defense

- 5.3.2 Large Enterprises

- 5.3.3 Telecom and IT

- 5.3.4 Financial Services

- 5.3.5 Healthcare and Life Sciences

- 5.3.6 Energy and Utilities

- 5.3.7 Research and Academia

- 5.4 By Network Type

- 5.4.1 Terrestrial Fiber Networks

- 5.4.2 Free-Space Optical Links

- 5.4.3 Satellite-Based Links

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Singapore

- 5.5.4.7 Malaysia

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Alibaba Group Holding Limited (Alibaba Quantum Laboratory)

- 6.4.2 Alphabet Inc. (Google Quantum AI)

- 6.4.3 Amazon Web Services, Inc.

- 6.4.4 Anellos Photonics Inc.

- 6.4.5 Atos SE

- 6.4.6 Baidu, Inc.

- 6.4.7 BT Group plc

- 6.4.8 China Aerospace Science and Industry Corporation Limited

- 6.4.9 D-Wave Quantum Inc.

- 6.4.10 Fujitsu Limited

- 6.4.11 Huawei Technologies Co., Ltd.

- 6.4.12 ID Quantique SA

- 6.4.13 Infineon Technologies AG

- 6.4.14 IonQ, Inc.

- 6.4.15 Nokia Corporation

- 6.4.16 Quantum Xchange, Inc.

- 6.4.17 QuTech (Stichting Veldhoven Institute)

- 6.4.18 Rigetti and Co, LLC

- 6.4.19 SK Telecom Co., Ltd.

- 6.4.20 Toshiba Digital Solutions Corporation

- 6.4.21 Verizon Communications Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment