PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062427

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062427

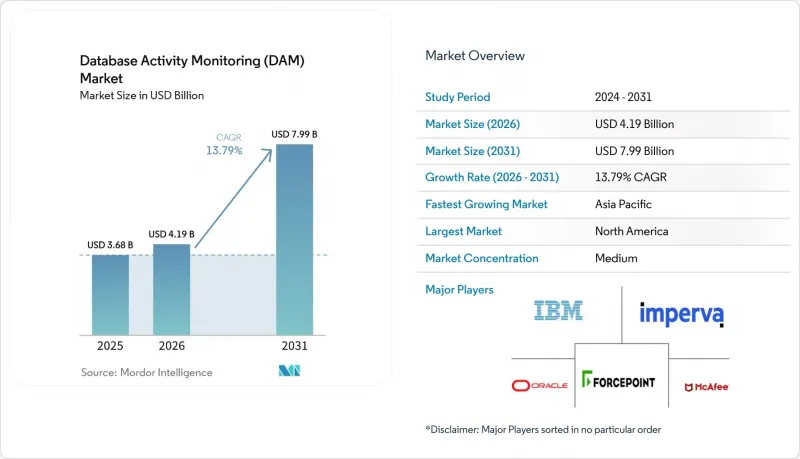

Database Activity Monitoring (DAM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the database activity monitoring (DAM) market size was USD 3.68 billion in 2025, USD 4.19 billion in 2026, and is anticipated to reach USD 7.99 billion by 2031, growing at a CAGR of 13.79% from 2026 to 2031.

This report is Segmented by Component (Software and Services), Deployment Mode (On-Premises, Cloud-Based, and More), Organization Size (Small and Medium Enterprises, and Large Enterprises), Database Type (Relational, Nosql, and More), End-User Industry (BFSI, Healthcare, Retail, Government, IT and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Database Activity Monitoring (DAM) Market Trends and Insights

Escalating Data-Sovereignty Fines Reshape Compliance Budgets

In the Database Activity Monitoring (DAM) market, global regulators imposed EUR 1.2 billion (USD 1.35 billion) in GDPR penalties during 2024, led by EUR 310 million (USD 350.3 million) against LinkedIn and EUR 251 million (USD 283.63 million) against Meta EDPB. Enterprises are directing fresh capital to continuous query-level audit trails that record every cross-border transfer in real time. U.S. healthcare providers face parallel pressure as HIPAA enforcement adds mandatory multi-factor authentication by 2026, prompting hospitals to treat monitoring as a core security control. This regulatory tempo explains why the Database Activity Monitoring market is pivoting from quarterly compliance checks to always-on anomaly-detection infrastructure. Real-time visibility is now a board-level budget line rather than a discretionary item.

Multi-Cloud Workload Migration Fragments Visibility

Synergy Research Group found that AWS held 31%, Azure 25%, and Google Cloud 11% of infrastructure share in Q4 2024, while 87% of enterprises ran workloads across more than one hyperscaler. Each cloud keeps proprietary log schemas that force security teams to normalize data before analysis. The mid-2024 Snowflake breach, which exposed 73 million AT&T and 560 million Ticketmaster records, showed how inconsistent session monitoring across regions can snowball into systemic compromise. Consolidated dashboards that merge on-premises Oracle logs with Snowflake events are therefore moving from wish-list to purchase order.

Performance Overhead in Real-Time Workloads Constrains Deployment

Inline agents impose 5-15% CPU drag that trading systems and Black Friday retail traffic cannot tolerate, and a 100-millisecond delay can shave 7% off cart conversions. Merchants thus sample 10-20% of queries, but gaps let sophisticated attacks hide. PCI DSS v4.0.1 insists on continuous audit coverage, intensifying the struggle. Agentless cloud APIs solve part of the issue, but legacy on-premises estates still face the overhead dilemma.

Other drivers and restraints analyzed in the detailed report include:

- AI-Driven Insider-Threat Detection Moves Beyond Rule-Based Alerts

- SIEM-SOAR Integrations Transform Monitoring into Automated Response

- Shortage of DAM Security Specialists Limits Effective Implementation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based monitoring is projected to post a 17.5% CAGR to 2031 as Amazon Web Services, Azure, and Google Cloud embed native audit log streams. On-premises still controls 63.5% revenue because mission-critical Oracle and IBM Db2 applications remain in corporate data centers in the DAM market. Hybrid rollouts let organizations standardize logging across both environments, meeting data-residency mandates that prohibit the external storage of regulated information.

European Union transfer restrictions and United States federal zero-trust directives encourage localized logging, but cost relief and reduced CPU overhead make cloud-delivered monitoring attractive once compliance officers approve. Enterprises in long migration cycles are standardizing on single dashboards that ingest Snowflake, MongoDB Atlas, and on-premises SQL telemetry side by side.

Managed Services revenue is rising faster than overall demand in the database activity monitoring market, advancing at a 14.8% CAGR through 2031, as buyers outsource detective controls to 24-hour monitoring partners. Software still owns the majority share thanks to perpetual licensing, preferred by financial institutions that keep tooling on-premises. Agent-based suites dominate deep session inspection for Oracle and IBM Db2, while agentless deployments introduced by Microsoft Database Watcher and Datadog attract latency-sensitive workloads.

Second-generation managed detection and response providers integrate rule tuning, threat intelligence, and automated containment. This appeal is strongest in Asia-Pacific, where certified database talent is scarce, and boards seek quicker deployment over long-term capability building. Professional Services revenue also climbs as integrators stitch database logs into centralized security information and event management pipelines.

Geography Analysis

North America accounted for the largest share of the Database Activity Monitoring (DAM) market in 2025, with 38.4% revenue, as Executive Order 14144 and HIPAA rules converged, driving zero-trust rollouts across federal, healthcare, and insurance verticals. The Snowflake breach raised public awareness, leading to a 22% increase in agentless deployments in Q3 2024. Canada's cyber center issued similar directives, while Mexican banks tighten logging to meet data-residency clauses.

Asia-Pacific registers the fastest CAGR at 14.40% through 2031 as China's Personal Information Protection Law, Singapore's revised PDPA, and India's Digital Personal Data Protection Act all require localized audit infrastructure. Japanese and Korean semiconductor plants protect intellectual property with continuous monitoring, and Australia raises penalties to AUD 50 million (USD 33 million) for firms lacking reasonable safeguards.

Europe remains pivotal because GDPR fines totaled EUR 1.2 billion (USD 1.4 billion) in 2024, far exceeding prior years. Germany's 12-month log mandate sets a standard that cascades into private procurement. South America progresses as Brazil's LGPD issues its first enforcement cases, while the Middle East and Africa growth rides the UAE and Saudi data-localization statutes that push on-premises or in-country cloud logs.

- International Business Machines Corporation

- Imperva Inc. (Thales S.A.)

- Oracle Corporation

- McAfee LLC

- Forcepoint LLC

- HexaTier Ltd.

- Trustwave Holdings Inc.

- SolarWinds Corporation

- Quest Software Inc.

- Guardicore Ltd. (Akamai Technologies)

- Idera Inc.

- Datadog Inc.

- Micro Focus International plc

- Amazon Web Services Inc.

- Google Cloud Platform (Chronicle Security)

- Teradata Corporation

- SAP SE

- Snowflake Inc.

- Microsoft Corporation (Azure SQL)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Data-Sovereignty Fines

- 4.2.2 Multi-cloud Workload Migration

- 4.2.3 AI-driven Insider-threat Detection

- 4.2.4 Zero-trust Mandates in Public Sector

- 4.2.5 SIEM-SOAR Integrations

- 4.2.6 Agentless Telemetry Adoption

- 4.3 Market Restraints

- 4.3.1 Performance Overhead in Real-time Workloads

- 4.3.2 Shortage of DAM Security Specialists

- 4.3.3 Heterogeneous Database Environments

- 4.3.4 False-positive Fatigue

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Agent-based Monitoring

- 5.1.1.2 Agentless Monitoring

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Software

- 5.2 By Deployment Mode

- 5.2.1 On-premises

- 5.2.2 Cloud-based

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By Database Type

- 5.4.1 Relational Databases

- 5.4.2 NoSQL Databases

- 5.4.3 Big Data / Hadoop

- 5.4.4 Cloud-native Databases

- 5.5 By End-User Industry

- 5.5.1 Banking, Financial Services and Insurance

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Retail and E-commerce

- 5.5.4 Government and Defense

- 5.5.5 IT and Telecommunications

- 5.5.6 Industrial and Manufacturing

- 5.5.7 Energy and Utilities

- 5.5.8 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 International Business Machines Corporation

- 6.4.2 Imperva Inc. (Thales S.A.)

- 6.4.3 Oracle Corporation

- 6.4.4 McAfee LLC

- 6.4.5 Forcepoint LLC

- 6.4.6 HexaTier Ltd.

- 6.4.7 Trustwave Holdings Inc.

- 6.4.8 SolarWinds Corporation

- 6.4.9 Quest Software Inc.

- 6.4.10 Guardicore Ltd. (Akamai Technologies)

- 6.4.11 Idera Inc.

- 6.4.12 Datadog Inc.

- 6.4.13 Micro Focus International plc

- 6.4.14 Amazon Web Services Inc.

- 6.4.15 Google Cloud Platform (Chronicle Security)

- 6.4.16 Teradata Corporation

- 6.4.17 SAP SE

- 6.4.18 Snowflake Inc.

- 6.4.19 Microsoft Corporation (Azure SQL)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment