PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062431

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062431

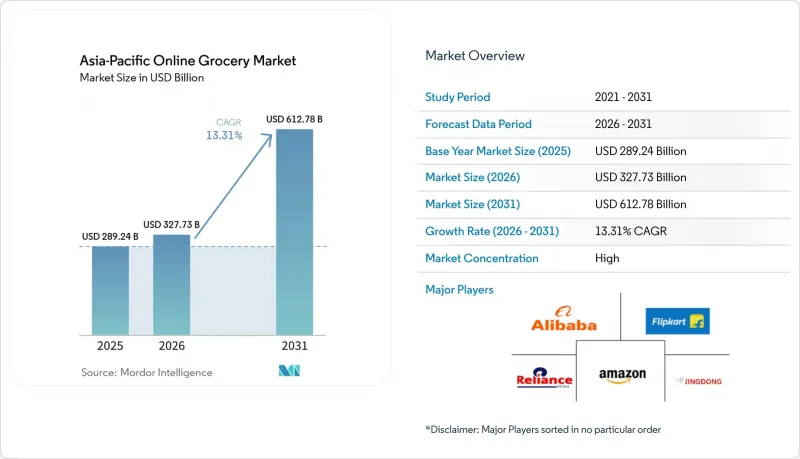

Asia-Pacific Online Grocery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific online grocery delivery market is expected to grow from USD 289.24 billion in 2025 to USD 327.73 billion in 2026 and is forecast to reach USD 612.78 billion by 2031 at a CAGR of 13.31% over 2026-2031.

This report is Segmented by Product Category (Fresh Produce, Packaged Foods, Beverages, and More), Delivery Speed (Instant/Same Day, Scheduled/Next Day), Fulfilment Model (Marketplace Aggregator, Retailer-Owned Dark and More), Order-Frequency Plan (On-Demand, Subscription Auto-Replenish), and Geography (China, India, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Online Grocery Market Trends and Insights

Rising Online Adoption of Fresh and Perishable Grocery Categories

Fresh produce has become a key growth driver for platforms, supported by advancements in temperature-controlled logistics and automated picking, which enhance order accuracy and minimize waste. Automated customer fulfillment centers in Sydney and Melbourne have increased throughput and improved freshness, enabling scalable two-hour delivery windows and strengthening consumer trust in online purchases of perishables. Cold chain gaps persist in several markets, with India experiencing post-harvest losses of 5-15% for fruits and vegetables due to inadequate farmgate infrastructure and a focus on single commodities. Regional cold chain projects and modernized logistics systems are addressing these challenges, while Southeast Asia requires further investment in storage, energy-efficient operations, and digital WMS and TMS.

Smartphone Penetration Driving Mobile-First Grocery Shopping Behavior

Mobile devices dominate digital commerce access across Asia-Pacific, with smartphone adoption shaping how consumers discover, order, and pay for groceries. Younger demographics and urban density drive frequent orders, while real-time inventory visibility and route optimization reduce delivery times. In Japan, e-commerce ecosystems integrate fulfillment centers, loyalty programs, and payment systems, enhancing engagement for routine grocery purchases. Regional policies on digital identity and cross-border data flows aim to ease checkout and compliance for mobile-first transactions across ASEAN. In India, account-to-account payments and minimal transaction costs eliminate cash-handling inefficiencies, enabling quick, low-value transactions and supporting mobile grocery adoption at scale.

High Last-Mile Delivery Costs and Urban Congestion Challenges

Urban congestion and delivery density variability keep last-mile costs high, impacting unit economics for under-30-minute delivery. Platforms address these challenges through route clustering, batched picking, and dynamic labor allocation, but demand fluctuations driven by time of day and weather drive cost-to-serve variability. Perishable-heavy baskets can improve margins if spoilage is controlled, though temperature-controlled handling and returns management add costs requiring scale to offset. Retailer-owned store networks mitigate last-mile complexities by using backrooms and curbside pickup to smooth peak-hour demand and reduce delivery distances. Urban policies on curb space, delivery windows, and rider safety influence capacity planning, requiring compliance while maintaining delivery speed.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Growth of Quick-Commerce for Instant Delivery Needs

- Government Support for Digital Infrastructure and E-Commerce Adoption

- Inadequate Cold Chain Infrastructure in Tier-2 and Tier-3 Cities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Same-day and next-day services are projected to account for 53.48% of the market in 2025, with ultra-fast delivery within 30 minutes growing at a CAGR of 18.74% through 2031. Dense networks and automated fulfillment systems are transforming access to daily essentials across cities. The Asia-Pacific online grocery delivery market is shifting toward shorter delivery windows, balancing express deliveries for smaller orders with scheduled deliveries for larger baskets to optimize vehicle utilization and labor productivity. Automated customer fulfillment centers in Australia enhance throughput and accuracy for high-demand items, increasing two-hour delivery rates in metropolitan areas and strengthening trust in fresh delivery services. In China, networked warehouses integrated with online assortments enable 30-minute delivery in dense areas, supported by selective offline locations for instant delivery.

Advancements in routing, inventory visibility, and city logistics reduce cancellations and substitutions, improving customer experience in fast-delivery formats. Scheduled deliveries beyond 24 hours remain vital for bulk restocking in suburban areas, ensuring the relevance of longer delivery windows. Micro-fulfillment adoption compresses pick-to-ship times, expanding same-day delivery coverage. Hybrid models like click-and-collect lower last-mile costs and improve suburban pickup options. Platforms use short-window order data to refine assortments and pricing, enhancing conversion rates. The market trends toward shorter timelines while maintaining capacity for larger orders, mitigating peak demand and ensuring fresh product availability.

List of Companies Covered in this Report:

- Alibaba Group

- JD.com

- Amazon

- Reliance Retail

- Flipkart

- Zomato

- Swiggy

- Zepto

- Dingdong Maicai

- Meituan Maicai

- Pinduoduo

- Woolworths Group

- Coles Group

- NTUC FairPrice

- Lazada

- Rakuten

- Coupang

- Grab

- Foodpanda

- Ocado

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising online adoption of fresh and perishable grocery categories

- 4.2.2 Smartphone penetration driving mobile-first grocery shopping behavior

- 4.2.3 Rapid growth of quick-commerce for instant delivery needs

- 4.2.4 Increasing FMCG spending on in-app advertising and promotions

- 4.2.5 Expansion of subscription-based models for recurring essentials

- 4.2.6 Government support for digital infrastructure and e-commerce adoption

- 4.3 Market Restraints

- 4.3.1 High last-mile delivery costs and urban congestion challenges

- 4.3.2 Inadequate cold chain infrastructure in Tier-2 and Tier-3 cities

- 4.3.3 Rising urban warehousing costs impacting quick-commerce margins

- 4.3.4 Intense competition leading to sustained margin pressure

- 4.4 Consumer Behevaior Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Delivery Speed

- 5.1.1 <=30 Minutes

- 5.1.2 Same-Day (2-12 h) and Next Day

- 5.1.3 Scheduled (more than 24 h)

- 5.2 By Product Type

- 5.2.1 Fresh Produce

- 5.2.2 Dairy and Bakery

- 5.2.3 Meat, Fish, and Seafood

- 5.2.4 Staples and Packaged Goods

- 5.2.5 Beverages

- 5.2.6 Frozen Foods

- 5.2.7 Other Product Type

- 5.3 By Delivery Channel

- 5.3.1 Direct-to-Consumer (D2C)

- 5.3.2 Aggregator Platforms

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 Australia

- 5.4.5 Indonesia

- 5.4.6 South Korea

- 5.4.7 Thailand

- 5.4.8 Singapore

- 5.4.10 Vietnam

- 5.4.11 Philippines

- 5.4.12 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Alibaba Group

- 6.4.2 JD.com

- 6.4.3 Amazon

- 6.4.4 Reliance Retail

- 6.4.5 Flipkart

- 6.4.6 Zomato

- 6.4.7 Swiggy

- 6.4.8 Zepto

- 6.4.9 Dingdong Maicai

- 6.4.10 Meituan Maicai

- 6.4.11 Pinduoduo

- 6.4.12 Woolworths Group

- 6.4.13 Coles Group

- 6.4.14 NTUC FairPrice

- 6.4.15 Lazada

- 6.4.16 Rakuten

- 6.4.17 Coupang

- 6.4.18 Grab

- 6.4.19 Foodpanda

- 6.4.20 Ocado

7 Market Opportunities and Future Trends