PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062435

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062435

Instructor-led Language Training - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

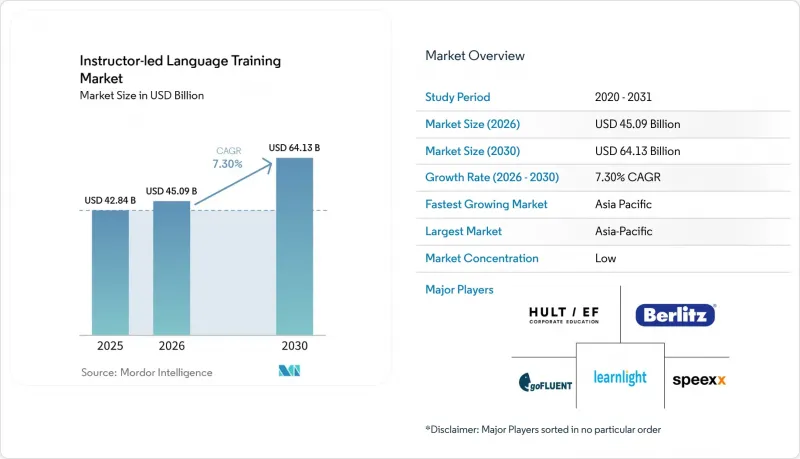

According to Mordor Intelligence, the instructor-led language training market size is projected to be USD 42.84 billion in 2025, USD 45.09 billion in 2026, and reach USD 64.13 billion by 2030, growing at a CAGR of 7.30% from 2026 to 2030.

This report is Segmented by Delivery Mode (On-Site Classroom Training, Virtual Live Classroom, Blended Learning, and More), End User (Corporates, Academic Institutions, Government & Defense, and More), Language (English, Mandarin Chinese, Spanish, French, and More), and Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Instructor-led Language Training Market Trends and Insights

Corporate Globalization Requiring Multilingual Teams

Multinational organizations continue to standardize language benchmarks to reduce friction in cross-border operations, and they anchor learning outcomes to CEFR levels for hiring and mobility decisions . Corporate buyers favor providers that integrate training into HR systems, so enrolments align to job-role thresholds, completion tracking, and audit readiness, which ties vendor selection to integration depth as much as to pedagogy. Aligning course design with recognized assessments makes the transition from training to certification smoother, especially as major tests refine CEFR mapping. Enterprises also respond to compliance-driven needs, where regulated communication and safety protocols prioritize verified proficiency, which sustains paid instructor-led programs even as unregulated skills move online. These preferences reinforce a premium segment of the instructor-led language training market where enterprise-grade reporting and CEFR-level accountability are non-negotiable.

Migration Inflows Raising Local Language Demand

Record migration inflows into OECD economies channel government budgets into instructor-led English and local language instruction for integration and employability . In the United States, refugee resettlement programs earmark education funding that supports adult English classes and employment-linked language services delivered by certified instructors. State-level programs fund time-bound, instructor-led language support during the first year of arrival, which sustains contracted delivery across community colleges and nonprofit providers. Best-practice guidelines for refugee education also point to bilingual instruction and live facilitation for low-literacy learners, which supports a human-led approach over self-paced modules. This policy backdrop anchors multi-year procurement for integration-focused classes and stabilizes capacity planning in the instructor-led language training market.

Higher Per-Learner Costs Than Apps

Instructor-led courses command higher per-learner costs than app subscriptions, which puts pressure on adoption among self-funded learners in price-sensitive markets. Even as enterprises fund premium formats, individual candidates often defer enrolment or switch to lower-cost options when macro conditions tighten. Providers counter with virtual delivery that reduces travel and facility expenses, and some report material cost advantages at scale when moving cohorts online. Targeted programs in lower-income regions also experiment with pricing tied to textbook-equivalent costs, enabled by AI-supported delivery that scales instructor time. Despite these steps, the value gap with self-paced apps remains a near-term brake on conversion in the instructor-led language training market.

Other drivers and restraints analyzed in the detailed report include:

- Exam-Prep Tie-Ins Boosting Paid ILT

- Hybrid Workplaces Favor Virtual Live Classes

- Shortage of Certified Native Instructors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-site classroom and blended formats together accounted for 47.36% of revenue in 2025, while virtual live classrooms are forecast to grow at a 15.48% CAGR through 2031, reflecting a measured shift toward scalable, instructor-led online cohorts within the instructor-led language training market. In blended programs, learners combine scheduled workshops with structured self-study to maintain a predictable cadence and ensure instructor accountability for working adults. Virtual live classrooms earn preference when organizations require consistent delivery across regions and the ability to add cohorts quickly based on hiring or compliance needs. In these environments, native-speaking instructors use AI-enabled role-play and voice recognition to simulate realistic communication tasks that build confidence and speed to competence. This mix of live facilitation and AI support is now a key differentiator, keeping the instructor-led language training industry focused on quality of interaction and measurable outcomes.

The depth of HR system integrations also matters because buyers want training to plug into performance management, talent mobility, and compliance dashboards. Providers that support off-the-shelf connectors for platforms like SAP SuccessFactors accelerate implementations for distributed teams and reduce administrative overhead. Private tutoring remains a resilient niche because executives and exam retakers value the focus of one-to-one sessions, and marketplaces scale matches across time zones and interests. Immersion programs continue to serve learners who want concentrated progress, but they face logistics and visa-related headwinds that can push organizations toward virtual alternatives. This segmentation pattern keeps virtual live classrooms central to growth while in-person formats retain strategic roles in the instructor-led language training market.

Geography Analysis

Asia-Pacific led the instructor-led language training market with a 41.78% share in 2025 and is projected to grow at a 13.75% CAGR through 2031, driven by corporate English requirements, large technology services workforces, and strong exam-prep demand. International student mobility continues to contribute to demand for certification and pathway programs that require structured, instructor-led support. Ministries that approve cost-effective CEFR-aligned credentials make large cohorts more affordable for the public sector and teacher training programs. In Japan, enterprise partnerships are scaling AI-powered virtual lessons to serve corporate learners who need structured coaching aligned with CEFR goals. These factors underpin a broad shift toward hybrid instructor-led delivery that meets both compliance and career advancement needs across APAC.

Europe maintains steady momentum supported by multilingual education systems and enterprise demand for standardized proficiency verification. Corporate buyers are increasing their reliance on integrated platforms that enroll and track employees against CEFR thresholds across regions, including large-scale deployments in German-speaking markets. Aviation English remains a staple of regulated training as European authorities enforce proficiency validity periods that create predictable recertification cycles. European data-localization norms and privacy expectations also shape vendor selection because clients require secure hosting and compliance-ready controls for live-class delivery. This environment keeps in-person and virtual instructor-led formats embedded in organizational learning across the region.

North America shows stable demand patterns anchored by corporate learning budgets and government-funded integration programs that support adult English classes. Marketplaces that connect large tutor networks with learners worldwide continue to attract investment, expanding one-to-one options for consumers and complementing enterprise-focused cohorts. In the Middle East and Africa, partnerships that deliver AI-supported instruction at textbook-equivalent prices aim to widen access where infrastructure or budgets limit traditional center-based models. These patterns show region-specific mixes of corporate, public, and consumer demand that continue to shape the instructor-led language training market.

- Hult EF Corporate Education (EF)

- Berlitz Corporation

- goFLUENT

- Learnlight

- Speexx

- Wall Street English

- British Council

- International House World Organisation

- inlingua

- Kaplan International Languages

- ELS Language Centers

- ILSC Education Group

- Open English

- Preply

- italki

- Lingoda

- Cambly

- Voxy

- Babbel Live (Babbel for Business)

- Busuu for Business

- Eton Institute

- Goethe-Institut

- Learnlight

- Lingoda

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Corporate globalization requiring multilingual teams

- 4.2.2 Migration inflows raising local language demand

- 4.2.3 Exam-prep tie-ins boosting paid ILT

- 4.2.4 Hybrid workplaces favor virtual live classes

- 4.2.5 Aviation, healthcare proficiency mandates drive ILT

- 4.2.6 LMS integrations enable scalable ILT

- 4.3 Market Restraints

- 4.3.1 Higher per-learner costs than apps

- 4.3.2 Shortage of certified native instructors

- 4.3.3 Live-class recording privacy compliance constraints

- 4.3.4 Travel visa volatility curbs boot-camps

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Delivery Mode

- 5.1.1 On-site Classroom Training

- 5.1.2 Virtual Live Classroom (Online)

- 5.1.3 Blended Learning

- 5.1.4 Immersion Boot-camps

- 5.1.5 Private Tutoring

- 5.2 By End User

- 5.2.1 Corporates

- 5.2.2 Academic Institutions

- 5.2.3 Government & Defense

- 5.2.4 Individuals / Migrants

- 5.2.5 Exam-Prep Providers

- 5.3 By Language

- 5.3.1 English

- 5.3.2 Mandarin Chinese

- 5.3.3 Spanish

- 5.3.4 French

- 5.3.5 German

- 5.3.6 Japanese

- 5.3.7 Others

- 5.4 By Region

- 5.4.1 North America

- 5.4.1.1 Canada

- 5.4.1.2 United States

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 BENELUX

- 5.4.3.7 NORDICS

- 5.4.3.8 Rest of Europe

- 5.4.4 APAC

- 5.4.4.1 India

- 5.4.4.2 China

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 South East Asia

- 5.4.4.7 Rest of APAC

- 5.4.5 Middle East & Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East & Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Hult EF Corporate Education (EF)

- 6.4.2 Berlitz Corporation

- 6.4.3 goFLUENT

- 6.4.4 Learnlight

- 6.4.5 Speexx

- 6.4.6 Wall Street English

- 6.4.7 British Council

- 6.4.8 International House World Organisation

- 6.4.9 inlingua

- 6.4.10 Kaplan International Languages

- 6.4.11 ELS Language Centers

- 6.4.12 ILSC Education Group

- 6.4.13 Open English

- 6.4.14 Preply

- 6.4.15 italki

- 6.4.16 Lingoda

- 6.4.17 Cambly

- 6.4.18 Voxy

- 6.4.19 Babbel Live (Babbel for Business)

- 6.4.20 Busuu for Business

- 6.4.21 Eton Institute

- 6.4.22 Goethe-Institut

- 6.4.23 Learnlight

- 6.4.24 Lingoda

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment