PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062437

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062437

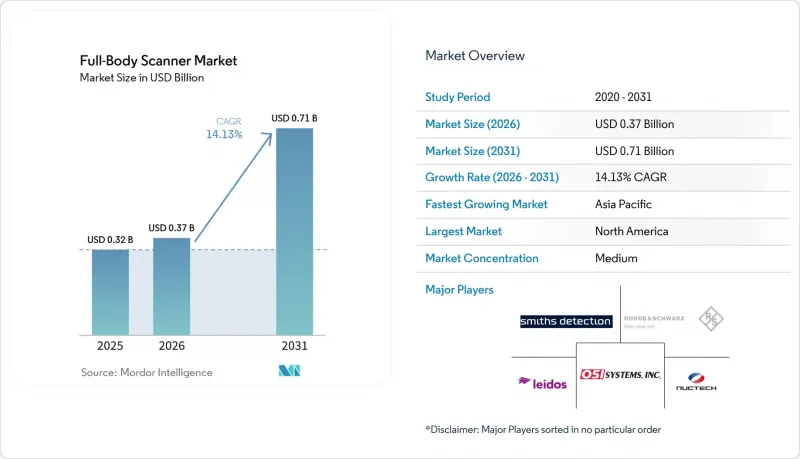

Full-Body Scanner - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the full-body scanner market size is expected to increase from USD 0.32 billion in 2025 to USD 0.37 billion in 2026 and reach USD 0.71 billion by 2031, growing at a CAGR of 14.13% over 2026-2031.

This report is Segmented by Technology (Millimeter-Wave Imaging, Backscatter X-Ray, Terahertz Imaging, and More), Application (Airport Security Checkpoints, Land and Sea Border Crossings, and More), Scanner Type (Fixed/Portal, Walk-Through Gate, and More), Component (Hardware, Software and Analytics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Full-Body Scanner Market Trends and Insights

Aviation Passenger-Volume Rebound

Single-day throughput at US checkpoints reached 3.13 million travelers in November 2025, surpassing pre-pandemic peaks and validating multi-year capital allocations for advanced imaging equipment. Brisbane Airport's eight-lane computed-tomography checkpoint, inaugurated in December 2025, doubled screening capacity and trimmed wait times by 30%, underscoring airlines' preference for high-throughput lanes during long-haul bank periods. South Korea's Incheon International Airport introduced a fully automated remote baggage-screening link with the US Customs and Border Protection in August 2025, shortening passenger connections by up to 20 minutes and showcasing cross-border collaboration made possible by next-generation scanners. Similar surge-demand dynamics will arise around the FIFA World Cup 2026, where pre-placed contracts for millimeter-wave portals at host-city airports highlight the full-body scanner market's event-driven upside. Across the Asia-Pacific, immigration agencies are pursuing upgrades to e-gates and body scanners in tandem, signaling convergent growth in people- and baggage-screening infrastructure.

Tightening Global Anti-Terrorism Regulations

India's Bureau of Civil Aviation Security now obliges airports handling >= 10 million annual passengers to install full-body scanners, catalyzing live trials of 70-80 GHz portals at Delhi Indira Gandhi International Airport that can process 1,200 scans per hour. Australia mandated the adoption of computed tomography at primary gateways by mid-2026, prompting nationwide retrofits that hardwire advanced imaging into domestic security codes. In the United States, Section 44925 of Title 49 codifies advanced imaging as the preferred primary screening modality, reinforcing the Transportation Security Administration's multi-billion-dollar fleet-refresh roadmap. Europe's Civil Aviation Conference continues to tighten Standard 3.1 image-quality benchmarks, pushing operators to retire legacy backscatter units in favor of millimeter-wave portals certified to the latest specification. Collectively, these statutes lock in a compliance-driven replacement wave that shields volumes against cyclical capex fluctuations.

Privacy and Data-Protection Litigation Risk

The 2025 Muir v. Department of Homeland Security filing alleges disproportionate false positives among passengers with disabilities, potentially forcing recalibration protocols that lengthen certification lead-times. A parallel settlement obliges the Transportation Security Administration to publish quarterly deletion-compliance reports, adding administrative overhead to fleet operations. Europe's General Data Protection Regulation pushes airports toward explicit-consent workflows, diverging from US opt-out norms and complicating multinational equipment rollouts. The Privacy and Civil Liberties Oversight Board now recommends six-month algorithm-bias audits for biometric integrations, elevating ongoing compliance costs for vendors. As airports weigh litigation exposure against throughput gains, procurement cycles risk elongation, tempering near-term momentum in the full-body scanner market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Decline in Millimeter-Wave Scanner Cost Curve

- Digital Twin-Enabled Checkpoint Optimization

- High Capital Expenditure for Mid-Tier Airports

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Millimeter-wave imaging accounted for 48.18% of revenue in 2025, anchored by certifications from the Transportation Security Administration and the European Civil Aviation Conference. Terahertz systems, however, are on track for a 14.78% CAGR, buoyed by sub-millimeter resolution breakthroughs at 220 GHz that enable video-rate concealed-object detection without motion controllers. The full-body scanner market size for millimeter-wave portals is expanding steadily, yet terahertz's ability to detect non-metallic contraband positions it for rapid share gains once certification paths mature. In applied trials, prototype handheld terahertz devices weighing under 5 kg expanded effective aperture by over 50 times, pointing to field-ready deployments in border patrol scenarios where portability dictates form-factor choices. Backscatter X-ray platforms remain confined to specialty use cases, such as drive-by vehicle inspection, while dual-energy transmission scanners are gaining traction in cargo applications.

Artificial-intelligence fusion that pairs computed tomography with threat-detection algorithms further differentiates high-resolution terahertz modalities. Certification remains the gating item; millimeter-wave incumbents enjoy entrenched compliance status, and terahertz vendors must navigate multi-year testing cycles before aviation adoption crystallizes. Second-order effects reinforce terahertz ascendance. Semiconductor advances are eroding unit cost, and the larger silicon photonics ecosystem is migrating know-how from 5G millimeter-wave components into security imaging. Major primes such as Smiths Detection are integrating DICOS 3.0-compliant interfaces that allow remote analysis of high-capacity data streams, a prerequisite for terahertz imagery. These intersecting technology arcs hint at a plateau for millimeter-wave share before the end of the decade and a gradual pivot toward hybrid deployments that mix mature portals with targeted terahertz add-ons.

Airport checkpoints accounted for 57.52% of revenue in 2025, underscoring their role as the centerpiece of the full-body scanner market. Yet public venues and events are projected to log a 14.59% CAGR as stadiums migrate away from walk-through metal detectors to high-throughput weapons-detection lanes. The full-body scanner market size for sports and entertainment facilities is expanding on the back of contract wins for mobile trailers fitted with millimeter-wave portals capable of screening crowds at 2,500 people per hour. High-profile rollouts at the FIFA Club World Cup 2025, SoFi Stadium, and Rugby World Cup proved that pop-up deployments could blend security with fan-experience imperatives.

Secondary use cases deepen diversification. Correctional facilities now procure portals to interdict narcotics and improvised weapons, while land-border agencies integrate low-energy X-ray portals that rotate between vehicle and pedestrian inspection modes. Corporate campuses are piloting scanners during elevated threat windows or executive events, leasing units for days or weeks rather than purchasing outright. Such variability in contract length invites outcome-based pricing, where vendors charge per scan or per day, thereby smoothing utilization across a traditionally lumpy aviation-centric order book.

Geography Analysis

North America accounted for 37.49% of revenue in 2025, thanks to the Transportation Security Administration's USD 220.6 million capital plan to refresh 1,065 advanced imaging units. Incremental demand now pivots to mega-events such as the FIFA World Cup 2026, where QPS201 portals will address surge throughput. Border agencies complement aviation demand, such as low-energy X-ray portals, which are rolling out at southern crossings under a program exceeding USD 200 million, reflecting a broader homeland-security budget that spans people and cargo. Canada is phasing out Chinese-origin scanners from future tenders, aligning supply chains with allied vendors, while Mexico's multi-year Rapiscan backlog illustrates sustained replacement momentum even in emerging-market fiscal environments.

Asia-Pacific is on track for a 14.71% CAGR, driven by greenfield airport construction, regulatory mandates, and tech-forward screening pilots. South Korea's remote baggage screening link with US authorities compresses minimum connection windows and positions Incheon as a template for trans-Pacific transfers. Australia's mid-2026 computed-tomography deadline is accelerating equipment rollouts in Brisbane, Sydney, and Melbourne. India's mandate for full-body scanners at Tier-1 airports triggers trials at Delhi and will cascade to Bengaluru and Hyderabad as passenger counts climb. Japan is gearing up for Expo 2025 Osaka via phased CT installations at Fukuoka and other airports, aligning with its 60-million-visitor target by 2030. China's digital-twin crowd-management rollouts reveal how data-layer integration can amplify scanner throughput, a model under evaluation in Singapore and Hong Kong.

Europe follows close behind, buoyed by London Heathrow's GBP 1 billion (USD 1.35 billion) CT upgrade and Dubai's 100-scanner order that cements the Gulf Cooperation Council's leadership within the extended European travel corridor. Export-control scrutiny on Chinese equipment, illustrated by Poland's removal of Nuctech portals, is redirecting tenders toward domestic European or allied US vendors. Middle Eastern hubs, especially Dubai and Riyadh, are scaling up CT lanes in anticipation of tourism diversification goals. South America and Africa remain nascent but show green shoots. Brazil's biometric e-gate deployments in 2025-2026 lay the foundation for advanced imaging to be layered on later. Overall, geographic diversification cushions the full-body scanner market against any single-region budget shock.

- OSI Systems, Inc. (Rapiscan Systems)

- Smiths Detection Group Ltd.

- Leidos Security Detection & Automation, Inc.

- Nuctech Company Limited

- Rohde & Schwarz GmbH & Co KG

- Tek84 Engineering Group, LLC

- Thruvision Group plc

- ADANI Systems, Inc.

- NEC Corporation

- Micro-X Limited

- CEIA SpA

- ASTROPHYSICS, Inc.

- Gilardoni S.p.A.

- Westminster Group plc

- VMI Security (VMI Sistemas)

- ISCON Imaging Inc.

- OD Security North America

- Evolv Technologies Holdings, Inc.

- Braun International Ltd.

- Bruker Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aviation Passenger-Volume Rebound

- 4.2.2 Tightening Global Anti-Terrorism Regulations

- 4.2.3 Rapid Decline in Millimeter-Wave Scanner Cost Curve

- 4.2.4 Digital Twin-Enabled Checkpoint Optimisation

- 4.2.5 Rise of Pop-Up Event Security Contracts

- 4.2.6 Emerging Cargo-Plus-People Hybrid Screening

- 4.3 Market Restraints

- 4.3.1 Privacy and Data-Protection Litigation Risk

- 4.3.2 High Capital Expenditure for Mid-Tier Airports

- 4.3.3 Cyber-Vulnerabilities in Connected Scanners

- 4.3.4 Export-Control Restrictions on Dual-Use Technology

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Millimeter-Wave Imaging

- 5.1.2 Backscatter X-ray

- 5.1.3 Terahertz Imaging

- 5.1.4 Dual-Energy Transmission

- 5.1.5 Emerging AI-Fusion Methods

- 5.2 By Application

- 5.2.1 Airport Security Checkpoints

- 5.2.2 Land and Sea Border Crossings

- 5.2.3 Correctional and Detention Facilities

- 5.2.4 Corporate and Critical Infrastructure

- 5.2.5 Public Venues and Events

- 5.3 By Scanner Type

- 5.3.1 Fixed / Portal

- 5.3.2 Walk-Through Gate

- 5.3.3 Portable / Rapid-Deploy

- 5.4 By Component

- 5.4.1 Hardware

- 5.4.2 Software and Analytics

- 5.4.3 Maintenance and Integration Services

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 OSI Systems, Inc. (Rapiscan Systems)

- 6.4.2 Smiths Detection Group Ltd.

- 6.4.3 Leidos Security Detection & Automation, Inc.

- 6.4.4 Nuctech Company Limited

- 6.4.5 Rohde & Schwarz GmbH & Co KG

- 6.4.6 Tek84 Engineering Group, LLC

- 6.4.7 Thruvision Group plc

- 6.4.8 ADANI Systems, Inc.

- 6.4.9 NEC Corporation

- 6.4.10 Micro-X Limited

- 6.4.11 CEIA SpA

- 6.4.12 ASTROPHYSICS, Inc.

- 6.4.13 Gilardoni S.p.A.

- 6.4.14 Westminster Group plc

- 6.4.15 VMI Security (VMI Sistemas)

- 6.4.16 ISCON Imaging Inc.

- 6.4.17 OD Security North America

- 6.4.18 Evolv Technologies Holdings, Inc.

- 6.4.19 Braun International Ltd.

- 6.4.20 Bruker Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment