PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063232

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063232

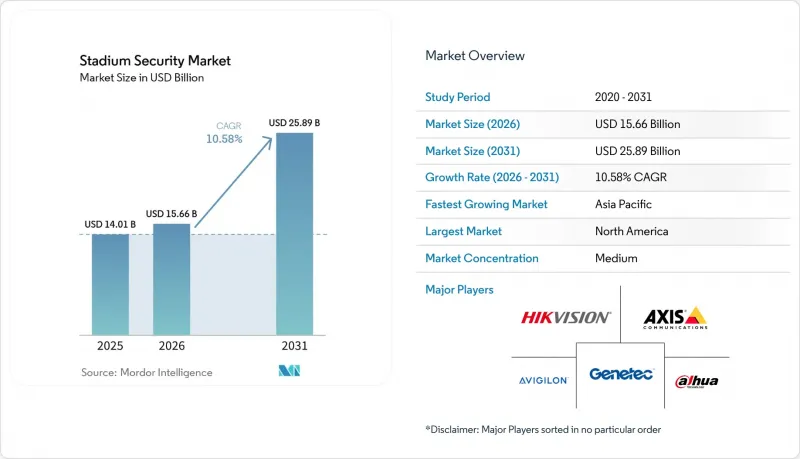

Stadium Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the stadium security market size is projected to expand from USD 14.01 billion in 2025 and USD 15.66 billion in 2026 to USD 25.89 billion by 2031, registering a CAGR of 10.58% between 2026 to 2031.

This report is Segmented by Component (Hardware, Software, and Services), Solution Type (Video Surveillance Systems, Access Control Systems, and More), Deployment Model (On-Premise, and Cloud-Based), Stadium Capacity (Less Than 30, 000 Seats, 30, 000-50, 000 Seats, and Greater Than 50, 000 Seats), and Geography (North America, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Stadium Security Market Trends and Insights

Heightened Terrorism Threat Accelerating Mandatory Security Compliance

The July 2024 Copa America pitch invasion exposed perimeter weaknesses and intelligence gaps, motivating regulators to embed security clauses into hosting contracts. FEMA tied USD 625 million in grants to weapon-detection, counter-drone, and cybersecurity milestones, forcing venues that once planned five-year rollouts to compress projects into 18 months. Insurance carriers now peg premium discounts to AI analytics and biometric access control, ensuring a durable demand baseline even during discretionary-spending pauses.

Rapid Adoption of AI-Powered Video Analytics for Real-Time Threat Detection

AI video analytics that flag unattended bags, crowd surges, and weapon signatures are moving from pilots to mass deployment. Convergint integrated object-recognition software that cut control-room headcount by 60% at multiple U.S. venues. Royal Challengers Bangalore funded 300-plus AI cameras for predictive congestion alerts and facial recognition in January 2026, illustrating Asia-Pacific's leapfrog adoption.

High Upfront CapEx for Integrated Security Suites

A mid-tier stadium, with a capacity of 40,000 seats, allocates a budget of USD 8-12 million for AI cameras, biometrics, intrusion sensors, and a unified command center. However, these stadiums often stagger their purchases due to budget constraints, which creates security gaps and reduces their return on investment (ROI). This fragmented approach to security upgrades can leave vulnerabilities unaddressed for extended periods. In regions like South America and Africa, operators are increasingly turning to incremental upgrades or managed security as-a-service solutions. These strategies help them avoid significant upfront capital expenditures while maintaining a degree of operational security. Such approaches also allow for flexibility in adapting to evolving security needs over time.

Other drivers and restraints analyzed in the detailed report include:

- Government-Funded Smart-Stadium Renovations Ahead of 2026-2028 Mega-Events

- Migration from Analog CCTV to IP/PoE Lowering TCO

- Privacy Regulations Constraining Biometric Deployment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware anchored 61.63% of stadium security market share in 2025 on the back of cameras, turnstiles, and perimeter sensors, yet services are pacing the expansion at 10.78% CAGR to 2031 as venues outsource integration, 24-hour monitoring, and compliance audits. The shift is most visible in facilities under 30,000 seats that lack in-house IT depth and pivot to subscription models for algorithm tuning and incident response.

The services boom aligns with managed-security bundles from Genetec and Convergint that convert capital sales into annuities, while software sits between the two streams, monetizing IP camera migrations with video management licensing and predictive crowd modules. Evolv Technologies' per-scan bag-screening fees illustrate how hardware vendors pivot to consumption economics, extending customer lifetime value without heavy refresh cycles.

Video surveillance accounted for 43.28% of the stadium security market in 2025, cementing cameras as the primary security layer. Cybersecurity, though a smaller slice, is accelerating at 10.91% CAGR because ransomware, distributed denial-of-service risks, and OT network exposures threaten event continuity. Fortinet secured ticketing, point-of-sale, and surveillance networks at FC Barcelona, while Nozomi Networks monitors HVAC controllers for anomalous traffic.

Access control, perimeter detection, and alarm platforms post steady mid-single-digit growth, supported by biometrics mandates in Middle East venues and automated PTZ radar tracking that stretches protection 500 m beyond stadium fences. Insurers require annual penetration testing, effectively hard-wiring cybersecurity demand into lease covenants and sponsorship agreements.

Geography Analysis

North America retained 38.55% stadium security market share in 2025, lifted by FEMA funding, NFL and Major League Baseball security mandates, and a dense integrator ecosystem. MetLife Stadium, SoFi Stadium, and AT&T Stadium all upgraded to AI analytics, biometric gates, and counter-drone radar ahead of FIFA 2026. Canadian and Mexican venues mirror the pattern, with Axis Communications integrating license-plate recognition and facial analytics at Estadio Azteca.

Asia-Pacific, with a 11.31% CAGR, is the fastest-growing region. Royal Challengers Bangalore's January 2026 camera project and China-financed deployments in Southeast Asia underscore how new builds skip analog entirely. Australia is installing counter-UAS systems for the 2032 Brisbane Olympics, and Japan is tying stadium networks into smart-city grids for emergency services. Data-protection fragmentation remains a wild card, particularly in India, where national biometric rules are still pending.

Europe, the Middle East, and Africa show mixed momentum. GDPR fines temper biometric rollouts in Spain and Denmark, but privacy-preserving facial analytics at Paris Saint-Germain reveal a commercial workaround. Saudi Arabia's sovereign-funded 15-stadium initiative positions the Middle East for rapid category adoption, while South America rebuilds confidence after the Copa America breach, with Brazil and Argentina mandating QR ticket checks and expanded guard staffing. African venues proceed gradually, prioritizing incremental upgrades within fiscal constraints.

- Avigilon Corporation

- Genetec Inc.

- Axis Communications AB

- Hangzhou Hikvision Digital Technology Co., Ltd.

- Zhejiang Dahua Technology Co., Ltd.

- Dallmeier Electronic GmbH & Co. KG

- AxxonSoft Limited

- Rapiscan Systems, Inc.

- Evolv Technologies Holdings, Inc.

- Patriot One Technologies Inc. (Xtract One)

- Senstar Corporation

- BriefCam Ltd.

- Hanwha Vision Co., Ltd.

- Bosch Sicherheitssysteme GmbH

- NEC Corporation

- Teledyne FLIR LLC

- Gallagher Group Limited (Security Division)

- IDEMIA Group S.A.S.

- Magal Security Systems Ltd.

- Fortem Technologies, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Heightened Terrorism Threat Accelerating Mandatory Security Compliance

- 4.2.2 Rapid Adoption of AI-Powered Video Analytics for Real-Time Threat Detection

- 4.2.3 Government-Funded Smart-Stadium Renovations Ahead of 2026-2028 Mega-Events

- 4.2.4 Migration from Analog CCTV to IP/PoE Lowering TCO

- 4.2.5 Monetization of Crowd-Flow Data for Sponsor Analytics

- 4.2.6 Temporary Private-5G Network-in-a-Box Kits for Event Security

- 4.3 Market Restraints

- 4.3.1 High Upfront CapEx for Integrated Security Suites

- 4.3.2 Privacy Regulations Constraining Biometric Deployment

- 4.3.3 Shortage of Skilled Security Analysts for AI Platforms

- 4.3.4 RF Congestion from Dense IoT Devices Causing Sensor Interference

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Solution Type

- 5.2.1 Video Surveillance Systems

- 5.2.2 Access Control Systems

- 5.2.3 Perimeter Intrusion Detection Systems

- 5.2.4 Alarm and Notification Systems

- 5.2.5 Cybersecurity and Network Monitoring

- 5.3 By Deployment Model

- 5.3.1 On-Premise

- 5.3.2 Cloud-Based

- 5.4 By Stadium Capacity

- 5.4.1 Less Than 30,000 Seats

- 5.4.2 30,000-50,000 Seats

- 5.4.3 Greater Than 50,000 Seats

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.5 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Avigilon Corporation

- 6.4.2 Genetec Inc.

- 6.4.3 Axis Communications AB

- 6.4.4 Hangzhou Hikvision Digital Technology Co., Ltd.

- 6.4.5 Zhejiang Dahua Technology Co., Ltd.

- 6.4.6 Dallmeier Electronic GmbH & Co. KG

- 6.4.7 AxxonSoft Limited

- 6.4.8 Rapiscan Systems, Inc.

- 6.4.9 Evolv Technologies Holdings, Inc.

- 6.4.10 Patriot One Technologies Inc. (Xtract One)

- 6.4.11 Senstar Corporation

- 6.4.12 BriefCam Ltd.

- 6.4.13 Hanwha Vision Co., Ltd.

- 6.4.14 Bosch Sicherheitssysteme GmbH

- 6.4.15 NEC Corporation

- 6.4.16 Teledyne FLIR LLC

- 6.4.17 Gallagher Group Limited (Security Division)

- 6.4.18 IDEMIA Group S.A.S.

- 6.4.19 Magal Security Systems Ltd.

- 6.4.20 Fortem Technologies, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment