PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063244

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063244

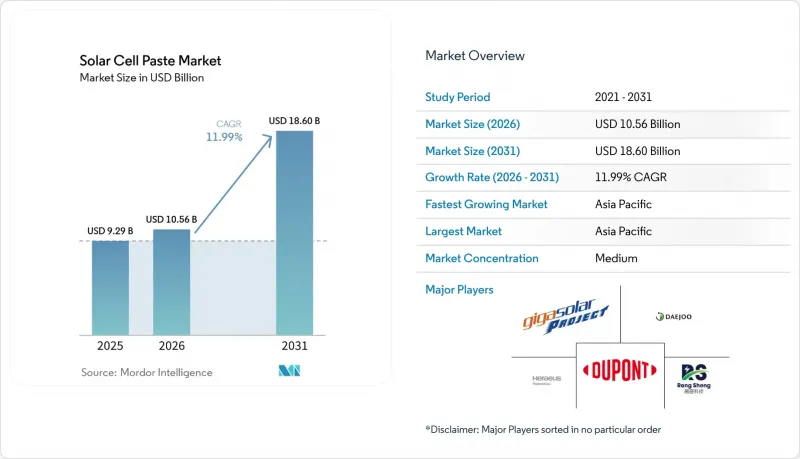

Solar Cell Paste - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the solar cell paste market size is projected to be USD 9.29 billion in 2025, USD 10.56 billion in 2026, and reach USD 18.60 billion by 2031, growing at a CAGR of 11.99% from 2026 to 2031.

This report is Segmented by Type (Silver Paste, Aluminum Paste, and More), Application (Monocrystalline Cells, Polycrystalline Cells, Thin-Film Cells, and More), End-User (Residential, Commercial and Industrial, Utility-Scale, and Off-Grid/Micro-grid) and Geography (North America, Asia-Pacific, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Solar Cell Paste Market Trends and Insights

Relentless PV Capacity Additions in China, India & US Boosting Paste Demand

China alone added 280 GW of new cell capacity during 2024-2025, pushing cumulative capability beyond 800 GW and lifting past consumption as lines run at higher utilization to amortize fixed costs. India's USD 2.4 billion Production-Linked Incentive mandates domestic paste sourcing, catalyzing joint ventures between local cell makers and Korean suppliers. In the United States, the IRA's 45X credit is underwriting a projected climb to 50 GW of annual cell output by 2027, trimming lead times for paste deliveries to 30 days as suppliers commission regional blending plants. Regionalization reduces working capital tied up in inventory by up to 20%, freeing cash for further process upgrades. The driver's impact stays pronounced through 2028, underpinning baseline demand even as per-watt paste loadings decline.

Rapid Shift to PERC, TOPCon & HJT Cells Requiring Higher-Performance Pastes

TOPCon overtook PERC in quarterly capacity additions by late 2025, delivering module efficiencies above 24.5% that justify dual-layer metallization and selective-emitter architectures, which in turn require front-side pastes that achieve contact resistivity under 1.5 mΩ*cm2 and line widths under 25 µm. HJT cells demand low-temperature silver formulations that fire below 200 °C to preserve amorphous-silicon layers; REC Solar and Huasun expect 10 GW of combined HJT capacity online by end-2026. These tighter specs limit qualified suppliers to fewer than 10 globally, consolidating purchasing around Heraeus, DuPont, and Giga Solar. As manufacturers pivot, paste vendors investing in rheology control and nano-silver dispersion secure premium pricing and longer-term contracts, cushioning margin pressure from silver volatility.

Silver Price Volatility Enlarging Cost Risk for Cell Makers

Silver rallied 76% from January 2025 to January 2026, then retraced to USD 2.65-2.90 per g by March 2026, forcing Tongwei, LONGi, and JA Solar to book USD 1.1 billion in combined Q1 2026 losses tied to unhedged silver exposure. Paste suppliers now offer fixed-price contracts indexed to three-month forwards, but these shift commodity risk upstream, compressing supplier gross margins by up to 200 bps. To cope, average silver consumption dropped from 110 mg to 92 mg per wafer between 2023 and 2025 through finer screen meshes. Volatility, therefore, reduces revenue predictability and accelerates the uptake of thrifting technologies.

Other drivers and restraints analyzed in the detailed report include:

- IRA, REPowerEU & Localization Schemes Spurring New Paste Lines Outside Asia

- Cost-Down Race Driving Silver-Coated-Copper & Low-Temp Pastes Uptake

- Accelerated Silver-Thrifting & Copper Plating Threaten Paste Volumes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silver Paste captured 70.1% of the solar cell paste market share in 2025, underpinned by its high conductivity and broad qualification across PERC, TOPCon, and HJT. The segment's dominance shields near-term revenues, yet silver volatility and regulatory headwinds limit upside. Lead-Free Multi-Metal Paste is forecast to post a 14.1% CAGR, benefiting from EU REACH and China's GB/T 38597 mandates; Sn-Ag-Cu blends add roughly 10% to production cost but remove compliance risk. Aluminum Paste remains relevant for Al-BSF cells in utility-scale projects, though share erodes as TOPCon spreads. Copper and silver-coated copper pastes present high upside if adhesion and migration challenges are solved.

Suppliers are aligning portfolios accordingly. Heraeus and DuPont funnel R&D into low-temperature nano-silver dispersions for HJT, leveraging 20-25% price premiums. Chinese contenders like Giga Solar double down on aluminum and conventional silver pastes aimed at price-sensitive gigawatt farms. Early certification of lead-free blends offers first-mover advantage in Europe's tightening policy environment, while silver-coated-copper pilots act as an option on future cost shocks. Competitive positioning, therefore, hinges on parallel bets across premium-efficiency and cost-optimized formulations, with IP around sintering additives and wetting agents forming key moats.

Geography Analysis

Asia-Pacific controlled 62.7% of the solar cell paste market share in 2025 and is expanding at a 13.4% CAGR to 2031, fueled by China's plan for 500 GW of additional PV by 2030 and India's National Solar Mission target of 280 GW. Jiangsu, Zhejiang, and Anhui house over 60% of global cell capacity, concentrating paste demand and enabling economies of scale. India's domestic-content rules have already lured Daejoo Electronic Materials and Giga Solar into Gujarat and Tamil Nadu joint ventures, trimming logistics lead times from 90 days to 30 days. South Korea and Japan, though smaller in volume, drive innovation in low-temperature HJT pastes, supported by extensive semiconductor materials expertise.

North America's share is set to rise rapidly through 2028 as the IRA's 45X credit propels U.S. cell capacity from 8 GW in 2023 to a forecast 50 GW by 2027, bringing with it localized paste demand. DuPont's North Carolina line and Heraeus's Ohio tech center illustrate first-mover capture of this resurgent market. Europe, targeting 30 GW per annum under REPowerEU, faces a manufacturing gap; local paste consumption therefore hinges on the success of intra-EU cell projects led by Meyer Burger and Enel Green Power. Still, the regulatory push for lead-free formulations positions European plants at the forefront of Sn-Ag-Cu adoption.

The Middle East and Africa are emerging growth zones. Saudi Arabia's Vision 2030 aims for 20 GW of solar, prompting Heraeus to open a Riyadh service hub in 2026. The UAE's 5 GW Al Dhafra farm and South Africa's procurement rounds will lift regional paste imports, though domestic manufacturing remains nascent. South America, led by Brazil and Chile, imports most cells but could catalyze future blending facilities if local content rules tighten. Collectively, these geographies diversify revenue streams, but Asia-Pacific will remain the anchor of the solar cell paste market through at least 2031.

- Heraeus Photovoltaics

- DuPont Microcircuit Materials

- Giga Solar Materials

- Rutech

- Daejoo Electronic Materials

- Samsung SDI

- Alpha Assembly (MacDermid Alpha)

- Dongjin Semichem

- InkTec

- Toyo Aluminium K.K.

- Monocrystal

- Ferro Corporation

- Targray

- Henkel AG & Co. KGaA

- Heraeus Noblelight (infra-red sintering)

- Pastetech GmbH

- Xi'an Hongxing Electronic Paste

- Jiangsu Hoyi Technology

- Hunan LEED Advanced Material

- Heraeus ShenZhen (local JV)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Relentless PV capacity additions in China, India & US boosting paste demand

- 4.2.2 Rapid shift to PERC, TOPCon & HJT cells that require higher-performance front & rear pastes

- 4.2.3 IRA, REPowerEU & similar localisation schemes spurring new paste lines outside Asia

- 4.2.4 Cost-down race driving silver-coated-copper & low-temp pastes uptake

- 4.2.5 Surge in perovskite-tandem R&D demanding screen-printable conductive inks

- 4.3 Market Restraints

- 4.3.1 Silver price volatility enlarging cost risk for cell makers

- 4.3.2 Accelerated silver-thrifting & copper plating threaten paste volumes

- 4.3.3 Tighter lead-based frit regulations raising reformulation costs

- 4.3.4 High supplier concentration limits buyers' bargaining power

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Silver Paste

- 5.1.2 Aluminum Paste

- 5.1.3 Copper Paste

- 5.1.4 Silver-Coated-Copper Paste

- 5.1.5 Lead-Free Multi-Metal Paste

- 5.2 By Application

- 5.2.1 Monocrystalline Cells

- 5.2.2 Polycrystalline Cells

- 5.2.3 Thin-Film Cells

- 5.2.4 Heterojunction (HJT) Cells

- 5.2.5 Perovskite and Tandem Cells

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial and Industrial

- 5.3.3 Utility-Scale

- 5.3.4 Off-Grid/Micro-grid

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 NORDIC Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Heraeus Photovoltaics

- 6.4.2 DuPont Microcircuit Materials

- 6.4.3 Giga Solar Materials

- 6.4.4 Rutech

- 6.4.5 Daejoo Electronic Materials

- 6.4.6 Samsung SDI

- 6.4.7 Alpha Assembly (MacDermid Alpha)

- 6.4.8 Dongjin Semichem

- 6.4.9 InkTec

- 6.4.10 Toyo Aluminium K.K.

- 6.4.11 Monocrystal

- 6.4.12 Ferro Corporation

- 6.4.13 Targray

- 6.4.14 Henkel AG & Co. KGaA

- 6.4.15 Heraeus Noblelight (infra-red sintering)

- 6.4.16 Pastetech GmbH

- 6.4.17 Xi'an Hongxing Electronic Paste

- 6.4.18 Jiangsu Hoyi Technology

- 6.4.19 Hunan LEED Advanced Material

- 6.4.20 Heraeus ShenZhen (local JV)

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment