PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063255

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063255

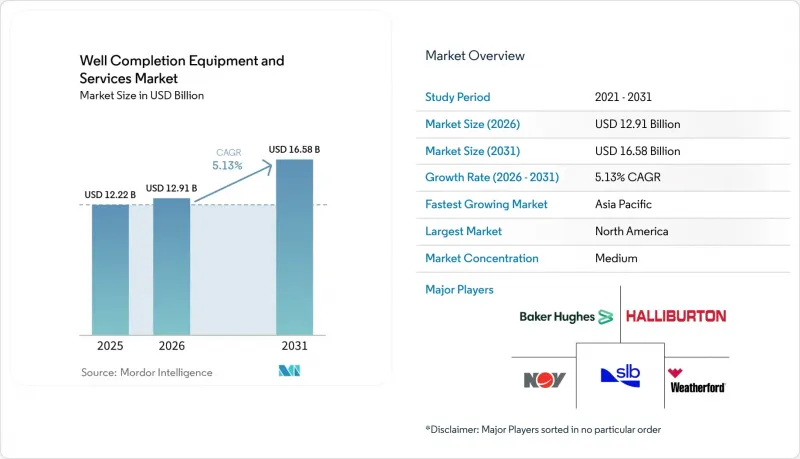

Well Completion Equipment and Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the well completion equipment and Services Market size is projected to expand from USD 12.22 billion in 2025 and USD 12.91 billion in 2026 to USD 16.58 billion by 2031, registering a CAGR of 5.13% between 2026 to 2031.

This report is Segmented by Type (Equipment: Packers, Sand-Control Tools, Multi-Stage Fracturing Tools, Liner Hangers, Valves and Others; Services: Hydraulic Fracturing, and More), Well Type (Conventional, Unconventional), Application (Onshore, Offshore), and Geography (North America, Europe, and Others). The Market Forecasts are Provided in Terms of Value (USD).

Global Well Completion Equipment and Services Market Trends and Insights

Rise in Global Drilling Activities

International rig counts climbed to 1,112 units in early 2025, adding 15 rigs year-on-year even as North American activity contracted, highlighting a pivot toward state-owned operators in the Middle East and Asia that prioritize energy security over short-cycle returns. Saudi Aramco's Jafurah start-up and ADNOC Drilling's USD 1 billion fleet expansion underline this trend. Deeper, hotter wells are driving demand for HPHT-rated packers, corrosion-resistant liner hangers, and multi-stage fracturing tools, pushing lead times to 26 weeks in late 2025. Completion revenue is therefore rising faster than rig count because every well consumes more value-added hardware. ONGC's Krishna-Godavari cluster evidences the capital intensity, with roughly USD 69 million spent per well, most of which funds completion hardware and subsea tie-backs.

Increasing Focus on Unconventional Reserves

Unconventional plays are expanding at 6.9% annually as Argentina, Saudi Arabia, and China replicate North American shale economics. Vaca Muerta executed 23,784 fracturing stages in 2025, up 34% year-on-year, and will require another 1,000 wells by 2032 to meet domestic and LNG commitments. Saudi Aramco's Jafurah aims for 2 billion scf/d of gas by 2030 from carbon-lite electric frac fleets, while China's Sichuan and Ordos basins employ fiber-optic monitoring to trim completion time by 18%. Localized supply chains and state financing are smoothing learning curves, allowing the well-completion equipment and services market to diversify beyond North America.

Volatile Crude-Oil Prices

Brent averaged USD 69/bbl in 2025 before spiking to USD 94 in March 2026, a 36% swing that compressed completion budgets as listed E&Ps held spending flat despite higher prices. Day rates for hydraulic fracturing slipped 8% in Q1 2026 even as diesel costs rose, squeezing pressure-pumper margins. Offshore projects are less price-sensitive because multi-year commitments insulate completion schedules, yet exploration budgets and the future pipeline of wells remain tied to price sentiment.

Other drivers and restraints analyzed in the detailed report include:

- Electrified Frac Fleets Reduce OpEx/CO2

- Repurposing Completions for CCUS and Geothermal Wells

- HPHT-Grade Elastomer and Alloy Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services revenue is projected to grow at a 6.8% CAGR to 2031 as operators outsource hydraulic fracturing, wireline, and zonal isolation. Liberty's USD 727 million Q3 2025 revenue highlights demand for e-frac fleets that save 30% in fuel. Wireline is evolving into an intelligent-perforation service, with Schlumberger's ReSOLVE iX platform reducing non-productive time by 12%. Gravel-packing demand is climbing in deepwater wells where sand control protects billion-dollar investments.

Equipment maintained a 54.4% share of the well completion equipment and services market size in 2025, fueled by packers, multi-stage fracturing tools, and liner hangers, yet growth is slowing as refurbishment programs increasingly extend tool lifespans and decrease replacement frequency. NOV logged USD 420 million in completion-equipment orders for Q4 2025, mainly from subsea systems destined for Guyana and Brazil. Suppliers able to pivot into HPHT and subsea niches or bundle installation services stand to defend margins.

Geography Analysis

North America maintained a 40.3% share in 2025, yet basin-level divergence is widening. The Permian sustains momentum with longer laterals and e-frac adoption that lowers emissions ahead of EPA methane fees, while the Bakken and Eagle Ford contract as operators prioritize free cash flow. Canada's Montney and Duvernay programs rely on high-rate pumping and dissipate completion dollars into LNG export value chains.

Asia-Pacific is the fastest-growing region at 7.2%. CNOOC's Wenchang 16-2, Weizhou 11-4, and Panyu expansions added more than 100,000 boe/d in 2025 through subsea completions equipped with sand-control screens and HPHT packers, while ONGC's Krishna-Godavari cluster produced 25,000 b/d from eight wells and a USD 477.28 million investment . Indonesian and Malaysian unconventional gas targets are driving collaboration accords, such as Pertamina's 2025 pact with Halliburton to automate completions.

The Middle East and Africa revolve around Aramco's Jafurah and ADNOC's SARB deep-gas buildouts, along with TechnipFMC's integrated subsea work in West Africa. ADNOC Drilling plans to expand its fleet to 151 rigs by 2028 after investing more than USD 1 billion in 2025, signaling longer-term completion demand beyond oil recovery. South America's Vaca Muerta remains a bright spot, with a 34% annual jump in fracture stages and cross-border gas sales approved to Petrobras, ensuring sustained activity through the decade.

- Schlumberger

- Halliburton

- Baker Hughes

- Weatherford

- NOV

- TechnipFMC

- Superior Energy Services

- Trican Well Service

- Nine Energy Service

- TAM International

- Liberty Oilfield Services

- NexTier Oilfield Solutions

- Calfrac Well Services

- FTS International

- Packers Plus Energy Services

- Welltec

- Archer Limited

- Patterson-UTI Pressure Pumping

- Core Laboratories

- CNPC Chuanqing Drilling & Completion

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in global drilling activities

- 4.2.2 Increasing focus on unconventional reserves

- 4.2.3 Growing demand for advanced well-completion techniques

- 4.2.4 Offshore deep-water CAPEX rebound

- 4.2.5 Electrified frac fleets reduce OpEx/CO2

- 4.2.6 Repurposing completions for CCUS and geothermal wells

- 4.3 Market Restraints

- 4.3.1 Volatile crude-oil prices

- 4.3.2 Environmental and regulatory stringency

- 4.3.3 HPHT-grade elastomer and alloy shortages

- 4.3.4 Data-platform interoperability gaps

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Equipment

- 5.1.1.1 Packers

- 5.1.1.2 Sand-control tools

- 5.1.1.3 Multi-stage fracturing tools

- 5.1.1.4 Liner hangers

- 5.1.1.5 Valves and others

- 5.1.2 Services

- 5.1.2.1 Hydraulic fracturing

- 5.1.2.2 Wireline services

- 5.1.2.3 Perforating

- 5.1.2.4 Gravel packing

- 5.1.2.5 Zonal-isolation services

- 5.1.1 Equipment

- 5.2 By Well Type

- 5.2.1 Conventional

- 5.2.2 Unconventional

- 5.3 By Application

- 5.3.1 Onshore

- 5.3.2 Offshore

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 NORDIC Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Schlumberger

- 6.4.2 Halliburton

- 6.4.3 Baker Hughes

- 6.4.4 Weatherford

- 6.4.5 NOV

- 6.4.6 TechnipFMC

- 6.4.7 Superior Energy Services

- 6.4.8 Trican Well Service

- 6.4.9 Nine Energy Service

- 6.4.10 TAM International

- 6.4.11 Liberty Oilfield Services

- 6.4.12 NexTier Oilfield Solutions

- 6.4.13 Calfrac Well Services

- 6.4.14 FTS International

- 6.4.15 Packers Plus Energy Services

- 6.4.16 Welltec

- 6.4.17 Archer Limited

- 6.4.18 Patterson-UTI Pressure Pumping

- 6.4.19 Core Laboratories

- 6.4.20 CNPC Chuanqing Drilling & Completion

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment