PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063260

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063260

Capacitor Bank - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

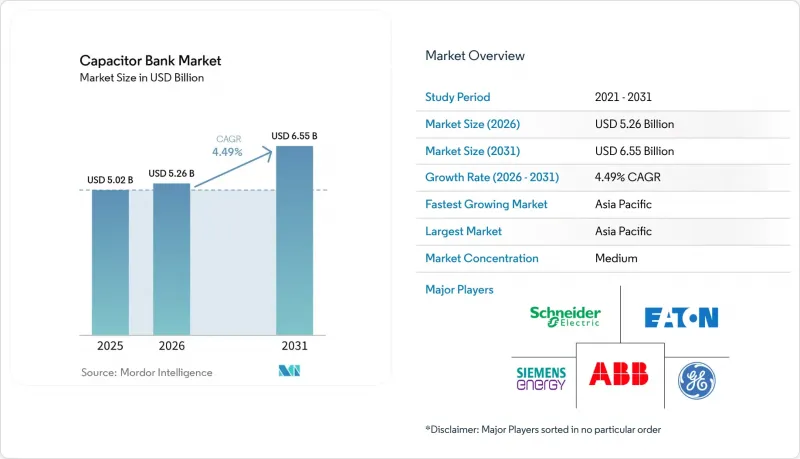

According to Mordor Intelligence, the capacitor bank market size is expected to increase from USD 5.02 billion in 2025 to USD 5.26 billion in 2026 and reach USD 6.55 billion by 2031, growing at a CAGR of 4.49% over 2026-2031.

This report is Segmented by Type (Open Air Substation, Others), Voltage Class (Low-Voltage Below 10 KV, Medium-Voltage 10 To 69 KV, High-Voltage Above 69 KV), Application (Power Factor Correction, Others), End-User (Utilities, Commercial, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Capacitor Bank Market Trends and Insights

Grid-modernization & DER build-out

Utilities worldwide are hardening grids to accommodate bidirectional flows from rooftop solar, community batteries, and utility-scale renewables. MISO's 2025 plan alone earmarks USD 12.3 billion for 432 projects that include 97 MVAr of new or relocated capacitor capacity across Minnesota and Iowa substations. Southern California Edison is embedding automated capacitor-bank controllers across its distribution feeders to manage midday voltage climb caused by distributed photovoltaics. Eversource Energy has budgeted USD 16.2 billion through 2028, with a portion dedicated to var-dispatch upgrades that allow second-level switching in response to behind-the-meter storage injections. These programs convert the capacitor bank market from a replacement cycle to an expansion cycle because each new feeder section now needs local var support. Suppliers offering turnkey enclosures with SCADA interfaces and health-monitoring diagnostics are positioned to win multiyear framework agreements with transmission system operators.

Surge in EV Charging Infrastructure

Fast chargers impose lagging power factors as low as 0.85, forcing utilities to mandate on-site compensation when connected load exceeds 1 MW. IEEE field tests show a 350 kW charger can draw 100 kVAr, equivalent to the reactive demand of 20 homes. CAISO's 2025-2026 study specifies series-capacitor insertion on two 70 kV corridors to counteract Bay-Area charging-related voltage sag. Property developers, therefore, purchase low-voltage capacitor cabinets that commission in weeks without utility studies, a niche where Schneider Electric and Eaton compete on delivery speed. As vehicle adoption accelerates, a dual-channel opportunity emerges: utilities procure medium-voltage banks for feeder stiffening, while charging-network operators buy modular units for depot installations.

MLCC supply-chain volatility spilling into film capacitors

AI-server demand pulled multilayer ceramic capacitor (MLCC) production toward high-capacitance grades, reducing metallization capacity for film devices. Supplyframe recorded 52-week MLCC lead times in early 2024, and TTI reported film-capacitor lead times stretching to 19 weeks in late 2025, up 46% from pre-pandemic norms. Smaller capacitor-bank assemblers without strategic sourcing contracts face component shortages that delay project commissioning. Mitigation hinges on dual-sourcing and long-term volume agreements, advantages enjoyed by Tier 1 vendors but not readily available to regional specialists.

Other drivers and restraints analyzed in the detailed report include:

- Electrification of Heat-Intensive Industries

- Rising Power-Quality Penalties from Utilities

- Slow Utility Cap-Ex Cycles in Price-Controlled Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal-enclosed assemblies accounted for a growing slice of the capacitor bank market in 2025 and are projected to grow at a 5.7% CAGR as urban utilities prioritize compact, fire-rated gear. Open-air yards still represent 42.7% of installations because rural substations have ample land, but their growth lags under tightening environmental constraints. Pole-mounted units remain popular in rural feeders where linemen can service equipment without pad construction. Other mobile or containerized banks address temporary grid reinforcement at construction sites and mines, creating a niche for plug-and-play cabinets that deploy within days.

Urban densification in California, Germany, and Singapore accelerates demand for indoor-rated designs that co-locate with switchgear. The Plainfield substation in California added two 5 MVAr metal-enclosed banks in March 2026 to meet wildfire regulations, illustrating how the capital premium is offset by avoided containment berms. Suppliers differentiate through stainless-steel housings, arc-fault venting, and integrated relay panels. Although type choice often aligns with voltage, hybrid yards that mix open-air reactors with enclosed capacitor steps are emerging as a cost-optimized middle ground.

Medium-voltage banks (10 kV-69 kV) generated 47.9% of revenue in 2025 and are forecast to expand at 4.8% CAGR, reflecting their role in feeder voltage regulation and wind-farm collector systems. Low-voltage units (< 10 kV) dominate building-level corrections in data centers and hospitals, where facility managers rather than utility engineers drive purchase decisions. High-voltage banks (> 69 kV) grow slowly as STATCOMs and series capacitors gain favor in transmission corridors, yet they persist in remote substations lacking the maintenance bandwidth for power electronics.

The capacitor bank market size for medium-voltage equipment is projected to rise steadily because each new DER-rich feeder requires multi-step banks to stabilize voltage. Conversely, high-voltage banks defend pockets where STATCOM economics falter, such as sparsely populated deserts or mountain passes. Vendors offering seismic-rated designs and cybersecurity-hardened controllers capture share as utilities layer new specifications onto legacy IEC 60871 compliance.

Geography Analysis

Asia-Pacific generated 45.2% of 2025 revenue and will sustain a 5.2% CAGR through 2031 as China extends its ultra-high-voltage network and India builds renewable corridors. China's Jiayuguan NingSheng hybrid storage project, commissioned in December 2025, illustrates the hybridization trend in which capacitor banks manage steady-state vars while supercapacitors address transients. India's Power Grid contract with Hitachi Energy for 30 units of 765 kV transformers underscores continued grid expansion that necessitates substantial shunt capacitance.

North America grows more slowly because the installed base is mature, and regulated utilities follow lengthy approval cycles. MISO's USD 12.3 billion 2025 expansion plan still contains dozens of medium-voltage banks, and PG&E's Plainfield project adds 10 MVAr of enclosed capacity to meet wildfire-hardening rules. Data-center buildouts in Texas and Virginia create demand for low-voltage automatic banks, but STATCOM substitution limits upside in transmission corridors.

Europe favors dynamic compensators for offshore wind integration, yet urban utilities in Germany and the Nordics still procure medium-voltage banks for space-constrained substations. Ofgem's doubled network charges push U.K. industrial customers to install on-site banks and avoid penalties. L&T's involvement in North Sea HVDC hubs signals future orders for converter-station shunt capacitors.

South America and the Middle East remain niche, driven by renewable auctions in Brazil and storage tenders in Saudi Arabia. Tariff-constrained utilities defer replacements, so vendors focus on industrial electrification projects and battery-storage partnerships that bundle var support into EPC packages.

- ABB Ltd

- Siemens Energy AG

- Schneider Electric SE

- Eaton Corporation plc

- General Electric Co.

- Arteche Group

- Larsen & Toubro Limited

- Hitachi Energy Ltd

- Mitsubishi Electric Corp.

- Toshiba Energy Systems & Solutions

- CG Power & Industrial Solutions

- Hyosung Heavy Industries

- Nissin Electric Co. Ltd

- Trench Group (Siemens)

- Kondas Elektrik Kapasitor

- ZEZ Silko s.r.o.

- FRANKLIN Grid Solutions

- Enerlux Power SRL

- Samwha Electric Co. Ltd

- Cooper Power Systems (Eaton)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Grid-modernisation & DER build-out

- 4.2.2 Surge in EV charging infrastructure

- 4.2.3 Electrification of heat-intensive industries

- 4.2.4 Rising power-quality penalties from utilities

- 4.2.5 Breakthroughs in dry-type polypropylene film

- 4.2.6 AI-enabled predictive switching of capacitor banks

- 4.3 Market Restraints

- 4.3.1 MLCC supply-chain volatility spilling into film capacitors

- 4.3.2 Slow utility cap-ex cycles in price-controlled regions

- 4.3.3 Fire-event recalls in oil-impregnated banks

- 4.3.4 Increasing competition from STATCOMs & SVCs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Open air substation

- 5.1.2 Metal enclosed substation

- 5.1.3 Pole mounted

- 5.1.4 Others

- 5.2 By Voltage Class

- 5.2.1 Low-Voltage (Below 10 kV)

- 5.2.2 Medium-Voltage (10 to 69 kV)

- 5.2.3 High-Voltage (Above 69 kV)

- 5.3 By Application

- 5.3.1 Power factor correction

- 5.3.2 Harmonic filter

- 5.3.3 Voltage regulation

- 5.3.4 Renewable integration

- 5.3.5 Industrial application

- 5.3.6 Data centers

- 5.3.7 Others

- 5.4 By End-User

- 5.4.1 Utilities

- 5.4.2 Commercial

- 5.4.3 Industrial

- 5.4.4 Residential

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 ABB Ltd

- 6.4.2 Siemens Energy AG

- 6.4.3 Schneider Electric SE

- 6.4.4 Eaton Corporation plc

- 6.4.5 General Electric Co.

- 6.4.6 Arteche Group

- 6.4.7 Larsen & Toubro Limited

- 6.4.8 Hitachi Energy Ltd

- 6.4.9 Mitsubishi Electric Corp.

- 6.4.10 Toshiba Energy Systems & Solutions

- 6.4.11 CG Power & Industrial Solutions

- 6.4.12 Hyosung Heavy Industries

- 6.4.13 Nissin Electric Co. Ltd

- 6.4.14 Trench Group (Siemens)

- 6.4.15 Kondas Elektrik Kapasitor

- 6.4.16 ZEZ Silko s.r.o.

- 6.4.17 FRANKLIN Grid Solutions

- 6.4.18 Enerlux Power SRL

- 6.4.19 Samwha Electric Co. Ltd

- 6.4.20 Cooper Power Systems (Eaton)

7 Market Opportunities & Future Outlook