PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063278

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063278

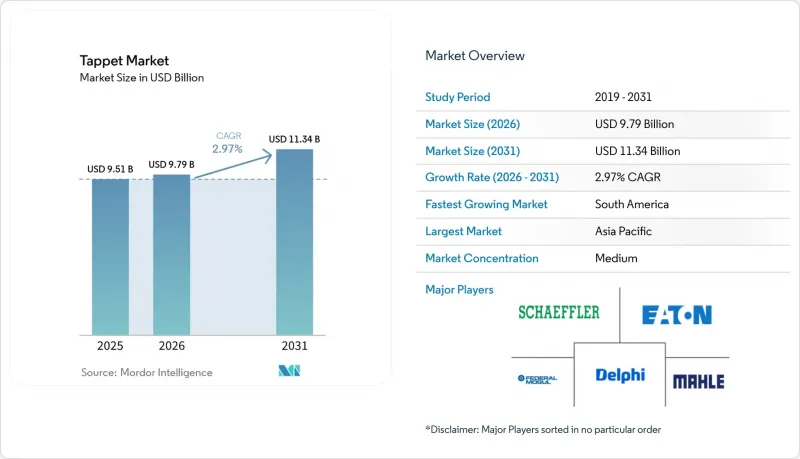

Tappet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the tappet market size was valued at USD 9.51 billion in 2025 and estimated to grow from USD 9.79 billion in 2026 to reach USD 11.34 billion by 2031, at a CAGR of 2.97% during the forecast period (2026-2031).

This report is Segmented by Type (Flat Tappets, Roller Tappets, and More), Engine Capacity (Below 4 Cylinders, 4-6 Cylinders, and More), Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, and More), Distribution Channel (OEM and Aftermarket), Fuel Type (Gasoline, Diesel, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Tappet Market Trends and Insights

Expanding Production of ICE Vehicles in Asia-Pacific

China's continued diesel-engine build rates and India's fresh investment pipeline are sustaining tappet demand despite battery-electric adoption. Japanese exporters are strengthening links with ASEAN plants, securing long-run orders for precision-ground components. Regional suppliers such as Schaeffler India have commissioned new facilities to comply with rising local content requirements. Hybrid penetration keeps full valvetrain architectures in upcoming models, cushioning the market from pure-EV substitution. The result is a stable growth platform that anchors long-term volume in the tappet market.

Stricter Global Emission Norms Heightening Demand for Precision Valvetrain Components

Euro 7 standards taking effect in 2027 mandate tighter real-world compliance, encouraging hydraulic roller followers that hold lash within 0.05 mm tolerances. China's National VI-b rules have already accelerated the adoption of roller designs in small turbocharged engines. U.S. fleet-average targets are likewise steering engineers toward low-friction tappets to unlock incremental fuel savings. These norms elevate the component from a commodity to a calibrated subsystem. Suppliers able to document precision across temperature swings gain a clear pricing premium.

Rapid Penetration of Battery-Electric Vehicles (ICE Displacement)

Battery-electric models continue to compress the total addressable base of internal-combustion powertrains, particularly in China and the European Union, where consumer incentives and regulatory deadlines overlap. Passenger-car segments that once relied on high-volume four-cylinder engines are shifting toward full electrification, removing entire valvetrain assemblies from their bill of materials. Meanwhile, North America is seeing similar momentum as state-level mandates nudge automakers toward zero-emission fleets. Even so, hybrid drivetrains preserve conventional tappets, softening the blow in regions where charging infrastructure remains uneven.

Other drivers and restraints analyzed in the detailed report include:

- Growing OEM Shift from Mechanical to Hydraulic/Roller Tappets

- Micro-Hybrid Stop-Start Durability Requirements

- Volatility in Specialty Alloy and Tool-Steel Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hydraulic tappets commanded 40.43% of the tappet market share in 2025, reflecting automakers' preference for self-adjusting lash control that minimizes maintenance needs. Recent design iterations pair hydraulic function with diamond-like carbon coatings to reduce wear during cold starts, helping keep warranty claims in check. Industry conversations reveal that service departments value the quieter operation such designs deliver, which improves perceived vehicle quality. Flat mechanical lifters now occupy niche roles in classic performance rebuilds where simplicity trumps refinement. Component suppliers are therefore prioritizing hydraulic inventory while supporting legacy formats for specialized aftermarket channels.

Roller tappets, projected to grow at a 2.99% CAGR through 2031, gain traction as friction-reduction mandates sharpen. Their needle-bearing interfaces lessen sliding contact, freeing incremental efficiency that helps meet tightening fleet targets. Engineers also cite lower oil-temperature rise and extended drain intervals as secondary benefits. Adoption accelerates when new engine programs combine overhead cams with direct injection, a pairing that magnifies the payoff from reduced valvetrain losses. As plant tooling amortizes, more mid-cycle refreshes switch to roller profiles, creating a steady conversion pipeline across vehicle classes.

Powerplants with 4-to-6 cylinders accounted for 53.32% of the tappet market share in 2025, largely because this configuration underpins global best-selling models in the passenger and light-commercial segments. Design teams favor a balance between displacement and fuel economy, which translates into long production cycles and stable parts procurement. Aftermarket catalogs mirror this dominance, stocking a broad mix of hydraulic and roller formats tailored to regional fuel qualities. Training programs for independent repair shops therefore focus their curricula around these mainstream engines, reinforcing installed-base advantages. Suppliers in emerging economies often start with mid-range lifter lines before expanding into other capacities.

Engines with more than 6 cylinders are expected to post a 3.01% CAGR, driven by medium- and heavy-duty trucks that continue to use diesel or natural gas combustion. Fleet operators depend on proven longevity, making them receptive to premium roller lifters with advanced coatings that withstand extended service intervals. Regulations on particulate matter continue to tighten, yet high-torque freight requirements leave few realistic electrification alternatives over long distances. Ongoing investments in alternative fuels, such as hydrogen-ready engines, may further increase lifter complexity without reducing overall counts.

Geography Analysis

Asia-Pacific retained the largest share of tappet demand at 47.18% in 2025, supported by steady internal-combustion vehicle output and widening hybrid penetration. Regional suppliers benefit from vertically integrated casting and heat-treatment lines that shorten lead times for local automakers. Policy frameworks encourage content localization, prompting fresh capacity additions across India, Thailand, and Vietnam. Component exports from Japan into the broader ASEAN bloc continue to rise as manufacturers seek tariff-free corridors inside the Regional Comprehensive Economic Partnership.

South America is forecast to post the fastest regional growth at a 4.13% CAGR through 2031, buoyed by the June 2025 Brazil-Argentina automotive accord, which removed tariffs on strategic powertrain parts. The agreement obliges vehicle assemblers to reinvest in local research facilities, channeling engineering budgets toward materials and coatings suited to high-ethanol blends. Flex-fuel technology dominates the Brazilian passenger-car fleet, driving steady demand for hardened tappets that withstand corrosive exhaust chemistry. Argentina's truck makers leverage the tariff reprieve to source valvetrain components regionally rather than import from Europe, adding resilience to local supply chains.

North America and Europe continue to generate significant volume even as electrification accelerates. Hybrid and range-extended platforms in both regions still rely on conventional cam-driven architectures, safeguarding baseline lifter consumption. Tightening Euro 7 legislation compels European OEMs to adopt precision roller designs that meet real-world emissions limits. At the same time, U.S. commercial fleets favor durability-oriented lifters specified for long-haul diesel engines. Meanwhile, material-price volatility has prompted many Tier 1 suppliers to expand domestic machining capacity, insulating programs from the effects of geopolitical steel shortages. Collectively, these factors sustain demand in mature markets even as the share of battery-electric vehicles edges upward.

- Schaeffler Group

- Eaton Corporation

- Delphi Technologies

- Riken Corporation

- Federal-Mogul (Tenneco Inc.)

- MAHLE GmbH

- NSK Ltd.

- TRW Automotive

- Otics Corporation

- COMP Cams

- Johnson Lifters

- Crower Cams & Equipment Co., Ltd.

- SM Motorenteile GmbH

- Wuxi Xizhou Machinery Co., Ltd.

- Zhejiang Huiyu Auto Parts Co., Ltd.

- ACDelco (General Motors)

- ISKY Racing Cams

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Production of ICE Vehicles in Asia-Pacific

- 4.2.2 Stricter Global Emission Norms Heightening Demand for Precision Valvetrain Components

- 4.2.3 Growing OEM Shift from Mechanical to Hydraulic/Roller Tappets

- 4.2.4 Micro-Hybrid Stop-Start Durability Requirements

- 4.2.5 Rising Aftermarket Demand for Performance Cam-Train Retrofits

- 4.2.6 Bio-Fuel Compatibility Pushing Coated Lightweight Tappets

- 4.3 Market Restraints

- 4.3.1 Rapid Penetration of Battery-Electric Vehicles (ICE Displacement)

- 4.3.2 Volatility in Specialty Alloy and Tool-Steel Prices

- 4.3.3 Emerging Cam-Less Electro-Hydraulic Actuation

- 4.3.4 Tool-Steel Supply-Chain Disruptions from Geopolitical Risks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 Flat Tappets

- 5.1.2 Roller Tappets

- 5.1.3 Mechanical Tappets

- 5.1.4 Hydraulic Tappets

- 5.1.5 Pneumatic Tappets

- 5.2 By Engine Capacity

- 5.2.1 Below 4 Cylinders

- 5.2.2 4-6 Cylinders

- 5.2.3 Above 6 Cylinders

- 5.3 By Vehicle Type

- 5.3.1 Passenger Vehicles

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Medium and Heavy Commercial Vehicles

- 5.4 By Distribution Channel

- 5.4.1 Original Equipment Manufacturer (OEM)

- 5.4.2 Aftermarket

- 5.5 By Fuel Type

- 5.5.1 Gasoline

- 5.5.2 Diesel

- 5.5.3 LPG/CNG

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 Spain

- 5.6.3.4 Italy

- 5.6.3.5 France

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 India

- 5.6.4.2 China

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Egypt

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Schaeffler Group

- 6.4.2 Eaton Corporation

- 6.4.3 Delphi Technologies

- 6.4.4 Riken Corporation

- 6.4.5 Federal-Mogul (Tenneco Inc.)

- 6.4.6 MAHLE GmbH

- 6.4.7 NSK Ltd.

- 6.4.8 TRW Automotive

- 6.4.9 Otics Corporation

- 6.4.10 COMP Cams

- 6.4.11 Johnson Lifters

- 6.4.12 Crower Cams & Equipment Co., Ltd.

- 6.4.13 SM Motorenteile GmbH

- 6.4.14 Wuxi Xizhou Machinery Co., Ltd.

- 6.4.15 Zhejiang Huiyu Auto Parts Co., Ltd.

- 6.4.16 ACDelco (General Motors)

- 6.4.17 ISKY Racing Cams

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment