PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063289

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063289

Japan Tire Manufacturing Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

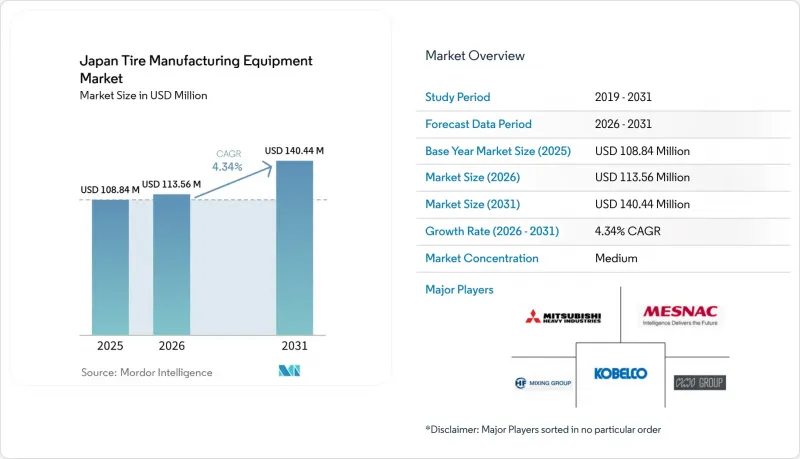

According to Mordor Intelligence, the japanese tire manufacturing equipment market size is projected to expand from USD 108.84 million in 2025 and USD 113.56 million in 2026 to USD 140.44 million by 2031, registering a CAGR of 4.34% between 2026 and 2031.

This report is Segmented by Equipment Type (Upstream, Building Area, and Curing & Inspection), Tire Design (Bias and Radial), Vehicle Type (Two-Wheelers, Three-Wheelers, and More), Rim Size (Up To 12 Inches, 12 To 18 Inches, and Above 18 Inches), and End-User (Original Equipment Manufacturers and Replacement/Aftermarket). The Market Forecasts are Provided in Terms of Value (USD).

Japan Tire Manufacturing Equipment Market Trends and Insights

Rising Demand for Fuel-Efficient, High-Performance Tires

Tires for electric and hybrid vehicles must balance low rolling resistance with higher load ratings. This need pushes manufacturers to adopt silica-rich treads and maintain calendering tolerances. Bridgestone's ENLITEN compound showcases this industry shift, necessitating co-extrusion heads to manage durometer variance across tread layers . Meanwhile, Yokohama Rubber is investing in a motorsports line to boost capacity. This expansion highlights the growing demand for precision curing presses. Tires tailored for EVs now feature sensor pockets for RFID chips and tire-pressure monitoring. These innovations not only enhance vehicle performance but also extend replacement cycles for traditional building and cutting machines. In response, equipment suppliers are rolling out advanced tools like laser-guided bias cutters and servo-driven tread extruders, both boasting micron-level accuracy. Additionally, pilot-produced bio-based sulfur copolymers are achieving a reduction in rolling resistance. However, these copolymers modify cure kinetics, necessitating upgrades to mixers for lower-temperature processing to prevent scorching.

Automation and Industry 4.0 Adoption in Japanese Tire Plants

Sumitomo Rubber deployed a Hitachi-PTC manufacturing execution system (MES) at its Shirakawa facility. This system aggregates live data from mixers, extruders, builders, and presses, leading to a significant reduction in unplanned downtime. Bridgestone's BCMA module further enhances efficiency, cutting changeover time substantially. This allows a single building machine to seamlessly switch between SKUs without manual drum changes. Kobe Steel is promoting bolt-on IoT sensor kits that transmit data on torque, viscosity, and temperature to cloud-based AI dashboards. These digitally optimized cycles have already achieved notable energy savings per mixing batch. While new machines come equipped with embedded sensors, a large portion of Japan's existing machines were installed earlier, presenting a significant retrofit opportunity. Financing options are becoming more accessible, especially with METI subsidies covering a portion of qualifying energy-efficient equipment. This support has significantly shortened the payback period.

High CAPEX and Long Payback Period for Curing Presses

In Japan, a modern hydraulic curing press equipped with RFID tagging comes with a high price tag. When installation is factored in, costs rise further. Mid-sized firms grapple with extended payback horizons. This duration not only surpasses standard financing tenors but also inches perilously close to the timelines for technological obsolescence. While leasing models are available, they remain a rarity in Japan. This is largely due to a prevailing preference for outright ownership, championed by both suppliers and accountants. As a result, larger OEMs capitalize on this landscape, placing multi-press orders to secure volume discounts.

In contrast, smaller producers find themselves in a bind, delaying replacements and extending the life of their older presses through third-party service contracts. This pronounced divergence in approach dampens immediate demand for new presses. However, it simultaneously amplifies interest in sensor-retrofit kits, predictive-maintenance software, and partial hydraulic upgrades.

Other drivers and restraints analyzed in the detailed report include:

- Flexible Modular Equipment for EV/AV Tire Customization

- Capacity-Expansion Programs by Leading OEMs

- Raw-Material Cost Volatility Squeezing Equipment Budgets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, upstream mixing and preparation assets accounted for 42.21% of the Japanese tire manufacturing equipment market. This dominance underscores the surging demand for precise compound control, especially as electric vehicle (EV) tires become increasingly mainstream. Projects in Japan's tire manufacturing equipment market are now integrating recycled fillers and bio-polymers into mixing lines, all while ensuring batch uniformity. Suppliers are also adopting torque analytics and automated feed hoppers, crucial for maintaining the consistent viscosity needed in low-rolling-resistance treads.

Systems for cutting and inspection are projected to expand at a 6.21% CAGR through 2031, outpacing all other categories. This growth is driven by camera-guided knife stations, X-ray tread scanners, and AI-driven defect classifiers, especially as OEMs enforce zero-defect standards for tires in autonomous vehicles. Additionally, portable smart sensors are being retrofitted onto legacy drums, enabling plants to gather predictive maintenance data without replacing older equipment. This capability is particularly appealing for shops with limited space.

Radial-tire technology commanded 89.22% of the Japanese tire manufacturing equipment market in 2025 and is expected to grow at a 6.39% CAGR through 2031, keeping the Japanese tire manufacturing equipment market firmly aligned with global radially-skewed automotive production. Servo-driven belt applicators now ensure the 90-degree cord angle remains within a minimal margin by monitoring tension in real-time. This precision is crucial for meeting OEM-specified rolling resistance metrics.

Holding a notable market share, the bias-tire gear caters to specialty farm, construction, and two-wheeler segments, with exports primarily directed to Southeast Asia. While growth remains modest due to limited unit volumes, Japanese manufacturers like Kawata Engineering find profitability by exporting compact bias cutters, priced significantly lower than their radial counterparts. Although national sustainability regulations target energy-intensive bias curing, potentially stifling future investments, a transitional demand endures as emerging markets gradually shift towards radial adoption.

List of Companies Covered in this Report:

- Kobe Steel Ltd.

- Mitsubishi Heavy Industries Machinery Systems, Ltd.

- Sanyo Machine Works, Ltd.

- Kawata Mfg. Co., Ltd.

- Fukui Rubber Industry Co., Ltd.

- Ishikawa Machinery Co., Ltd.

- Kurimoto Ltd.

- HF Mixing Group

- VMI Holland B.V.

- Mesnac Co., Ltd.

- Comerio Ercole S.p.A.

- Zeppelin Systems GmbH

- L&T Rubber Processing Machinery

- Himile Mechanical Science & Technology Co., Ltd.

- Guilin Rubber Machinery Co., Ltd.

- Safe-Run Machinery (Suzhou) Co., Ltd.

- Steelastic Company LLC

- Pelmar Engineering Ltd.

- Uzer Makina

- Yingkou JinDing Machinery Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Fuel-Efficient, High-Performance Tires

- 4.2.2 Automation and Industry 4.0 Adoption in Japanese Tire Plants

- 4.2.3 Capacity-Expansion Programs by Bridgestone, Sumitomo, Yokohama and Others

- 4.2.4 Flexible Modular Equipment for EV / AV Tire Customization

- 4.2.5 Government Subsidies for Energy-Efficient Machinery Upgrades

- 4.2.6 Novel Mixing Tech for Sustainable Rubber Blends

- 4.3 Market Restraints

- 4.3.1 High CAPEX and Long Payback Period for Curing Presses

- 4.3.2 Raw-Material Cost Volatility Squeezing Equipment Budgets

- 4.3.3 Space Constraints in Aging Domestic Plants

- 4.3.4 Slow METI Certification for Imported Machinery

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Equipment Type

- 5.1.1 Upstream (Mixer & Component Preparation)

- 5.1.1.1 Mixing Machines / Rubber Mixers

- 5.1.1.2 Calendaring Machines

- 5.1.1.3 Extrusion Machines

- 5.1.1.4 Cutting Machines

- 5.1.1.5 Others (Cooling Units, etc.)

- 5.1.2 Building Area

- 5.1.2.1 Bead Winding Machine

- 5.1.2.2 Tire Building Machine

- 5.1.2.3 Others (Strip Winding Machine, etc.)

- 5.1.3 Curing & Inspection (Testing Area)

- 5.1.3.1 Curing Press Machines

- 5.1.3.2 Tire Painting Machines

- 5.1.3.3 Others (Inspection Machines, etc.)

- 5.1.1 Upstream (Mixer & Component Preparation)

- 5.2 By Tire Design

- 5.2.1 Bias

- 5.2.2 Radial

- 5.3 By Vehicle Type

- 5.3.1 Two-wheelers

- 5.3.2 Three-wheelers

- 5.3.3 Passenger Cars

- 5.3.4 Light Commercial Vehicles

- 5.3.5 Medium & Heavy Commercial Vehicles

- 5.3.6 Off-Road Vehicles

- 5.4 By Rim Size

- 5.4.1 Up to 12 inches

- 5.4.2 12 to 18 inches

- 5.4.3 Above 18 inches

- 5.5 By End-User

- 5.5.1 Original Equipment Manufacturers (OEMs)

- 5.5.2 Replacement / Aftermarket

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 Kobe Steel Ltd.

- 6.4.2 Mitsubishi Heavy Industries Machinery Systems, Ltd.

- 6.4.3 Sanyo Machine Works, Ltd.

- 6.4.4 Kawata Mfg. Co., Ltd.

- 6.4.5 Fukui Rubber Industry Co., Ltd.

- 6.4.6 Ishikawa Machinery Co., Ltd.

- 6.4.7 Kurimoto Ltd.

- 6.4.8 HF Mixing Group

- 6.4.9 VMI Holland B.V.

- 6.4.10 Mesnac Co., Ltd.

- 6.4.11 Comerio Ercole S.p.A.

- 6.4.12 Zeppelin Systems GmbH

- 6.4.13 L&T Rubber Processing Machinery

- 6.4.14 Himile Mechanical Science & Technology Co., Ltd.

- 6.4.15 Guilin Rubber Machinery Co., Ltd.

- 6.4.16 Safe-Run Machinery (Suzhou) Co., Ltd.

- 6.4.17 Steelastic Company LLC

- 6.4.18 Pelmar Engineering Ltd.

- 6.4.19 Uzer Makina

- 6.4.20 Yingkou JinDing Machinery Co., Ltd.

7 Market Opportunities & Future Outlook